MV of S&P 500#

import numpy as np

import pandas as pd

pd.options.display.float_format = "{:,.4f}".format

import matplotlib.pyplot as plt

import seaborn as sns

import statsmodels.api as sm

from sklearn.linear_model import LinearRegression

filepath_data = '../data/spx_returns_weekly.xlsx'

SHEET = 's&p500 rets'

rets_raw = pd.read_excel(filepath_data,sheet_name=SHEET).set_index('date')

def delta_parameter(target_mean):

delta = (target_mean - mu.T@w_gmv)/(mu.T@w_tan - mu.T@w_gmv)

return delta

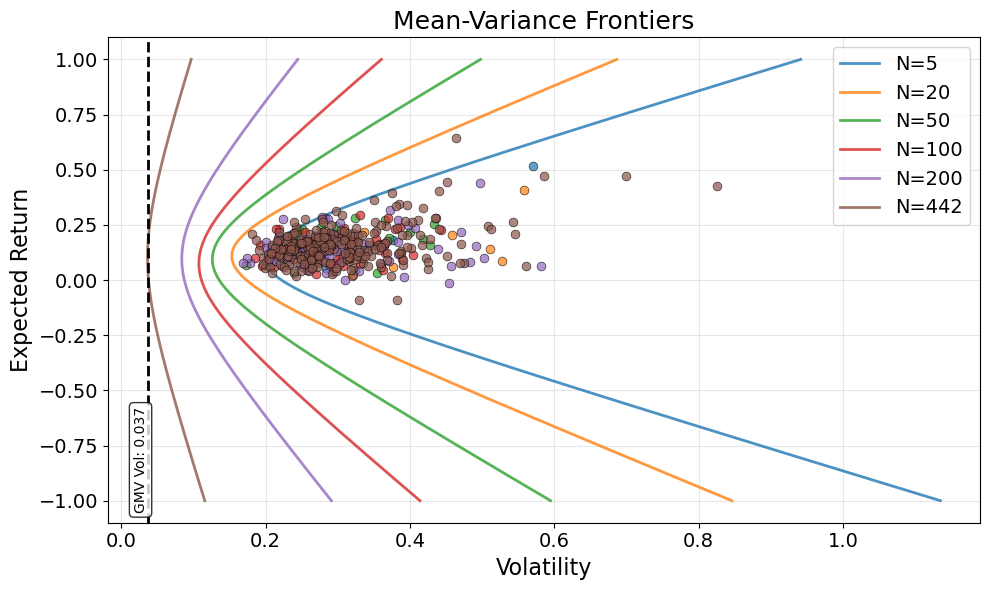

# Multi-Frontier Plot for Various N Values (Nested Subsamples)

N_values = [5, 20, 50, 100, 200, len(rets_raw.columns)]

fig, ax = plt.subplots(figsize=(10, 6))

# Create nested subsamples

np.random.seed(2025) # Use same seed for reproducibility

all_assets = list(rets_raw.columns)

np.random.shuffle(all_assets) # Shuffle once for consistent ordering

# Track which assets are included at each N level

asset_inclusion_level = {}

nested_asset_sets = {}

# Initialize summary data storage

summary_data = []

# Create nested sets

for i, N in enumerate(N_values):

if N > len(rets_raw.columns):

continue # Skip if N is larger than available assets

# For the first N, take the first N assets

# For subsequent N values, take the previous assets plus additional ones

if i == 0:

selected_assets = all_assets[:N]

else:

# Take all assets from previous levels plus additional ones

selected_assets = nested_asset_sets[N_values[i-1]] + all_assets[len(nested_asset_sets[N_values[i-1]]):N]

nested_asset_sets[N] = selected_assets

idx = sorted(selected_assets)

rets_n = rets_raw[idx]

# Track which N level each asset was first included in

for asset in selected_assets:

if asset not in asset_inclusion_level:

asset_inclusion_level[asset] = N

# Calculate metrics for this N

mu_n = rets_n.mean() * FREQ

covmat_n = rets_n.cov() * FREQ

vec_ones_n = np.ones(mu_n.shape)

# Calculate GMV and tangency portfolios

w_gmv_n = np.linalg.solve(covmat_n, vec_ones_n)

w_tan_n = np.linalg.solve(covmat_n, mu_n)

w_gmv_n /= w_gmv_n.sum()

w_tan_n /= w_tan_n.sum()

# Calculate Sharpe ratios and gross market value for this N

# Individual asset Sharpe ratios

individual_sharpe = mu_n / (rets_n.std() * np.sqrt(FREQ))

max_individual_sharpe = individual_sharpe.max()

# Tangency portfolio Sharpe ratio

tangency_sharpe = (mu_n.T @ w_tan_n) / np.sqrt(w_tan_n.T @ covmat_n @ w_tan_n)

# Gross market value of tangency portfolio

gross_market_value = np.abs(w_tan_n).sum()

# Store summary data

summary_data.append({

'N': N,

'Max_Individual_Sharpe': max_individual_sharpe,

'Tangency_Sharpe': tangency_sharpe,

'Gross_Market_Value': gross_market_value

})

# Define delta parameter function for this N

def delta_parameter_n(target_mean):

delta = (target_mean - mu_n.T@w_gmv_n)/(mu_n.T@w_tan_n - mu_n.T@w_gmv_n)

return delta

# Create frontier for this N

MAX_n = (N+5) * .0005 * FREQ

MIN_n = - MAX_n/1.6

MAX_n = -1

MIN_n = 1

grid_n = np.linspace(MIN_n, MAX_n, 250)

df_n = pd.DataFrame(index=grid_n, columns=['delta','mu','vol'], dtype=float)

for mu_target in grid_n:

delta = delta_parameter_n(mu_target)

w = delta * w_tan_n + (1-delta) * w_gmv_n

df_n.loc[mu_target,'delta'] = delta

df_n.loc[mu_target,'mu'] = w.T @ mu_n

df_n.loc[mu_target,'vol'] = np.sqrt(w.T @ covmat_n @ w)

# Plot this frontier

ax.plot(df_n['vol'], df_n['mu'],

linewidth=2, alpha=0.8, label=f'N={N}')

# Plot base assets colored by inclusion level

base_mu = rets_raw.mean() * FREQ

base_vol = rets_raw.std() * np.sqrt(FREQ)

# Create color mapping for assets based on their first inclusion level

for N in N_values:

if N > len(rets_raw.columns):

continue

# Get assets that were first included at this N level

assets_at_level = [asset for asset, level in asset_inclusion_level.items() if level == N]

if assets_at_level:

# Get the corresponding mu and vol for these assets

mu_at_level = base_mu[assets_at_level]

vol_at_level = base_vol[assets_at_level]

# Plot with the color corresponding to this N level

color_idx = N_values.index(N)

ax.scatter(vol_at_level, mu_at_level,

alpha=0.7, s=40,

zorder=5, edgecolors='black', linewidth=0.5)

# Add vertical line at the global minimum variance portfolio of the largest N

largest_N = N_values[-1]

if largest_N <= len(rets_raw.columns):

# Get the assets for the largest N

largest_assets = nested_asset_sets[largest_N]

largest_rets = rets_raw[largest_assets]

# Calculate GMV portfolio for largest N

largest_mu = largest_rets.mean() * FREQ

largest_covmat = largest_rets.cov() * FREQ

largest_vec_ones = np.ones(largest_mu.shape)

largest_w_gmv = np.linalg.solve(largest_covmat, largest_vec_ones)

largest_w_gmv /= largest_w_gmv.sum()

# Calculate volatility of GMV portfolio

gmv_vol = np.sqrt(largest_w_gmv.T @ largest_covmat @ largest_w_gmv)

# Add vertical line

ax.axvline(x=gmv_vol, color='black', linestyle='--', linewidth=2)

# Add text label on x-axis

ax.text(gmv_vol, ax.get_ylim()[0] + 0.02 * (ax.get_ylim()[1] - ax.get_ylim()[0]),

f'GMV Vol: {gmv_vol:.3f}',

rotation=90, verticalalignment='bottom', horizontalalignment='right',

fontsize=10, bbox=dict(boxstyle='round,pad=0.3', facecolor='white', alpha=0.8))

ax.set_xlabel('Volatility', fontsize=16)

ax.set_ylabel('Expected Return', fontsize=16)

ax.set_title('Mean-Variance Frontiers', fontsize=18)

ax.legend(fontsize=14)

ax.grid(True, alpha=0.3)

# Increase tick label font sizes

ax.tick_params(axis='x', labelsize=14)

ax.tick_params(axis='y', labelsize=14)

plt.tight_layout()

plt.show()

# Summary Table: Sharpe Ratios and Gross Market Values by N

summary_df = pd.DataFrame(summary_data)

summary_df = summary_df.set_index('N')

# Format the display

pd.options.display.float_format = "{:,.4f}".format

summary_df.style.format({

'Max_Individual_Sharpe': "{:,.1%}",

'Tangency_Sharpe': "{:,.1%}",

'Gross_Market_Value': "{:,.1%}"

})

| Max_Individual_Sharpe | Tangency_Sharpe | Gross_Market_Value | |

|---|---|---|---|

| N | |||

| 5 | 90.5% | 109.5% | 272.2% |

| 20 | 90.5% | 150.8% | 449.9% |

| 50 | 91.9% | 202.3% | 809.6% |

| 100 | 108.3% | 277.7% | 1,888.7% |

| 200 | 122.6% | 409.6% | 2,978.0% |

| 442 | 139.3% | 1,038.3% | 8,247.8% |

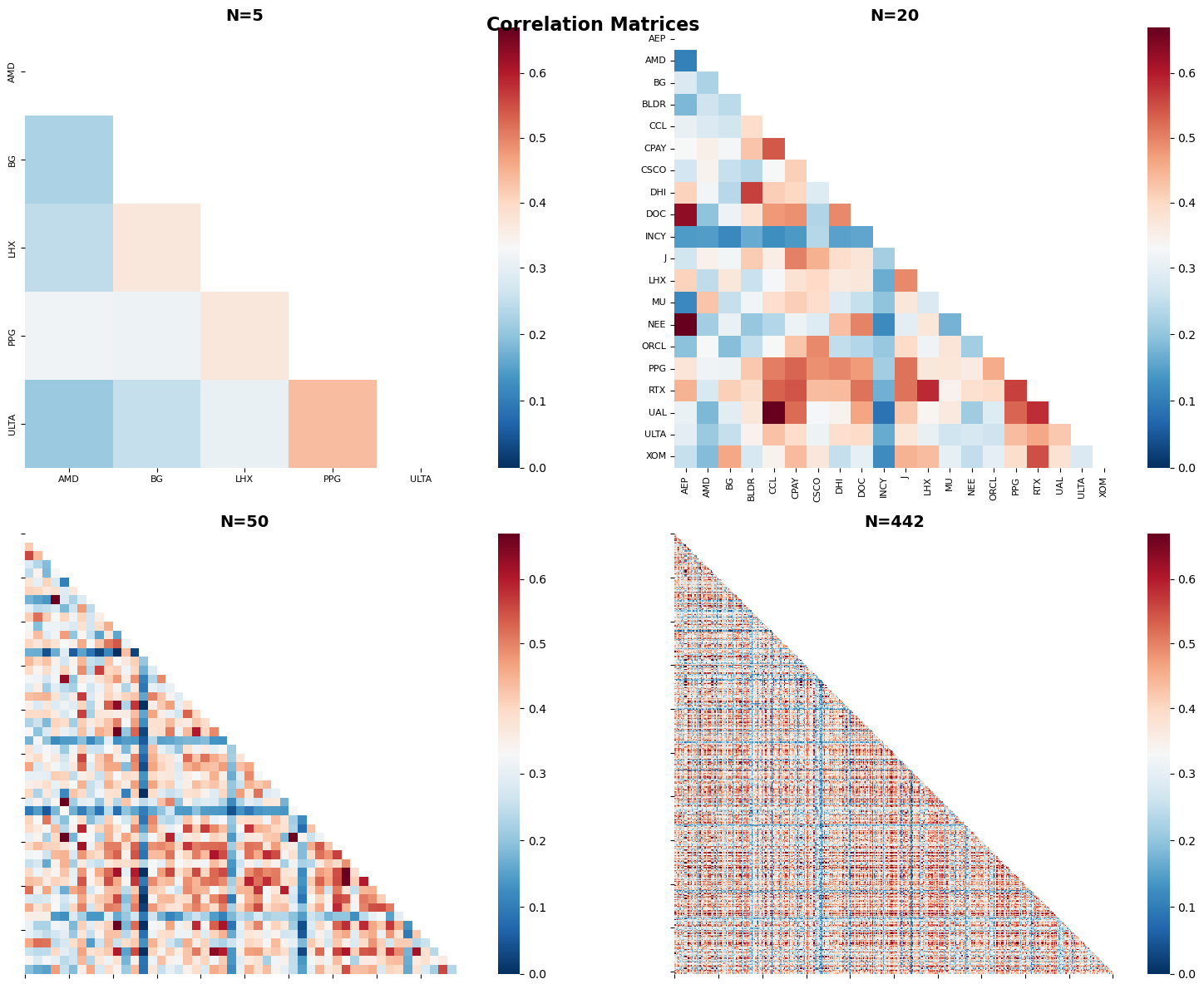

# 2x2 Correlation Heatmaps for Various Subsets

from matplotlib.colors import TwoSlopeNorm

# Define subsets to analyze - smallest 3 N values and largest N

N_values_sorted = sorted([5, 20, 50, 100, len(rets_raw.columns)])

subset_configs = [

{'name': f'N={N_values_sorted[0]}', 'size': N_values_sorted[0], 'title': f'N={N_values_sorted[0]}'},

{'name': f'N={N_values_sorted[1]}', 'size': N_values_sorted[1], 'title': f'N={N_values_sorted[1]}'},

{'name': f'N={N_values_sorted[2]}', 'size': N_values_sorted[2], 'title': f'N={N_values_sorted[2]}'},

{'name': f'N={N_values_sorted[-1]}', 'size': N_values_sorted[-1], 'title': f'N={N_values_sorted[-1]}'}

]

# Use the same random seed for consistency

np.random.seed(2025)

all_assets = list(rets_raw.columns)

np.random.shuffle(all_assets)

fig, axes = plt.subplots(2, 2, figsize=(16, 12))

axes = axes.flatten()

for i, config in enumerate(subset_configs):

# Select assets for this subset

selected_assets = sorted(all_assets[:config['size']])

rets_subset = rets_raw[selected_assets]

# Calculate correlation matrix

corr_matrix = rets_subset.corr()

# Set upper triangle and diagonal to NaN for cleaner visualization

mask = np.triu(np.ones_like(corr_matrix), k=0)

corr_matrix_masked = corr_matrix.copy()

corr_matrix_masked[mask.astype(bool)] = np.nan

# Set up color normalization

center = 0.33

vmin = 0

vmax = 0.67

norm = TwoSlopeNorm(vmin=vmin, vcenter=center, vmax=vmax)

# Create heatmap

sns.heatmap(corr_matrix_masked,

annot=False, # No annotations

norm=norm,

cmap='RdBu_r',

cbar=True,

ax=axes[i],

square=True)

axes[i].set_title(config['title'], fontsize=14, fontweight='bold')

# Adjust tick labels for readability

if config['size'] <= 20:

axes[i].tick_params(axis='both', labelsize=8)

else:

axes[i].tick_params(axis='both', labelsize=6)

# For larger matrices, show fewer tick labels

step = max(1, config['size'] // 10)

axes[i].set_xticks(range(0, config['size'], step))

axes[i].set_yticks(range(0, config['size'], step))

plt.tight_layout()

plt.suptitle('Correlation Matrices',

fontsize=16, fontweight='bold', y=0.98)

plt.show()

# Correlation Statistics DataFrame

correlation_stats = []

# Use the same random seed for consistency

np.random.seed(2025)

all_assets = list(rets_raw.columns)

np.random.shuffle(all_assets)

for config in subset_configs:

# Select assets for this subset

selected_assets = sorted(all_assets[:config['size']])

rets_subset = rets_raw[selected_assets]

# Calculate correlation matrix

corr_matrix = rets_subset.corr()

# Calculate correlation statistics (excluding diagonal)

mask = np.triu(np.ones_like(corr_matrix), k=1)

correlations = corr_matrix.values[mask.astype(bool)]

avg_pairwise_corr = correlations.mean()

min_corr = correlations.min()

max_corr = correlations.max()

# Calculate condition number and determinant of correlation matrix

condition_number = np.linalg.cond(corr_matrix)

determinant = np.linalg.det(corr_matrix)

correlation_stats.append({

'N': config['size'],

'Min Correlation': min_corr,

'Max Correlation': max_corr,

'Avg Pairwise Correlation': avg_pairwise_corr,

'Condition Number': condition_number,

'Determinant': determinant

})

# Create DataFrame

correlation_df = pd.DataFrame(correlation_stats)

correlation_df = correlation_df.set_index('N')

# Format the display

display_df = correlation_df.copy()

display_df['Min Correlation'] = display_df['Min Correlation'].apply(lambda x: f"{x:.0%}")

display_df['Max Correlation'] = display_df['Max Correlation'].apply(lambda x: f"{x:.0%}")

display_df['Avg Pairwise Correlation'] = display_df['Avg Pairwise Correlation'].apply(lambda x: f"{x:.0%}")

display_df['Condition Number'] = display_df['Condition Number'].apply(lambda x: f"{x:,.0f}")

display_df['Determinant'] = display_df['Determinant'].apply(lambda x: f"{x:.0e}")

display_df

| Min Correlation | Max Correlation | Avg Pairwise Correlation | Condition Number | Determinant | |

|---|---|---|---|---|---|

| N | |||||

| 5 | 21% | 43% | 30% | 4 | 5e-01 |

| 20 | 9% | 72% | 34% | 33 | 1e-04 |

| 50 | -5% | 77% | 34% | 115 | 1e-13 |

| 442 | -9% | 94% | 36% | 83,061 | 0e+00 |

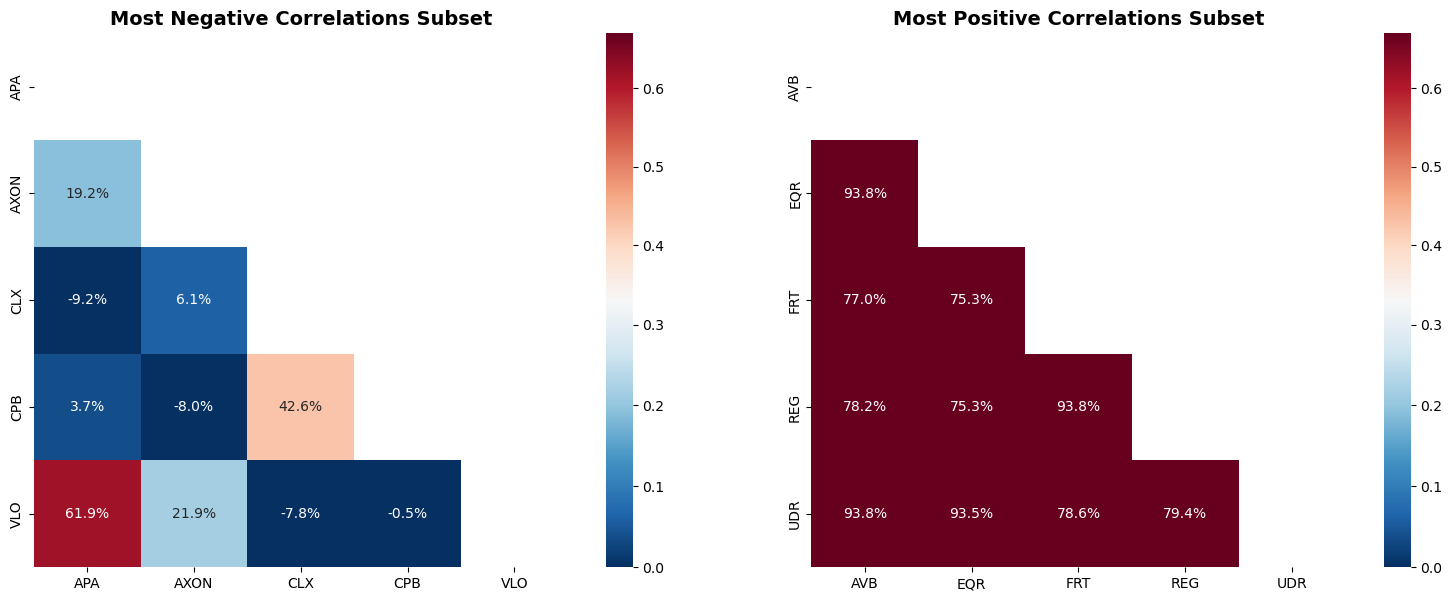

# Correlation Heatmaps for Most Negative and Most Positive Pairs

from matplotlib.colors import TwoSlopeNorm

# Calculate correlation matrix for full dataset

full_corr_matrix = rets_raw.corr()

# Find all pairwise correlations (excluding diagonal)

mask = np.triu(np.ones_like(full_corr_matrix), k=1)

correlations_flat = full_corr_matrix.values[mask.astype(bool)]

# Get indices of the correlations

row_indices, col_indices = np.where(mask)

# Find the 6 stocks involved in the 3 most negative correlations

min_corr_indices = []

min_corr_values = []

correlations_temp = correlations_flat.copy()

for i in range(3):

min_idx = np.argmin(correlations_temp)

min_corr_indices.append((row_indices[min_idx], col_indices[min_idx]))

min_corr_values.append(correlations_temp[min_idx])

correlations_temp[min_idx] = 0 # Remove this correlation from consideration

# Get unique stocks from the 3 most negative pairs

min_corr_stocks = set()

for row_idx, col_idx in min_corr_indices:

min_corr_stocks.add(full_corr_matrix.index[row_idx])

min_corr_stocks.add(full_corr_matrix.index[col_idx])

min_corr_stocks = sorted(list(min_corr_stocks))

# Find the 6 stocks involved in the 3 most positive correlations

max_corr_indices = []

max_corr_values = []

correlations_temp = correlations_flat.copy()

for i in range(3):

max_idx = np.argmax(correlations_temp)

max_corr_indices.append((row_indices[max_idx], col_indices[max_idx]))

max_corr_values.append(correlations_temp[max_idx])

correlations_temp[max_idx] = 0 # Remove this correlation from consideration

# Get unique stocks from the 3 most positive pairs

max_corr_stocks = set()

for row_idx, col_idx in max_corr_indices:

max_corr_stocks.add(full_corr_matrix.index[row_idx])

max_corr_stocks.add(full_corr_matrix.index[col_idx])

max_corr_stocks = sorted(list(max_corr_stocks))

# Create 1x2 subplot figure

fig, axes = plt.subplots(1, 2, figsize=(16, 6))

# Set up color normalization

center = 0.33

vmin = 0

vmax = 0.67

norm = TwoSlopeNorm(vmin=vmin, vcenter=center, vmax=vmax)

# Plot 1: Most negative correlations subset

min_corr_subset = full_corr_matrix.loc[min_corr_stocks, min_corr_stocks]

# Set upper triangle and diagonal to NaN

mask_min = np.triu(np.ones_like(min_corr_subset), k=0)

min_corr_subset_masked = min_corr_subset.copy()

min_corr_subset_masked[mask_min.astype(bool)] = np.nan

sns.heatmap(min_corr_subset_masked,

annot=True,

fmt='.1%',

norm=norm,

cmap='RdBu_r',

cbar=True,

ax=axes[0],

square=True)

axes[0].set_title('Most Negative Correlations Subset', fontsize=14, fontweight='bold')

axes[0].set_xlabel('')

axes[0].set_ylabel('')

# Plot 2: Most positive correlations subset

max_corr_subset = full_corr_matrix.loc[max_corr_stocks, max_corr_stocks]

# Set upper triangle and diagonal to NaN

mask_max = np.triu(np.ones_like(max_corr_subset), k=0)

max_corr_subset_masked = max_corr_subset.copy()

max_corr_subset_masked[mask_max.astype(bool)] = np.nan

sns.heatmap(max_corr_subset_masked,

annot=True,

fmt='.1%',

norm=norm,

cmap='RdBu_r',

cbar=True,

ax=axes[1],

square=True)

axes[1].set_title('Most Positive Correlations Subset', fontsize=14, fontweight='bold')

axes[1].set_xlabel('')

axes[1].set_ylabel('')

plt.tight_layout()

plt.show()

# Get firm names for the most and least correlated pairs

# Read the first sheet to get ticker to company name mapping

ticker_mapping = pd.read_excel(filepath_data, sheet_name=0)

# Create a dictionary mapping tickers to company names

ticker_to_name = dict(zip(ticker_mapping.iloc[:, 0], ticker_mapping.iloc[:, 1]))

# Create DataFrame for 3 most negative correlations

most_negative_pairs = []

for i, (row_idx, col_idx) in enumerate(min_corr_indices):

stock1 = full_corr_matrix.index[row_idx]

stock2 = full_corr_matrix.index[col_idx]

corr_val = min_corr_values[i]

most_negative_pairs.append({

'Ticker_1': stock1,

'Company_1': ticker_to_name.get(stock1, 'Unknown'),

'Ticker_2': stock2,

'Company_2': ticker_to_name.get(stock2, 'Unknown'),

'Correlation': corr_val

})

most_negative_df = pd.DataFrame(most_negative_pairs)

most_negative_df.index = [f'Pair {i+1}' for i in range(len(most_negative_pairs))]

# Create DataFrame for 3 most positive correlations

most_positive_pairs = []

for i, (row_idx, col_idx) in enumerate(max_corr_indices):

stock1 = full_corr_matrix.index[row_idx]

stock2 = full_corr_matrix.index[col_idx]

corr_val = max_corr_values[i]

most_positive_pairs.append({

'Ticker_1': stock1,

'Company_1': ticker_to_name.get(stock1, 'Unknown'),

'Ticker_2': stock2,

'Company_2': ticker_to_name.get(stock2, 'Unknown'),

'Correlation': corr_val

})

most_positive_df = pd.DataFrame(most_positive_pairs)

most_positive_df.index = [f'Pair {i+1}' for i in range(len(most_positive_pairs))]

# Display the DataFrames

most_negative_df[['Ticker_1', 'Company_1', 'Ticker_2', 'Company_2', 'Correlation']].style.hide(axis='index').format({'Correlation': '{:.0%}'})

| Ticker_1 | Company_1 | Ticker_2 | Company_2 | Correlation |

|---|---|---|---|---|

| APA | APA Corp | CLX | Clorox Co/The | -9% |

| AXON | Axon Enterprise Inc | CPB | The Campbell's Company | -8% |

| CLX | Clorox Co/The | VLO | Valero Energy Corp | -8% |

most_positive_df[['Ticker_1', 'Company_1', 'Ticker_2', 'Company_2', 'Correlation']].style.hide(axis='index').format({'Correlation': '{:.0%}'})

| Ticker_1 | Company_1 | Ticker_2 | Company_2 | Correlation |

|---|---|---|---|---|

| AVB | AvalonBay Communities Inc | UDR | UDR Inc | 94% |

| FRT | Federal Realty Investment Trus | REG | Regency Centers Corp | 94% |

| AVB | AvalonBay Communities Inc | EQR | Equity Residential | 94% |