Solution - Forecasting with Linear Factor Pricing Models#

# Output from previous execution

Loaded 25 size/value portfolios (FF 25)

Date range: 1980-01-31 to 2025-08-31

Number of monthly observations: 548

# Output from previous execution

Built forecasts using expanding factor premia

Factor model: ['MKT', 'HML', 'RMW', 'UMD']

Rolling window: 60 months (5.0 years)

# Output from previous execution

| OOS R-squared | IC | |

|---|---|---|

| Mean | -0.4% | -5.9% |

| Median | -0.4% | -5.3% |

| Min | -1.1% | -11.7% |

| Max | 0.2% | 0.2% |

| % Positive | 16.0% | 4.0% |

# Output from previous execution

| OOS R-squared | IC | |

|---|---|---|

| ME5 BM4 | -0.0% | 0.2% |

| BIG LoBM | 0.2% | -0.8% |

| SMALL LoBM | 0.1% | -1.0% |

| ME4 BM5 | 0.2% | -2.7% |

| ME3 BM5 | -0.0% | -3.3% |

| OOS R-squared | IC | |

|---|---|---|

| ME4 BM3 | -0.5% | -11.7% |

| ME4 BM1 | -0.6% | -11.7% |

| ME5 BM2 | 0.0% | -11.4% |

| ME4 BM2 | -0.4% | -9.5% |

| ME3 BM3 | -0.3% | -9.2% |

# Output from previous execution

CAPM / expanding...

CAPM / constant...

AQR 4-Factor / expanding...

AQR 4-Factor / constant...

FF 5-Factor / expanding...

FF 5-Factor / constant...

| Mean OOS R-squared | Mean IC | ||

|---|---|---|---|

| Factor Model | Lambda Method | ||

| CAPM | expanding | -0.0% | -7.3% |

| constant | 0.3% | 0.2% | |

| AQR 4-Factor | expanding | -0.4% | -5.9% |

| constant | 0.1% | -0.1% | |

| FF 5-Factor | expanding | -0.1% | -7.5% |

| constant | 0.3% | -0.7% |

# Output from previous execution

CAPM / 36 months...

CAPM / 48 months...

CAPM / 60 months...

CAPM / 120 months...

CAPM / 180 months...

CAPM / 240 months...

AQR 4-Factor / 36 months...

AQR 4-Factor / 48 months...

AQR 4-Factor / 60 months...

AQR 4-Factor / 120 months...

AQR 4-Factor / 180 months...

AQR 4-Factor / 240 months...

| Mean OOS R-squared | Mean IC | ||

|---|---|---|---|

| Factor Model | Beta Window (months) | ||

| CAPM | 36 | 0.4% | 1.8% |

| 48 | 0.4% | 1.0% | |

| 60 | 0.3% | 0.2% | |

| 120 | 0.3% | 2.7% | |

| 180 | 0.2% | 1.4% | |

| 240 | 0.2% | 1.9% | |

| AQR 4-Factor | 36 | 0.2% | 1.4% |

| 48 | 0.1% | -0.8% | |

| 60 | 0.1% | -0.1% | |

| 120 | 0.2% | 1.3% | |

| 180 | 0.1% | 0.3% | |

| 240 | 0.2% | 1.4% |

# Output from previous execution

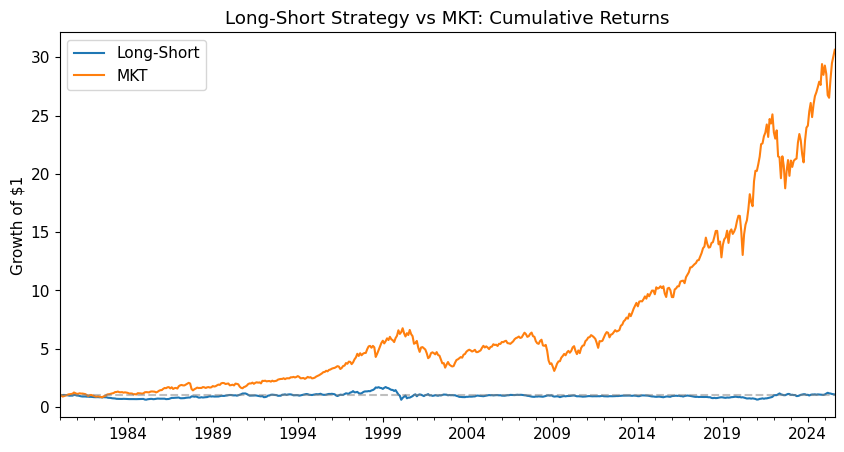

| Mean | Vol | Sharpe | |

|---|---|---|---|

| Long-Short | 1.3% | 14.4% | 8.7% |

| MKT | 8.8% | 15.6% | 56.1% |

# Output from previous execution

| alpha | MKT | r-squared | Info Ratio | |

|---|---|---|---|---|

| Long-Short | 2.85% | -18.27% | 3.94% | 20.22% |

# Output from previous execution

# Output from previous execution

| Mean OOS R-squared | Mean IC | |

|---|---|---|

| CAPM | -0.0% | -7.3% |

| AQR 4-Factor | -0.4% | -5.9% |

| FF 5-Factor | -0.1% | -7.5% |

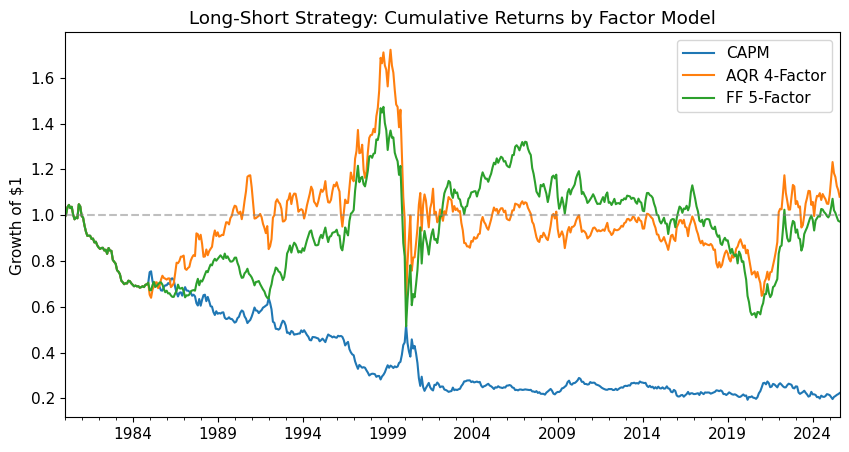

| Mean | Vol | Sharpe | |

|---|---|---|---|

| CAPM | -2.6% | 12.0% | -21.5% |

| AQR 4-Factor | 1.3% | 14.4% | 8.7% |

| FF 5-Factor | 0.9% | 13.4% | 6.7% |

| alpha | MKT | r-squared | Info Ratio | |

|---|---|---|---|---|

| CAPM | -5.17% | 29.69% | 15.04% | -46.88% |

| AQR 4-Factor | 2.85% | -18.27% | 3.94% | 20.22% |

| FF 5-Factor | 2.39% | -17.08% | 3.94% | 18.15% |

# Output from previous execution