Solution - Replicating Regressions#

# Output from previous execution

| shortName | quoteType | currency | volume | totalAssets | longBusinessSummary | |

|---|---|---|---|---|---|---|

| ticker | ||||||

| SPY | SPDR S&P 500 | ETF | USD | 25604208 | 627773800448 | The Trust seeks to achieve its investment obje... |

| EFA | iShares MSCI EAFE ETF | ETF | USD | 10653257 | 54985711616 | The fund generally will invest at least 80% of... |

| EEM | iShares MSCI Emerging Index Fun | ETF | USD | 17962107 | 17468592128 | The fund generally will invest at least 80% of... |

| PSP | Invesco Global Listed Private E | ETF | USD | 8928 | 277930496 | The fund generally will invest at least 90% of... |

| QAI | NYLI Hedge Multi-Strategy Track | ETF | USD | 49257 | 637390272 | The fund is a "fund of funds" which means it i... |

| HYG | iShares iBoxx $ High Yield Corp | ETF | USD | 22374708 | 15881510912 | The underlying index is a rules-based index co... |

| DBC | Invesco DB Commodity Index Trac | ETF | USD | 478168 | 1387142912 | The fund pursues its investment objective by i... |

| IYR | iShares U.S. Real Estate ETF | ETF | USD | 2699001 | 4990495744 | The fund seeks to track the investment results... |

| IEF | iShares 7-10 Year Treasury Bond | ETF | USD | 2340833 | 32854654976 | The underlying index measures the performance ... |

| BWX | SPDR Bloomberg International Tr | ETF | USD | 180426 | 959621824 | The fund generally invests substantially all, ... |

| TIP | iShares TIPS Bond ETF | ETF | USD | 2132017 | 15497157632 | The index tracks the performance of inflation-... |

| SHV | iShares Short Treasury Bond ETF | ETF | USD | 1850899 | 18620065792 | The fund will invest at least 80% of its asset... |

# Output from previous execution

| BWX | DBC | EEM | EFA | HYG | IEF | IYR | PSP | QAI | SHV | SPY | TIP | |

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| Date | ||||||||||||

| 2015-02-28 | -0.010834 | 0.044253 | 0.044080 | 0.063378 | 0.022312 | -0.024717 | -0.025976 | 0.064102 | 0.034138 | 0.000181 | 0.056204 | -0.012886 |

| 2015-03-31 | -0.013922 | -0.060539 | -0.014973 | -0.014286 | -0.009478 | 0.008561 | 0.010745 | -0.010454 | -0.001667 | -0.000091 | -0.015706 | -0.004819 |

| 2015-04-30 | 0.019579 | 0.071471 | 0.068527 | 0.036466 | 0.008714 | -0.006330 | -0.048160 | 0.053982 | 0.002004 | 0.000091 | 0.009834 | 0.006779 |

| 2015-05-31 | -0.032312 | -0.031711 | -0.041045 | 0.001955 | 0.003555 | -0.004164 | -0.003311 | 0.026868 | -0.000333 | 0.000000 | 0.012856 | -0.010056 |

| 2015-06-30 | -0.007442 | 0.016375 | -0.029309 | -0.031182 | -0.018871 | -0.016309 | -0.043979 | -0.019153 | -0.013671 | 0.000091 | -0.020312 | -0.010246 |

| ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... |

| 2024-08-31 | 0.030519 | -0.020815 | 0.009779 | 0.032603 | 0.015474 | 0.013458 | 0.054008 | 0.001225 | 0.007648 | 0.004979 | 0.023366 | 0.007990 |

| 2024-09-30 | 0.023484 | 0.007237 | 0.057413 | 0.007833 | 0.016971 | 0.013825 | 0.030631 | 0.051617 | 0.014548 | 0.004586 | 0.021005 | 0.014976 |

| 2024-10-31 | -0.048497 | 0.014369 | -0.030746 | -0.052732 | -0.009636 | -0.033874 | -0.034947 | -0.013779 | -0.005923 | 0.003576 | -0.008924 | -0.018469 |

| 2024-11-30 | 0.002212 | -0.019920 | -0.026772 | -0.003156 | 0.016446 | 0.010209 | 0.040688 | 0.064952 | 0.022891 | 0.003697 | 0.059633 | 0.004981 |

| 2024-12-31 | -0.032164 | 0.011994 | -0.013676 | -0.029502 | -0.012152 | -0.023790 | -0.090579 | -0.053956 | -0.016640 | 0.000161 | -0.020497 | -0.017664 |

119 rows × 12 columns

# Output from previous execution

| portfolio | |

|---|---|

| Date | |

| 2015-02-28 | 0.011887 |

| 2015-03-31 | 0.001796 |

| 2015-04-30 | 0.000374 |

| 2015-05-31 | 0.004765 |

| 2015-06-30 | -0.023278 |

| ... | ... |

| 2024-08-31 | 0.019085 |

| 2024-09-30 | 0.027655 |

| 2024-10-31 | -0.022130 |

| 2024-11-30 | 0.034685 |

| 2024-12-31 | -0.046241 |

119 rows × 1 columns

# Output from previous execution

| Dep. Variable: | portfolio | R-squared: | 0.780 |

|---|---|---|---|

| Model: | OLS | Adj. R-squared: | 0.778 |

| Method: | Least Squares | F-statistic: | 414.7 |

| Date: | Tue, 07 Jan 2025 | Prob (F-statistic): | 2.86e-40 |

| Time: | 16:34:05 | Log-Likelihood: | 329.70 |

| No. Observations: | 119 | AIC: | -655.4 |

| Df Residuals: | 117 | BIC: | -649.8 |

| Df Model: | 1 | ||

| Covariance Type: | nonrobust |

| coef | std err | t | P>|t| | [0.025 | 0.975] | |

|---|---|---|---|---|---|---|

| const | -0.0034 | 0.001 | -2.332 | 0.021 | -0.006 | -0.001 |

| SPY | 0.6474 | 0.032 | 20.365 | 0.000 | 0.584 | 0.710 |

| Omnibus: | 3.740 | Durbin-Watson: | 1.968 |

|---|---|---|---|

| Prob(Omnibus): | 0.154 | Jarque-Bera (JB): | 3.181 |

| Skew: | 0.314 | Prob(JB): | 0.204 |

| Kurtosis: | 3.497 | Cond. No. | 22.7 |

Notes:

[1] Standard Errors assume that the covariance matrix of the errors is correctly specified.

# Output from previous execution

| Dep. Variable: | portfolio | R-squared: | 0.825 |

|---|---|---|---|

| Model: | OLS | Adj. R-squared: | 0.822 |

| Method: | Least Squares | F-statistic: | 274.1 |

| Date: | Tue, 07 Jan 2025 | Prob (F-statistic): | 1.10e-44 |

| Time: | 16:34:05 | Log-Likelihood: | 343.45 |

| No. Observations: | 119 | AIC: | -680.9 |

| Df Residuals: | 116 | BIC: | -672.6 |

| Df Model: | 2 | ||

| Covariance Type: | nonrobust |

| coef | std err | t | P>|t| | [0.025 | 0.975] | |

|---|---|---|---|---|---|---|

| const | -0.0027 | 0.001 | -2.051 | 0.043 | -0.005 | -9.11e-05 |

| SPY | 0.4241 | 0.050 | 8.549 | 0.000 | 0.326 | 0.522 |

| HYG | 0.5404 | 0.098 | 5.492 | 0.000 | 0.346 | 0.735 |

| Omnibus: | 0.907 | Durbin-Watson: | 2.253 |

|---|---|---|---|

| Prob(Omnibus): | 0.635 | Jarque-Bera (JB): | 0.879 |

| Skew: | 0.204 | Prob(JB): | 0.644 |

| Kurtosis: | 2.898 | Cond. No. | 85.4 |

Notes:

[1] Standard Errors assume that the covariance matrix of the errors is correctly specified.

# Output from previous execution

Correlation between portfolio and replication: 90.85%.

Square of this correaltion is 82.54%

which equals the R-squared.

# Output from previous execution

Correlation between SPY and HYG is 81.9%

# Output from previous execution

| IYR | PSP | QAI | IEF | SHV | EEM | EFA | HYG | const | BWX | DBC | SPY | TIP | |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| weights | 0.25 | 0.25 | 0.25 | 0.25 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | -0.00 |

| Dep. Variable: | portfolio | R-squared: | 1.000 |

|---|---|---|---|

| Model: | OLS | Adj. R-squared: | 1.000 |

| Method: | Least Squares | F-statistic: | 1.685e+29 |

| Date: | Tue, 07 Jan 2025 | Prob (F-statistic): | 0.00 |

| Time: | 16:34:05 | Log-Likelihood: | 4114.2 |

| No. Observations: | 119 | AIC: | -8202. |

| Df Residuals: | 106 | BIC: | -8166. |

| Df Model: | 12 | ||

| Covariance Type: | nonrobust |

| coef | std err | t | P>|t| | [0.025 | 0.975] | |

|---|---|---|---|---|---|---|

| const | 1.735e-16 | 3.3e-17 | 5.259 | 0.000 | 1.08e-16 | 2.39e-16 |

| BWX | 1.665e-16 | 2.13e-15 | 0.078 | 0.938 | -4.05e-15 | 4.39e-15 |

| DBC | 6.939e-18 | 6.74e-16 | 0.010 | 0.992 | -1.33e-15 | 1.34e-15 |

| EEM | 7.008e-16 | 9.75e-16 | 0.719 | 0.474 | -1.23e-15 | 2.63e-15 |

| EFA | 3.634e-16 | 1.57e-15 | 0.232 | 0.817 | -2.74e-15 | 3.47e-15 |

| HYG | 2.776e-16 | 2.28e-15 | 0.122 | 0.903 | -4.25e-15 | 4.8e-15 |

| IEF | 0.2500 | 3e-15 | 8.34e+13 | 0.000 | 0.250 | 0.250 |

| IYR | 0.2500 | 8.33e-16 | 3e+14 | 0.000 | 0.250 | 0.250 |

| PSP | 0.2500 | 1.08e-15 | 2.31e+14 | 0.000 | 0.250 | 0.250 |

| QAI | 0.2500 | 5.36e-15 | 4.66e+13 | 0.000 | 0.250 | 0.250 |

| SHV | 1.11e-15 | 1.58e-14 | 0.070 | 0.944 | -3.02e-14 | 3.24e-14 |

| SPY | 0 | 1.56e-15 | 0 | 1.000 | -3.1e-15 | 3.1e-15 |

| TIP | -1.665e-16 | 3.8e-15 | -0.044 | 0.965 | -7.69e-15 | 7.36e-15 |

| Omnibus: | 17.654 | Durbin-Watson: | 0.719 |

|---|---|---|---|

| Prob(Omnibus): | 0.000 | Jarque-Bera (JB): | 38.094 |

| Skew: | 0.563 | Prob(JB): | 5.35e-09 |

| Kurtosis: | 5.533 | Cond. No. | 702. |

Notes:

[1] Standard Errors assume that the covariance matrix of the errors is correctly specified.

# Output from previous execution

| Dep. Variable: | EEM | R-squared: | 0.789 |

|---|---|---|---|

| Model: | OLS | Adj. R-squared: | 0.761 |

| Method: | Least Squares | F-statistic: | 28.25 |

| Date: | Tue, 07 Jan 2025 | Prob (F-statistic): | 1.50e-23 |

| Time: | 16:34:05 | Log-Likelihood: | 221.60 |

| No. Observations: | 95 | AIC: | -419.2 |

| Df Residuals: | 83 | BIC: | -388.6 |

| Df Model: | 11 | ||

| Covariance Type: | nonrobust |

| coef | std err | t | P>|t| | [0.025 | 0.975] | |

|---|---|---|---|---|---|---|

| const | 0.0045 | 0.004 | 1.231 | 0.222 | -0.003 | 0.012 |

| BWX | 0.8016 | 0.218 | 3.682 | 0.000 | 0.369 | 1.235 |

| DBC | -0.0003 | 0.073 | -0.004 | 0.997 | -0.145 | 0.144 |

| EFA | 0.5235 | 0.184 | 2.844 | 0.006 | 0.157 | 0.890 |

| HYG | -0.2021 | 0.237 | -0.853 | 0.396 | -0.673 | 0.269 |

| IEF | -0.8203 | 0.350 | -2.343 | 0.022 | -1.517 | -0.124 |

| IYR | -0.0130 | 0.094 | -0.139 | 0.890 | -0.200 | 0.173 |

| PSP | -0.1470 | 0.142 | -1.038 | 0.302 | -0.429 | 0.135 |

| QAI | 1.9912 | 0.560 | 3.558 | 0.001 | 0.878 | 3.104 |

| SHV | -2.1211 | 3.064 | -0.692 | 0.491 | -8.215 | 3.973 |

| SPY | -0.2012 | 0.183 | -1.098 | 0.275 | -0.566 | 0.163 |

| TIP | 0.2022 | 0.431 | 0.469 | 0.640 | -0.656 | 1.060 |

| Omnibus: | 1.305 | Durbin-Watson: | 2.314 |

|---|---|---|---|

| Prob(Omnibus): | 0.521 | Jarque-Bera (JB): | 1.215 |

| Skew: | -0.272 | Prob(JB): | 0.545 |

| Kurtosis: | 2.895 | Cond. No. | 1.19e+03 |

Notes:

[1] Standard Errors assume that the covariance matrix of the errors is correctly specified.

[2] The condition number is large, 1.19e+03. This might indicate that there are

strong multicollinearity or other numerical problems.

# Output from previous execution

| BWX | QAI | EFA | const | TIP | DBC | IYR | SHV | HYG | PSP | SPY | IEF | |

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| t-stats | 3.7 | 3.6 | 2.8 | 1.2 | 0.5 | -0.0 | -0.1 | -0.7 | -0.9 | -1.0 | -1.1 | -2.3 |

# Output from previous execution

# Output from previous execution

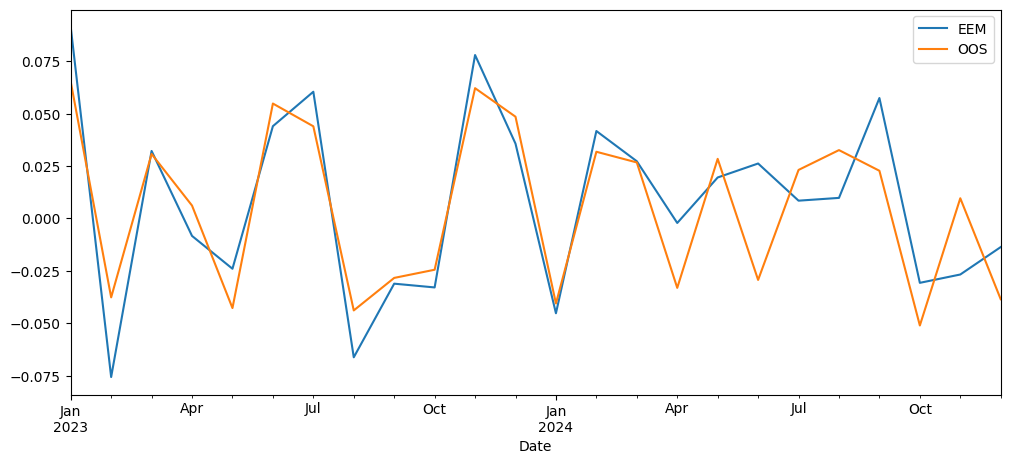

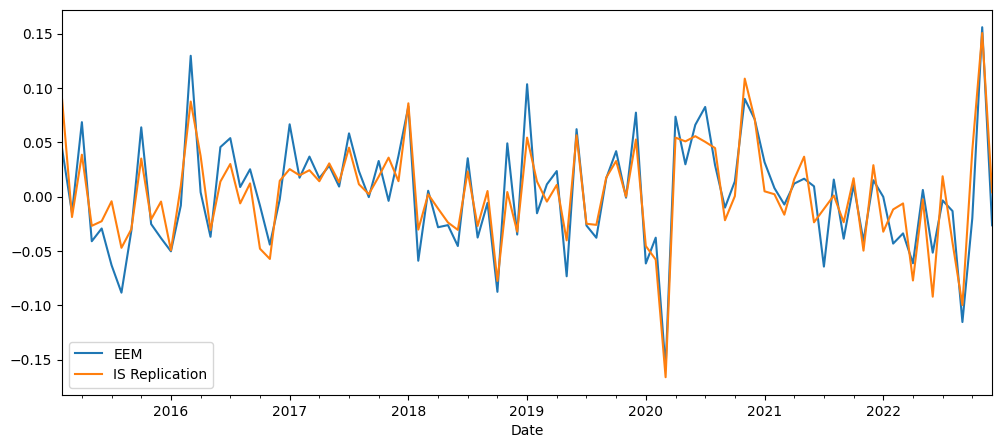

Correlation between EEM and Replicating Portfolio

In-Sample: 88.8%

Out-of-Sample: 85.0%

# Output from previous execution