import pandas as pd

import numpy as np

from sklearn.linear_model import LinearRegression

from sklearn.decomposition import PCA

import statsmodels.api as sm

import matplotlib.pyplot as plt

import seaborn as sns

import scipy.stats as stats

pd.options.display.float_format = "{:,.4f}".format

plt.style.use('seaborn-v0_8')

from cmds.portfolio import *

# Load S&P 500 individual stock returns

spx_file = '../data/spx_returns_weekly.xlsx'

stock_rets = pd.read_excel(spx_file, 's&p500 rets').set_index('date')

bench_rets = pd.read_excel(spx_file, 'benchmark rets').set_index('date')

# Load sector ETF returns

sector_file = '../data/sector_etf_data.xlsx'

sector_rets = pd.read_excel(sector_file, 'total returns').set_index('date')

print(f"Stock returns shape: {stock_rets.shape}")

print(f"Sector returns shape: {sector_rets.shape}")

print(f"Benchmark returns shape: {bench_rets.shape}")

Stock returns shape: (542, 442)

Sector returns shape: (380, 11)

Benchmark returns shape: (542, 7)

# Align all datasets to common dates

common_dates = stock_rets.index.intersection(sector_rets.index).intersection(bench_rets.index)

# Extract aligned data

stocks = stock_rets.loc[common_dates]

sectors = sector_rets.loc[common_dates]

benchmarks = bench_rets.loc[common_dates]

# Combine sector and benchmark factors (excluding overlapping ETFs)

benchmarks_clean = benchmarks.drop(columns=['SPY','TLT','IYR','BTC'], errors='ignore')

factors = pd.concat([sectors, benchmarks_clean], axis=1)

# Display final dataset information

final_dataset_info = pd.DataFrame({

'Metric': ['Common Dates', 'Number of Stocks', 'Number of Factors', 'Date Range'],

'Value': [

f"{len(common_dates)} observations",

f"{stocks.shape[1]} stocks",

f"{factors.shape[1]} factors",

f"{common_dates[0].strftime('%Y-%m-%d')} to {common_dates[-1].strftime('%Y-%m-%d')}"

]

})

final_dataset_info

| Metric | Value | |

|---|---|---|

| 0 | Common Dates | 361 observations |

| 1 | Number of Stocks | 442 stocks |

| 2 | Number of Factors | 14 factors |

| 3 | Date Range | 2018-06-29 to 2025-05-23 |

TICKS = [

'AAPL',

'BRK/B',

'NVDA',

'TSLA',

'V',

'C',

'LLY',

'AMZN',

]

# Get OLS metrics for factor decomposition

ols_metrics = get_ols_metrics(factors, stocks, annualization=52)

ols_metrics.loc[TICKS].style.format('{:.1%}',na_rep='-')

| alpha | XLK | XLI | XLF | XLC | XLRE | XLE | XLY | XLB | XLV | XLU | XLP | USO | IEF | GLD | r-squared | Info Ratio | |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| AAPL | 7.5% | 102.2% | -25.2% | -5.0% | 2.0% | 8.3% | -1.5% | 1.3% | -10.8% | -1.1% | 6.5% | 36.1% | 0.7% | -15.2% | -9.1% | 68.3% | 46.3% |

| BRK/B | 7.2% | 2.2% | 5.4% | 66.4% | 2.9% | -9.4% | 3.9% | -18.2% | -0.2% | 15.1% | 0.3% | 18.7% | 0.1% | 12.5% | -3.3% | 74.8% | 69.5% |

| NVDA | 22.9% | 179.2% | 6.7% | -16.7% | -24.0% | -44.5% | -6.2% | 48.4% | 13.5% | 1.9% | 9.5% | -57.3% | 2.4% | 18.5% | 8.2% | 68.8% | 83.6% |

| TSLA | 43.7% | 17.8% | -84.6% | -70.9% | -60.4% | -9.9% | 16.6% | 300.0% | 16.3% | -24.2% | 29.7% | 2.9% | 13.0% | -67.8% | 2.4% | 53.4% | 97.1% |

| V | 4.9% | 29.5% | -7.5% | 42.7% | 16.4% | 12.6% | -1.3% | -7.2% | -6.4% | 8.4% | -9.6% | 27.2% | -2.1% | 13.4% | -4.8% | 62.2% | 33.1% |

| C | -4.6% | 0.6% | 1.1% | 146.3% | 9.7% | -6.0% | 8.1% | 0.8% | -5.0% | -22.6% | 3.6% | -21.9% | -1.7% | 12.8% | 3.9% | 81.0% | -28.7% |

| LLY | 29.6% | 28.3% | -12.9% | -16.1% | -12.6% | 4.3% | 16.0% | -19.9% | -20.5% | 140.8% | 0.3% | -16.3% | -0.6% | 12.9% | -3.1% | 39.3% | 122.0% |

| AMZN | 0.0% | 33.2% | -44.3% | 0.1% | 34.3% | -27.6% | -0.1% | 108.0% | -17.8% | 10.4% | -7.9% | -5.9% | -1.3% | 13.1% | 15.7% | 67.8% | 0.1% |

# Perform factor decomposition for each stock

USE_INTERCEPT = True

# Initialize results DataFrames

betas = pd.DataFrame(index=stocks.columns, columns=factors.columns, dtype=float)

residuals = pd.DataFrame(index=stocks.index, columns=stocks.columns, dtype=float)

r_squared = pd.Series(index=stocks.columns, dtype=float)

# Prepare factor matrix (with intercept if needed)

X = factors.copy()

if USE_INTERCEPT:

X = sm.add_constant(X)

betas.insert(0, 'alpha', 0)

# Run regressions for each stock

for stock in stocks.columns:

y = stocks[stock]

results = sm.OLS(y, X).fit()

betas.loc[stock] = results.params

residuals[stock] = results.resid

r_squared[stock] = results.rsquared

# Display regression summary statistics

regression_summary = pd.DataFrame({

'value': [

f"{r_squared.mean():.3f}",

f"{r_squared.median():.3f}",

f"{r_squared.min():.3f}",

f"{r_squared.max():.3f}",

f"{r_squared.std():.3f}"

]

}, index=['Average R2', 'Median R2', 'Min R2', 'Max R2', 'Std R2'])

# Find stocks with min and max R2

min_r2_stock = r_squared.idxmin()

max_r2_stock = r_squared.idxmax()

r2_extremes = pd.DataFrame({

'Stock': [min_r2_stock, max_r2_stock],

'R2': [f"{r_squared[min_r2_stock]:.3f}", f"{r_squared[max_r2_stock]:.3f}"]

}, index=['Min R2', 'Max R2'])

display(regression_summary)

display(r2_extremes)

| value | |

|---|---|

| Average R2 | 0.571 |

| Median R2 | 0.570 |

| Min R2 | 0.123 |

| Max R2 | 0.899 |

| Std R2 | 0.152 |

| Stock | R2 | |

|---|---|---|

| Min R2 | ERIE | 0.123 |

| Max R2 | XOM | 0.899 |

Dimension Reduction#

nPCA = 3

# Compare PCA structure between original returns and residuals

pca_stocks = PCA()

pca_resids = PCA()

pca_stocks.fit(stocks)

pca_resids.fit(residuals)

# Calculate cumulative explained variance for first 5 components

stocks_cum_var = np.cumsum(pca_stocks.explained_variance_ratio_[:nPCA] * 100)

resids_cum_var = np.cumsum(pca_resids.explained_variance_ratio_[:nPCA] * 100)

# Create comparison DataFrame

pca_analysis = pd.DataFrame({

'Stock Returns Explained (%)': [f"{var:.2f}%" for var in stocks_cum_var],

'Residuals Explained (%)': [f"{var:.2f}%" for var in resids_cum_var]

}, index=[f'PC{i+1}' for i in range(nPCA)])

pca_analysis

| Stock Returns Explained (%) | Residuals Explained (%) | |

|---|---|---|

| PC1 | 40.75% | 4.81% |

| PC2 | 46.35% | 8.26% |

| PC3 | 50.41% | 11.37% |

# Numerical measures of correlation structure

condition_numbers = pd.DataFrame({

'Dataset': ['Original Returns', 'Residuals', 'Factors'],

'Condition Number': [

f"{np.linalg.cond(stocks.corr()):.1e}",

f"{np.linalg.cond(residuals.corr()):.1e}",

f"{np.linalg.cond(factors.corr()):.1e}"

],

'Determinant': [

f"{np.linalg.det(stocks.corr()):.1e}",

f"{np.linalg.det(residuals.corr()):.1e}",

f"{np.linalg.det(factors.corr()):.1e}"

],

'Average Correlation': [

f"{stocks.corr().abs().mean().mean():.1%}",

f"{residuals.corr().abs().mean().mean():.1%}",

f"{factors.corr().abs().mean().mean():.1%}"

]

})

condition_numbers

| Dataset | Condition Number | Determinant | Average Correlation | |

|---|---|---|---|---|

| 0 | Original Returns | 1.2e+19 | -0.0e+00 | 39.2% |

| 1 | Residuals | 4.6e+18 | 0.0e+00 | 6.9% |

| 2 | Factors | 1.0e+02 | 2.0e-06 | 50.9% |

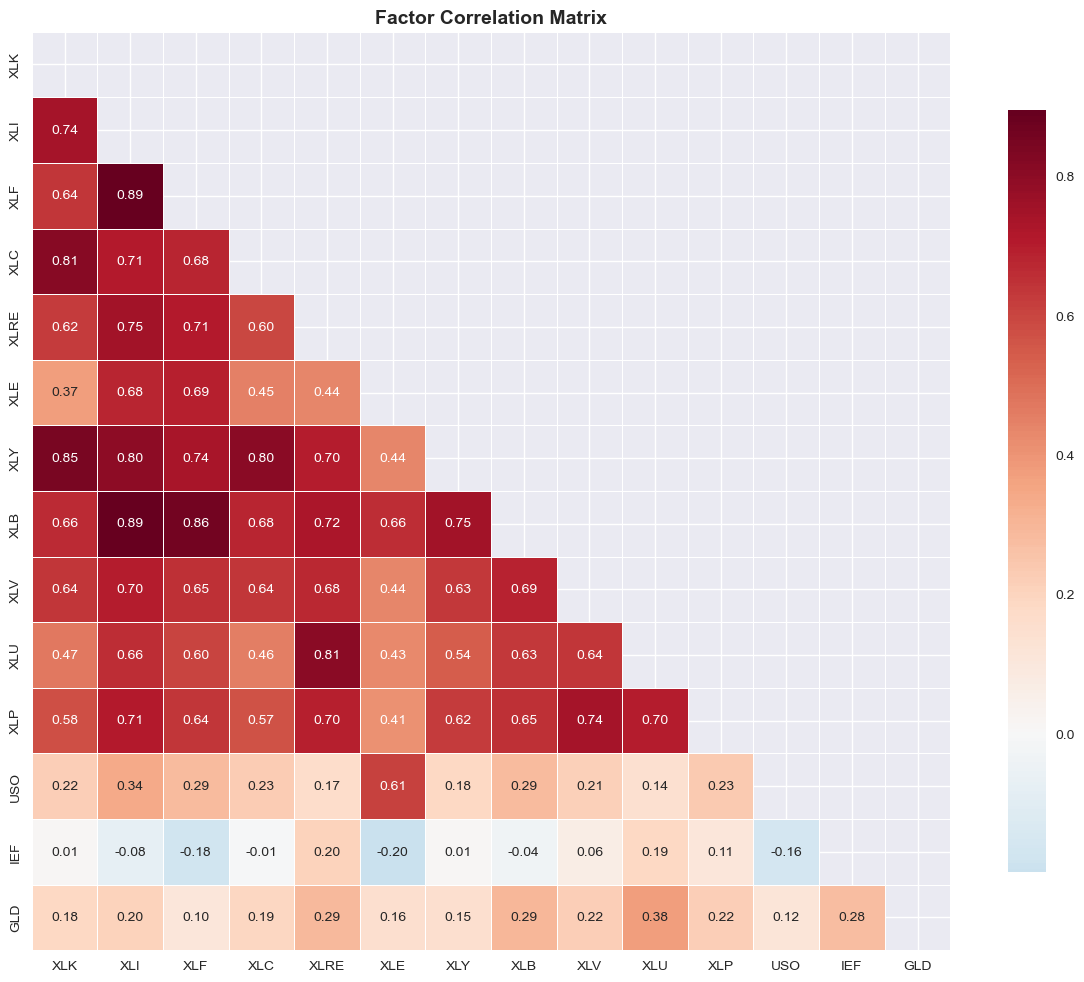

# Factor correlation heatmap

plt.figure(figsize=(12, 10))

corr_matrix = factors.corr()

mask = np.triu(np.ones_like(corr_matrix, dtype=bool))

sns.heatmap(corr_matrix, mask=mask, annot=True, fmt='.2f', cmap='RdBu_r', center=0,

square=True, linewidths=0.5, cbar_kws={"shrink": 0.8})

plt.title('Factor Correlation Matrix', fontsize=14, fontweight='bold')

plt.tight_layout()

plt.show()

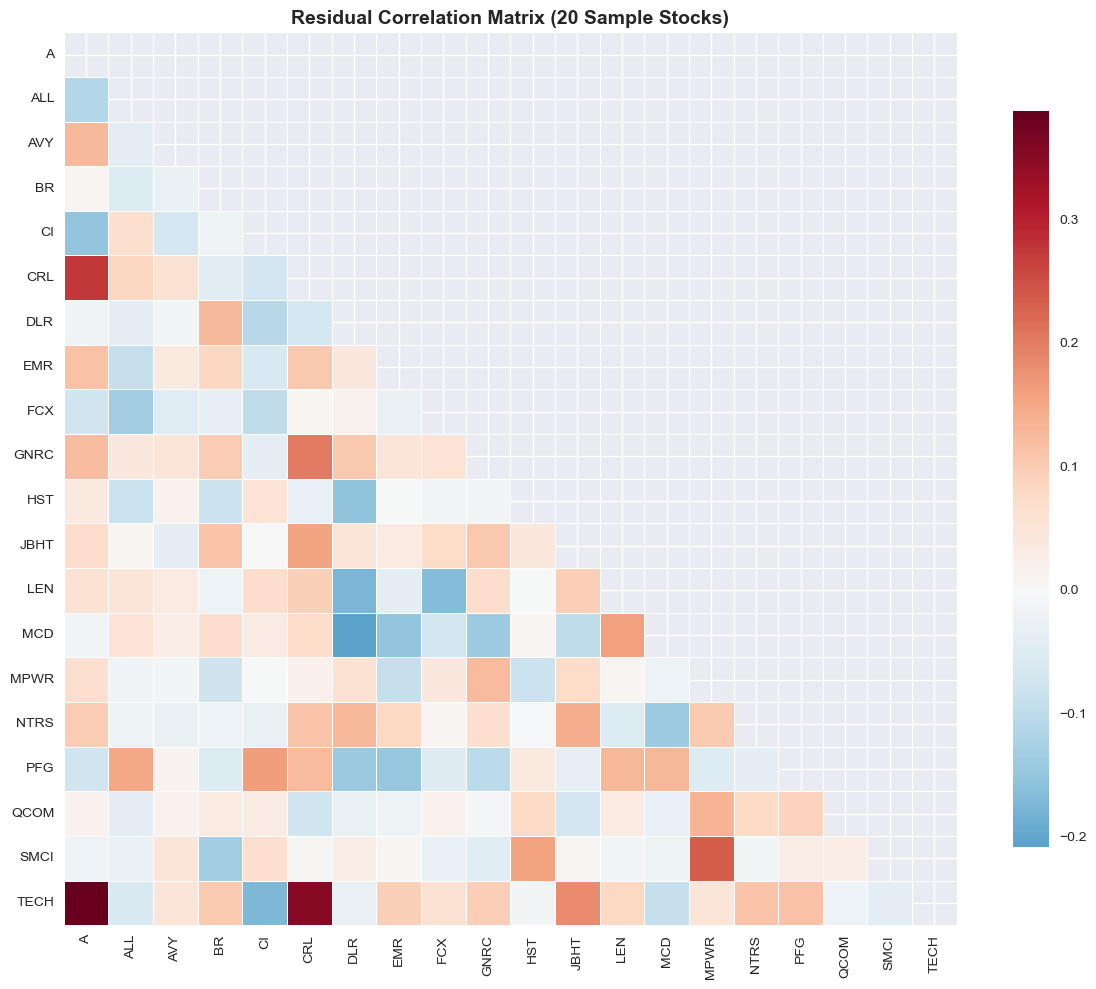

# Residual correlation heatmap (sample of stocks for readability)

# Get 20 stocks spaced evenly through the list

sample_stocks = residuals.columns[::20][:20] # Take every 20th stock, up to 20 stocks

plt.figure(figsize=(12, 10))

corr_matrix = residuals.loc[:, sample_stocks].corr()

mask = np.triu(np.ones_like(corr_matrix, dtype=bool))

sns.heatmap(corr_matrix, mask=mask, annot=False, fmt='.2f', cmap='RdBu_r', center=0,

square=True, linewidths=0.5, cbar_kws={"shrink": 0.8})

plt.title('Residual Correlation Matrix (20 Sample Stocks)', fontsize=14, fontweight='bold')

plt.tight_layout()

plt.show()

Reduced Risk#

# PRIMARY RESULTS: Key Risk Metrics Comparison

primary_results = pd.DataFrame({

'Metric': ['Volatility', 'Skewness', 'Kurtosis', 'Average Correlation'],

'Original Returns': [

stocks.std().mean(),

stocks.skew().mean(),

stocks.kurtosis().mean(),

stocks.corr().abs().mean().mean()

],

'Residuals': [

residuals.std().mean(),

residuals.skew().mean(),

residuals.kurtosis().mean(),

residuals.corr().abs().mean().mean()

],

})

primary_results.set_index('Metric', inplace=True)

primary_results.style.format({

'Original Returns': '{:.1%}',

'Residuals': '{:.1%}',

'Improvement': '{:.4f}'

}, na_rep='-')

primary_results.style.format('{:.1%}',na_rep='-')

| Original Returns | Residuals | |

|---|---|---|

| Metric | ||

| Volatility | 4.6% | 3.0% |

| Skewness | 0.1% | 6.0% |

| Kurtosis | 546.3% | 423.0% |

| Average Correlation | 39.2% | 6.9% |

# Load benchmark returns

benchmark = pd.read_excel(spx_file, sheet_name='benchmark rets')

benchmark.set_index('date', inplace=True)

# Calculate metrics for both stocks and residuals

metrics = {}

for metric, func in [('Volatility', lambda x: x.std()),

('Skewness', lambda x: x.skew()),

('SPY_Correlation', lambda x: pd.Series({col: x[col].corr(benchmark['SPY'])

for col in x.columns}))]:

# Calculate metric for both stocks and residuals

stocks_metric = func(stocks)

residuals_metric = func(residuals)

# Create dataframe with describe statistics for this metric

metric_df = pd.DataFrame({

'stocks': stocks_metric.describe(),

'residuals': residuals_metric.describe()

})

metrics[metric] = metric_df

# Combine into multilevel dataframe with metrics as top level

stats_df = pd.concat(metrics, axis=1)

stats_df.style.format('{:.1%}',na_rep='-')

| Volatility | Skewness | SPY_Correlation | ||||

|---|---|---|---|---|---|---|

| stocks | residuals | stocks | residuals | stocks | residuals | |

| count | 44200.0% | 44200.0% | 44200.0% | 44200.0% | 44200.0% | 44200.0% |

| mean | 4.6% | 3.0% | 0.1% | 6.0% | 59.2% | 0.1% |

| std | 1.2% | 1.0% | 47.7% | 70.9% | 12.2% | 0.5% |

| min | 2.5% | 1.2% | -241.9% | -617.9% | 14.9% | -1.7% |

| 25% | 3.7% | 2.3% | -26.1% | -22.7% | 52.4% | -0.3% |

| 50% | 4.3% | 2.8% | -1.5% | 11.0% | 61.1% | 0.1% |

| 75% | 5.1% | 3.4% | 23.7% | 38.7% | 67.6% | 0.4% |

| max | 11.1% | 9.6% | 196.7% | 252.4% | 82.5% | 2.1% |

# Summary table of normality improvements across all stocks

all_normality_stats = []

for stock in stocks.columns:

# Calculate key statistics

orig_skew = stocks[stock].skew()

orig_kurt = stocks[stock].kurtosis()

resid_skew = residuals[stock].skew()

resid_kurt = residuals[stock].kurtosis()

# Calculate improvement metrics

skew_improvement = abs(resid_skew) - abs(orig_skew) # Negative = improvement

kurt_improvement = abs(resid_kurt) - abs(orig_kurt) # Negative = improvement

all_normality_stats.append({

'Stock': stock,

'Orig_Skew': orig_skew,

'Resid_Skew': resid_skew,

'Skew_Change': skew_improvement,

'Orig_Kurt': orig_kurt,

'Resid_Kurt': resid_kurt,

'Kurt_Change': kurt_improvement

})

normality_summary = pd.DataFrame(all_normality_stats)

# Calculate summary statistics

normality_summary_stats = pd.DataFrame({

'Metric': [

'Stocks with Improved Skewness',

'Stocks with Improved Kurtosis',

'Average Skewness Improvement',

'Average Kurtosis Improvement'

],

'Value': [

f"{(normality_summary['Skew_Change'] < 0).sum()} / {len(normality_summary)}",

f"{(normality_summary['Kurt_Change'] < 0).sum()} / {len(normality_summary)}",

f"{normality_summary['Skew_Change'].mean():.4f}",

f"{normality_summary['Kurt_Change'].mean():.4f}"

]

})

normality_summary_stats

# Show top 10 improvements

top_skew = normality_summary.nsmallest(10, 'Skew_Change')[['Stock', 'Orig_Skew', 'Resid_Skew', 'Skew_Change']]

top_skew

| Stock | Orig_Skew | Resid_Skew | Skew_Change | |

|---|---|---|---|---|

| 425 | WELL | 1.8789 | 0.1516 | -1.7272 |

| 417 | VTR | 1.5470 | 0.2835 | -1.2634 |

| 230 | KIM | 1.9671 | 0.7868 | -1.1803 |

| 314 | PAYX | -1.0960 | 0.1423 | -0.9537 |

| 391 | TRGP | -1.1758 | -0.2274 | -0.9484 |

| 327 | PM | -1.0759 | -0.1405 | -0.9354 |

| 122 | DOC | 1.0237 | 0.1174 | -0.9063 |

| 126 | DTE | 0.7894 | -0.0039 | -0.7856 |

| 219 | J | -0.8223 | -0.0422 | -0.7801 |

| 234 | KMI | -0.7983 | -0.0694 | -0.7288 |

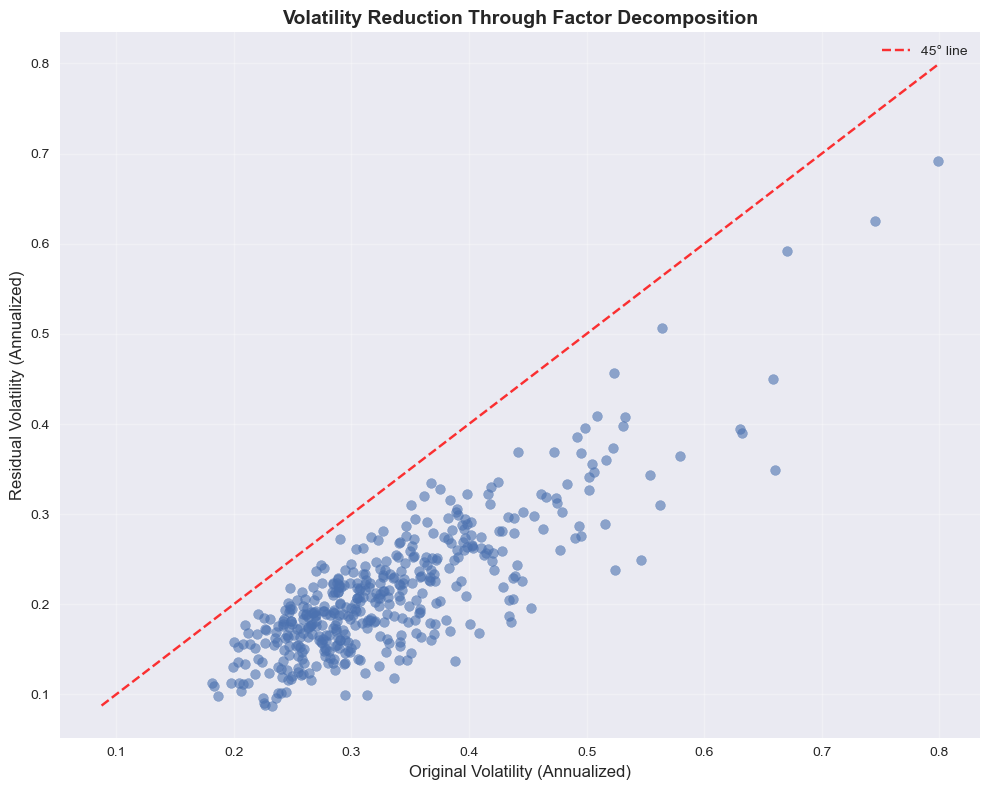

# Volatility comparison: Original vs Residuals

vols = pd.DataFrame({

'Original': stocks.std() * np.sqrt(52),

'Residuals': residuals.std() * np.sqrt(52)

})

fig, ax = plt.subplots(figsize=(10, 8))

x = vols['Original']

y = vols['Residuals']

ax.scatter(x, y, alpha=0.6, s=50)

# Add 45-degree line

min_val = min(min(x), min(y))

max_val = max(max(x), max(y))

ax.plot([min_val, max_val], [min_val, max_val], 'r--', alpha=0.8, label='45° line')

ax.set_xlabel('Original Volatility (Annualized)', fontsize=12)

ax.set_ylabel('Residual Volatility (Annualized)', fontsize=12)

ax.set_title('Volatility Reduction Through Factor Decomposition', fontsize=14, fontweight='bold')

ax.legend()

ax.grid(True, alpha=0.3)

plt.tight_layout()

plt.show()

print(f"Average volatility reduction: {(1 - vols['Residuals'].mean() / vols['Original'].mean()) * 100:.1f}%")

Average volatility reduction: 35.4%

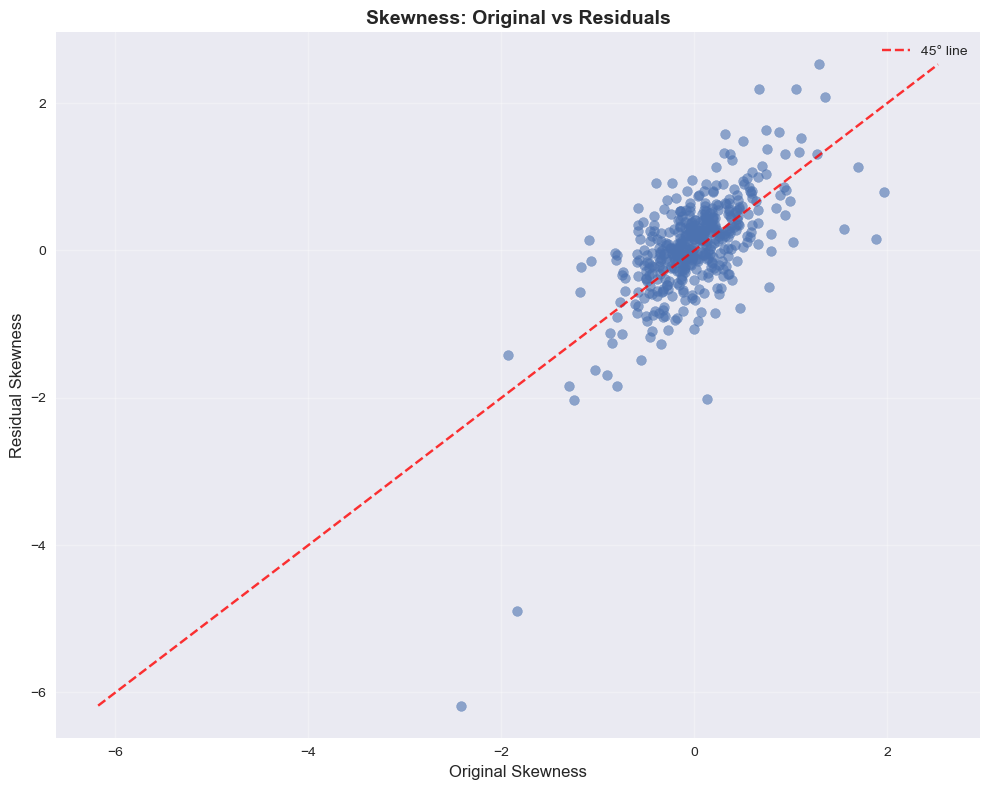

# Skewness comparison: Original vs Residuals

skews = pd.DataFrame({

'Original': stocks.skew(),

'Residuals': residuals.skew()

})

fig, ax = plt.subplots(figsize=(10, 8))

x = skews['Original']

y = skews['Residuals']

ax.scatter(x, y, alpha=0.6, s=50)

# Add 45-degree line

min_val = min(min(x), min(y))

max_val = max(max(x), max(y))

ax.plot([min_val, max_val], [min_val, max_val], 'r--', alpha=0.8, label='45° line')

ax.set_xlabel('Original Skewness', fontsize=12)

ax.set_ylabel('Residual Skewness', fontsize=12)

ax.set_title('Skewness: Original vs Residuals', fontsize=14, fontweight='bold')

ax.legend()

ax.grid(True, alpha=0.3)

plt.tight_layout()

plt.show()

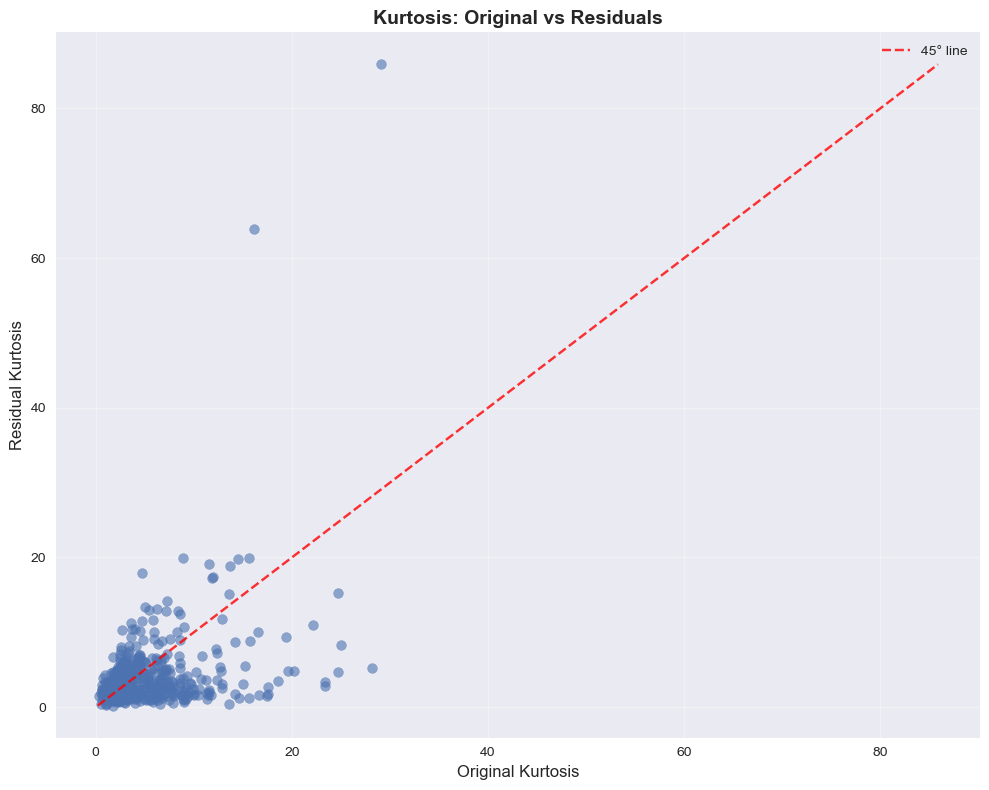

# Kurtosis comparison: Original vs Residuals

kurts = pd.DataFrame({

'Original': stocks.kurtosis(),

'Residuals': residuals.kurtosis()

})

fig, ax = plt.subplots(figsize=(10, 8))

x = kurts['Original']

y = kurts['Residuals']

ax.scatter(x, y, alpha=0.6, s=50)

# Add 45-degree line

min_val = min(min(x), min(y))

max_val = max(max(x), max(y))

ax.plot([min_val, max_val], [min_val, max_val], 'r--', alpha=0.8, label='45° line')

ax.set_xlabel('Original Kurtosis', fontsize=12)

ax.set_ylabel('Residual Kurtosis', fontsize=12)

ax.set_title('Kurtosis: Original vs Residuals', fontsize=14, fontweight='bold')

ax.legend()

ax.grid(True, alpha=0.3)

plt.tight_layout()

plt.show()

Normality#

# Statistical tests for normality improvement

from scipy.stats import shapiro, jarque_bera, normaltest

# Test normality for a sample of stocks

sample_stocks = ['AAPL', 'MSFT', 'GOOGL', 'AMZN', 'TSLA']

normality_tests = []

for stock in sample_stocks:

if stock in stocks.columns:

# Original returns

orig_stats = {

'Shapiro-Wilk p-value': shapiro(stocks[stock])[1],

'Jarque-Bera p-value': jarque_bera(stocks[stock])[1],

'D\'Agostino p-value': normaltest(stocks[stock])[1]

}

# Residuals

resid_stats = {

'Shapiro-Wilk p-value': shapiro(residuals[stock])[1],

'Jarque-Bera p-value': jarque_bera(residuals[stock])[1],

'D\'Agostino p-value': normaltest(residuals[stock])[1]

}

normality_tests.append({

'Stock': stock,

'Original_Shapiro': orig_stats['Shapiro-Wilk p-value'],

'Residual_Shapiro': resid_stats['Shapiro-Wilk p-value'],

'Original_JB': orig_stats['Jarque-Bera p-value'],

'Residual_JB': resid_stats['Jarque-Bera p-value']

})

normality_df = pd.DataFrame(normality_tests)

normality_df

| Stock | Original_Shapiro | Residual_Shapiro | Original_JB | Residual_JB | |

|---|---|---|---|---|---|

| 0 | AAPL | 0.0001 | 0.0113 | 0.0000 | 0.0001 |

| 1 | MSFT | 0.0021 | 0.0000 | 0.0000 | 0.0000 |

| 2 | GOOGL | 0.0200 | 0.0000 | 0.0114 | 0.0000 |

| 3 | AMZN | 0.0015 | 0.0001 | 0.0002 | 0.0000 |

| 4 | TSLA | 0.0000 | 0.0000 | 0.0000 | 0.0000 |

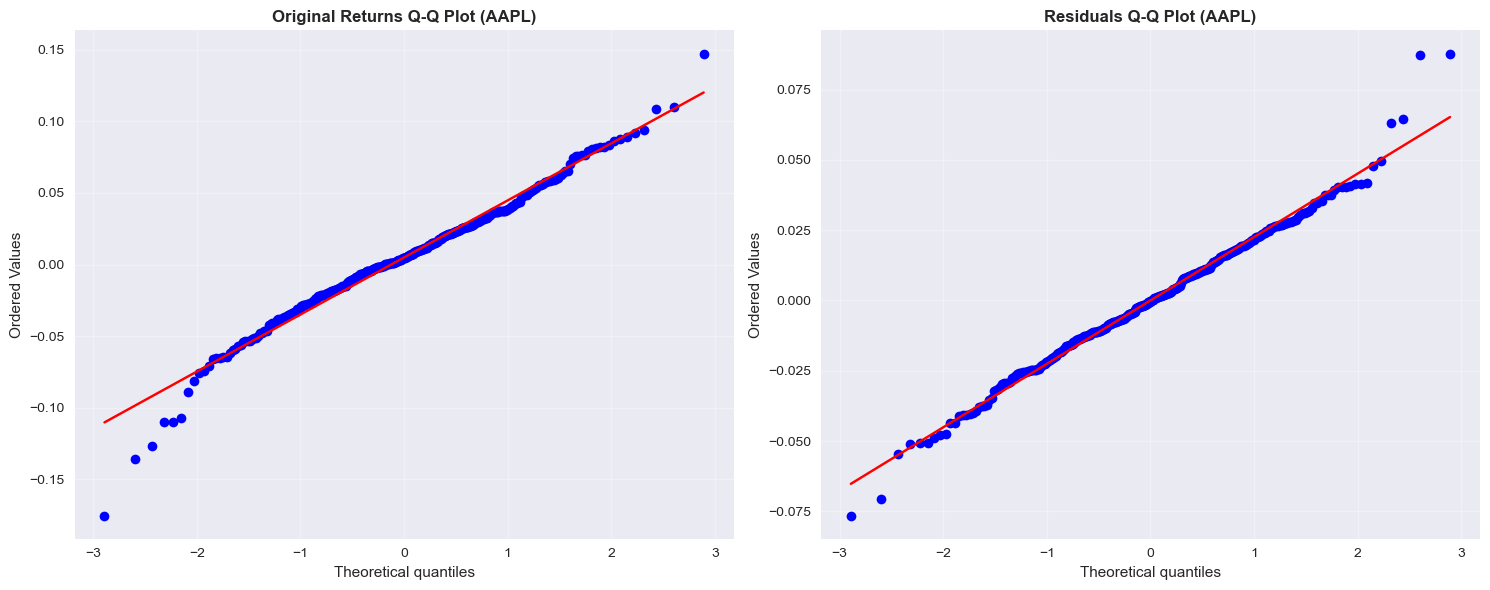

# Q-Q plots for normality assessment

fig, (ax1, ax2) = plt.subplots(1, 2, figsize=(15, 6))

# Original returns Q-Q plot

stats.probplot(stocks['AAPL'], dist="norm", plot=ax1)

ax1.set_title("Original Returns Q-Q Plot (AAPL)", fontweight='bold')

ax1.grid(True, alpha=0.3)

# Residuals Q-Q plot

stats.probplot(residuals['AAPL'], dist="norm", plot=ax2)

ax2.set_title("Residuals Q-Q Plot (AAPL)", fontweight='bold')

ax2.grid(True, alpha=0.3)

plt.tight_layout()

plt.show()

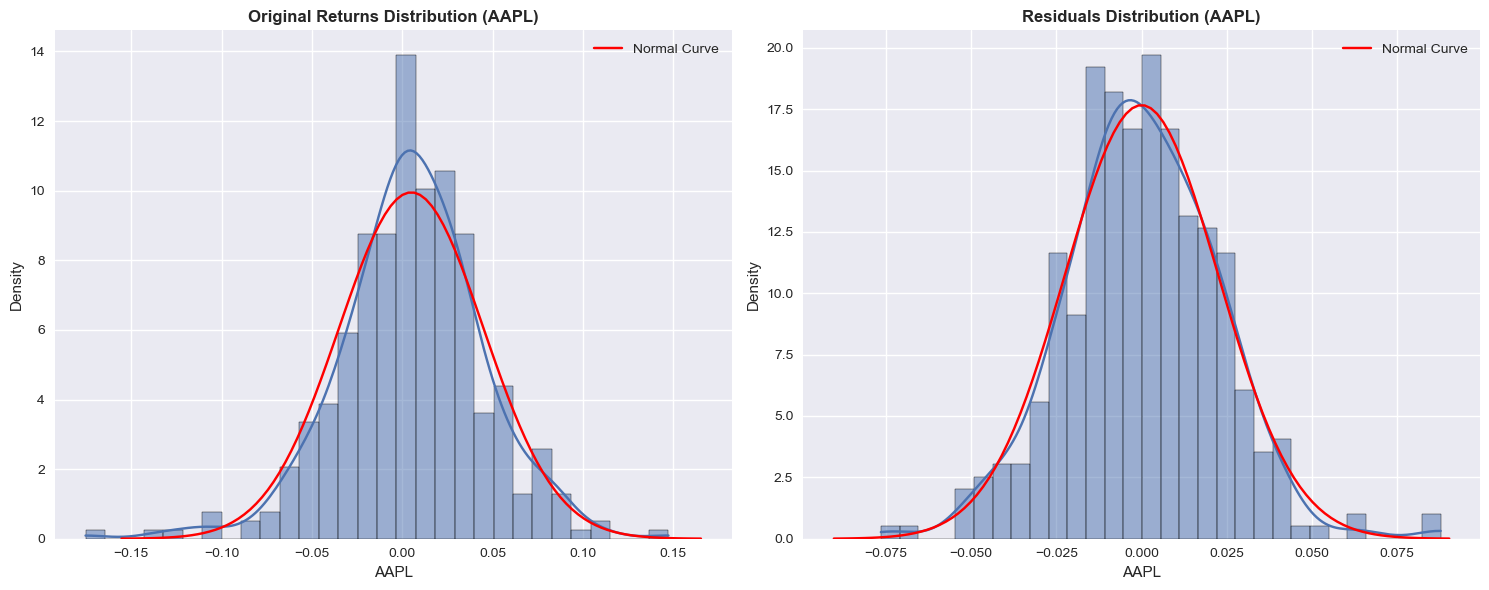

# Distribution comparison: Original vs Residuals

fig, (ax1, ax2) = plt.subplots(1, 2, figsize=(15, 6))

# Original returns distribution

sns.histplot(stocks['AAPL'], kde=True, stat="density", bins=30, ax=ax1)

mean = stocks['AAPL'].mean()

std = stocks['AAPL'].std()

x = np.linspace(mean - 4 * std, mean + 4 * std, 100)

ax1.plot(x, stats.norm.pdf(x, mean, std), label="Normal Curve", color="red")

ax1.set_title("Original Returns Distribution (AAPL)", fontweight='bold')

ax1.legend()

# Residuals distribution

sns.histplot(residuals['AAPL'], kde=True, stat="density", bins=30, ax=ax2)

mean = residuals['AAPL'].mean()

std = residuals['AAPL'].std()

x = np.linspace(mean - 4 * std, mean + 4 * std, 100)

ax2.plot(x, stats.norm.pdf(x, mean, std), label="Normal Curve", color="red")

ax2.set_title("Residuals Distribution (AAPL)", fontweight='bold')

ax2.legend()

plt.tight_layout()

plt.show()

# Statistical tests for normality improvement

from scipy.stats import shapiro, jarque_bera, normaltest

# Test normality for a sample of stocks

sample_stocks = ['AAPL', 'MSFT', 'GOOGL', 'AMZN', 'TSLA']

normality_tests = []

for stock in sample_stocks:

if stock in stocks.columns:

# Original returns

orig_stats = {

'Shapiro-Wilk p-value': shapiro(stocks[stock])[1],

'Jarque-Bera p-value': jarque_bera(stocks[stock])[1],

'D\'Agostino p-value': normaltest(stocks[stock])[1]

}

# Residuals

resid_stats = {

'Shapiro-Wilk p-value': shapiro(residuals[stock])[1],

'Jarque-Bera p-value': jarque_bera(residuals[stock])[1],

'D\'Agostino p-value': normaltest(residuals[stock])[1]

}

normality_tests.append({

'Stock': stock,

'Original_Shapiro': orig_stats['Shapiro-Wilk p-value'],

'Residual_Shapiro': resid_stats['Shapiro-Wilk p-value'],

'Original_JB': orig_stats['Jarque-Bera p-value'],

'Residual_JB': resid_stats['Jarque-Bera p-value']

})

normality_df = pd.DataFrame(normality_tests)

normality_df

| Stock | Original_Shapiro | Residual_Shapiro | Original_JB | Residual_JB | |

|---|---|---|---|---|---|

| 0 | AAPL | 0.0001 | 0.0113 | 0.0000 | 0.0001 |

| 1 | MSFT | 0.0021 | 0.0000 | 0.0000 | 0.0000 |

| 2 | GOOGL | 0.0200 | 0.0000 | 0.0114 | 0.0000 |

| 3 | AMZN | 0.0015 | 0.0001 | 0.0002 | 0.0000 |

| 4 | TSLA | 0.0000 | 0.0000 | 0.0000 | 0.0000 |

# Quantify QQ plot improvements with summary statistics

qq_improvements = []

for stock in sample_stocks:

if stock in stocks.columns:

# Calculate theoretical quantiles for comparison

orig_quantiles = np.percentile(stocks[stock], np.linspace(0.1, 99.9, 100))

resid_quantiles = np.percentile(residuals[stock], np.linspace(0.1, 99.9, 100))

# Theoretical normal quantiles

theoretical_quantiles = stats.norm.ppf(np.linspace(0.1, 99.9, 100) / 100)

# Calculate deviations from normality

orig_deviation = np.mean(np.abs(orig_quantiles - theoretical_quantiles))

resid_deviation = np.mean(np.abs(resid_quantiles - theoretical_quantiles))

qq_improvements.append({

'Stock': stock,

'Original_Deviation': orig_deviation,

'Residual_Deviation': resid_deviation,

'Improvement_%': (1 - resid_deviation / orig_deviation) * 100

})

qq_df = pd.DataFrame(qq_improvements)

qq_df

| Stock | Original_Deviation | Residual_Deviation | Improvement_% | |

|---|---|---|---|---|

| 0 | AAPL | 0.7883 | 0.8010 | -1.6212 |

| 1 | MSFT | 0.7920 | 0.8061 | -1.7901 |

| 2 | GOOGL | 0.7873 | 0.8012 | -1.7632 |

| 3 | AMZN | 0.7852 | 0.7997 | -1.8535 |

| 4 | TSLA | 0.7485 | 0.7736 | -3.3470 |

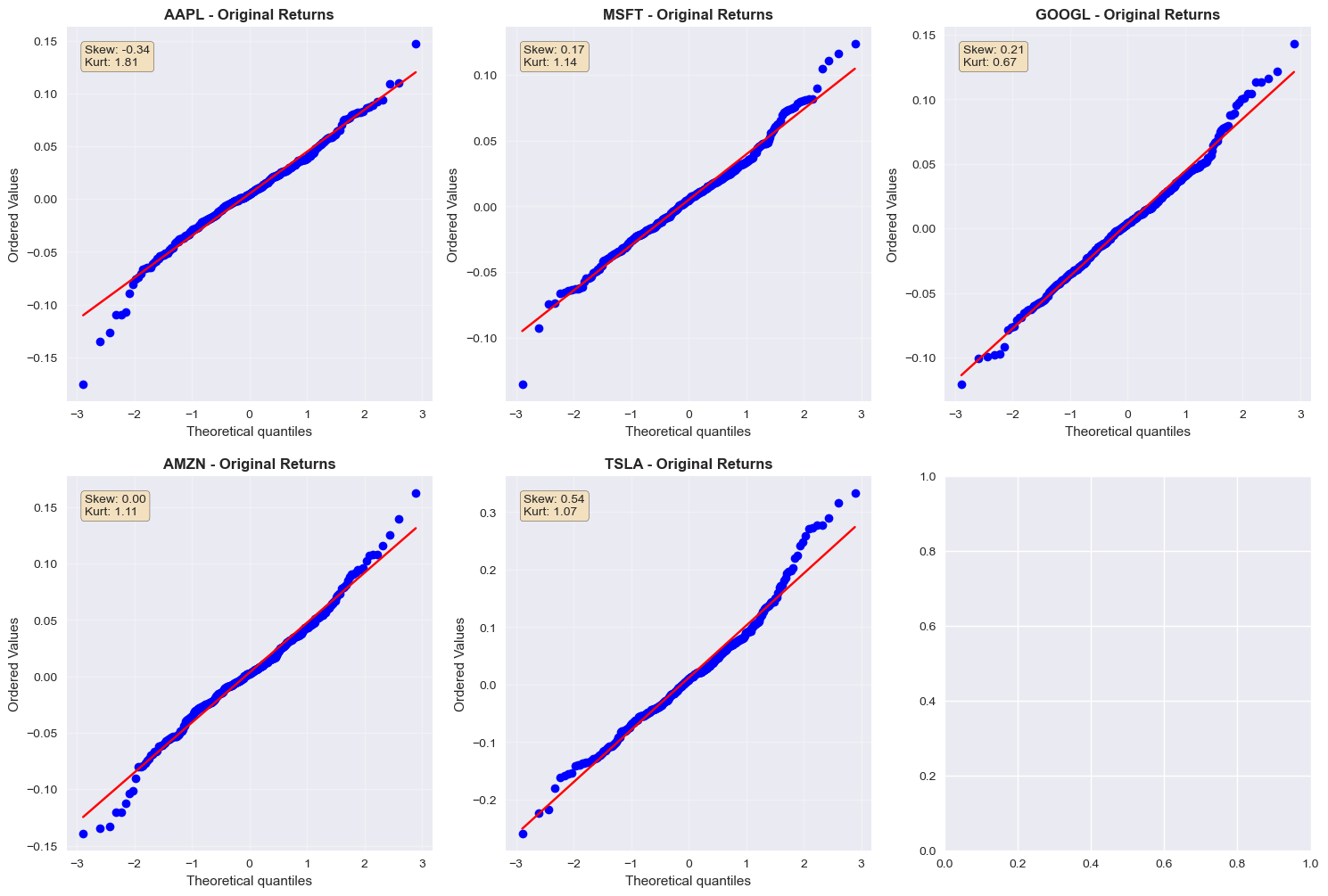

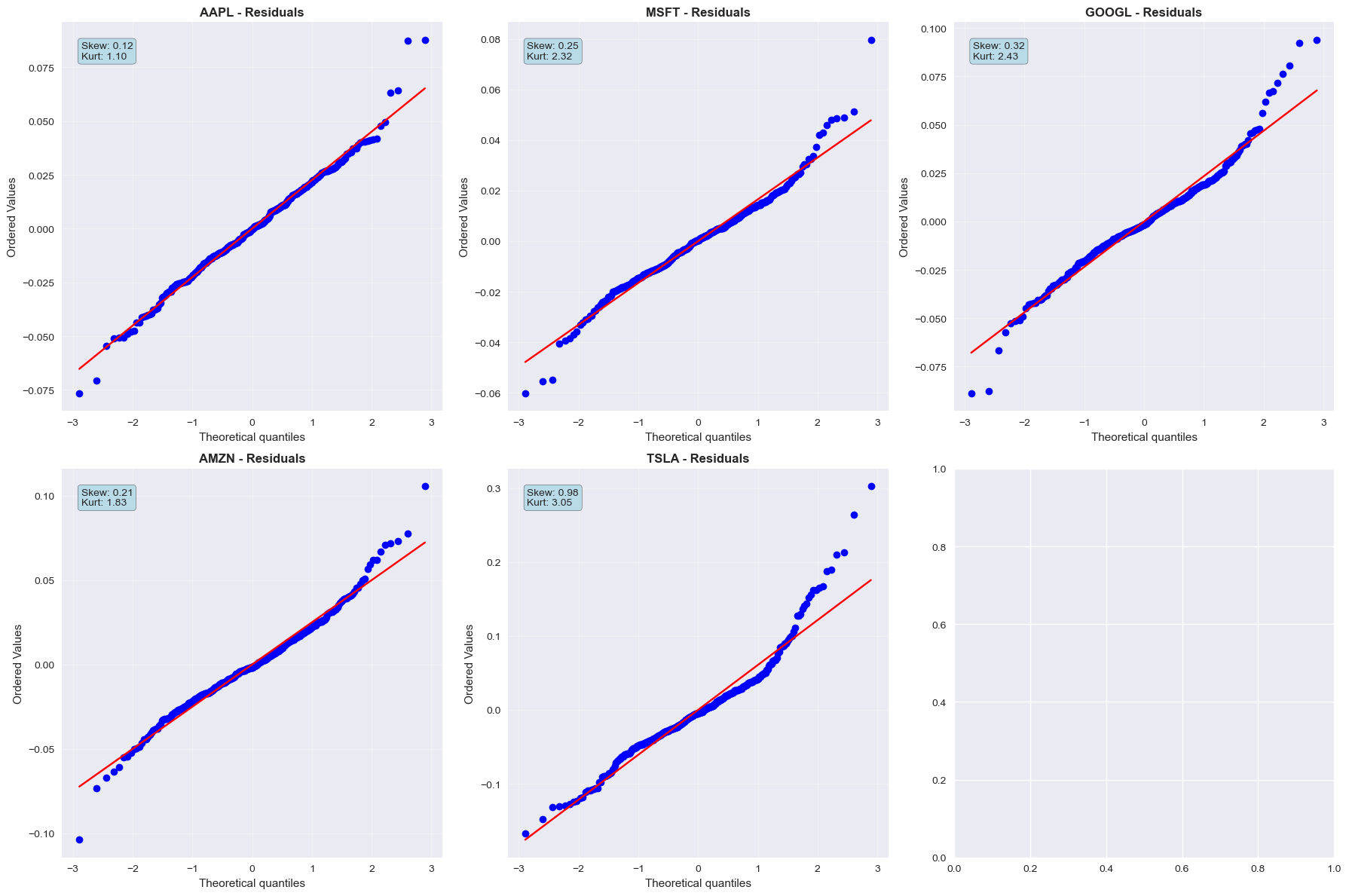

# Visual comparison of normality improvements

fig, axes = plt.subplots(2, 3, figsize=(18, 12))

axes = axes.flatten()

for i, stock in enumerate(sample_stocks[:6]):

if stock in stocks.columns and i < 6:

ax = axes[i]

# Create side-by-side QQ plots

stats.probplot(stocks[stock], dist="norm", plot=ax)

ax.set_title(f'{stock} - Original Returns', fontweight='bold')

ax.grid(True, alpha=0.3)

# Add statistics as text

orig_skew = stocks[stock].skew()

orig_kurt = stocks[stock].kurtosis()

ax.text(0.05, 0.95, f'Skew: {orig_skew:.2f}\nKurt: {orig_kurt:.2f}',

transform=ax.transAxes, verticalalignment='top',

bbox=dict(boxstyle='round', facecolor='wheat', alpha=0.8))

# Add residuals QQ plots

fig2, axes2 = plt.subplots(2, 3, figsize=(18, 12))

axes2 = axes2.flatten()

for i, stock in enumerate(sample_stocks[:6]):

if stock in residuals.columns and i < 6:

ax = axes2[i]

stats.probplot(residuals[stock], dist="norm", plot=ax)

ax.set_title(f'{stock} - Residuals', fontweight='bold')

ax.grid(True, alpha=0.3)

# Add statistics as text

resid_skew = residuals[stock].skew()

resid_kurt = residuals[stock].kurtosis()

ax.text(0.05, 0.95, f'Skew: {resid_skew:.2f}\nKurt: {resid_kurt:.2f}',

transform=ax.transAxes, verticalalignment='top',

bbox=dict(boxstyle='round', facecolor='lightblue', alpha=0.8))

plt.tight_layout()

plt.show()