Solution - Reversals#

Thanks to Anand Nakhate

1. Investigate Reversals#

Data#

Find monthly data on the long-term reversal factor.

LT Reversal (excess returns)deciles (total returns)

1.1.#

Report summary statistics for the reversal factor.

1.2.#

Report the summary statistics for the low and high decile from deciles (total returns).

Do you see evidence of differential performance?

Plot the cumulative return of each.

1.3.#

Does your answer to 1.2 change if we focus just on data since Jan 2001?

1.4.#

Staying with the later subsample, do you see evidence that the results are significantly impacted by small stocks?

Use size_sorts (total returns) to compare BIG LoPRIOR to BIG HiPRIOR.

1.#

KEY = 'REV'

TAG_LONG = 'Lo'

TAG_SHORT = 'Hi'

YR_CUTOFF = '2001'

YR_LAST_PRIOR_CUTOFF = '2000'

periods = [['1927', '2025'], ['1927', YR_LAST_PRIOR_CUTOFF], [YR_CUTOFF, '2025']]

FILE_PATH = '../data/reversal_data.xlsx'

SHEET_factors = 'FF factors (excess returns)'

SHEET_momentum = 'LT Reversal (excess returns)'

SHEET_deciles = 'deciles (total returns)'

SHEET_size_sorts = 'size_sorts (total returns)'

SHEET_rf = 'risk-free rate'

ANN_SCALE = 12

from functools import partial

import pandas as pd

import numpy as np

import seaborn as sns

import statsmodels.api as sm

import matplotlib.pyplot as plt

plt.style.use('ggplot')

import sys

if '../cmds/' not in sys.path:

sys.path.append('../cmds/')

from portfolio_management_helper import *

import warnings

warnings.filterwarnings("ignore")

raw_data = pd.read_excel(FILE_PATH,sheet_name = None)

ff_factors = raw_data[SHEET_factors].set_index('Date')

momentum = raw_data[SHEET_momentum].set_index('Date')

mom_deciles = raw_data[SHEET_deciles].set_index('Date')

tercile_port = raw_data[SHEET_size_sorts].set_index('Date')

rf = raw_data[SHEET_rf].set_index('Date')

ff_factors[KEY] = momentum[KEY]

1.1.#

summary_col_names = ['Annualized Mean','Annualized Vol','Annualized Sharpe','Skewness']

res = []

for period in periods:

temp = momentum.loc[period[0]:period[1]]

temp_ff = ff_factors.loc[period[0]:period[1]]

summary = calc_summary_statistics(temp, annual_factor=ANN_SCALE, provided_excess_returns=True)[summary_col_names]

summary['mkt_corr'] = temp_ff.corr().loc['MKT',[KEY]]

summary['val_corr'] = temp_ff.corr().loc['HML',[KEY]]

summary = summary.T.iloc[:,0].rename(f'{period[0]} - {period[1]}')

res.append(summary)

summary = pd.concat(res, axis=1).T

summary.style.format('{:.1%}')

| Annualized Mean | Annualized Vol | Annualized Sharpe | Skewness | mkt_corr | val_corr | |

|---|---|---|---|---|---|---|

| 1927 - 2025 | 3.4% | 11.9% | 28.1% | 289.5% | 23.5% | 64.8% |

| 1927 - 2000 | 4.4% | 12.5% | 34.8% | 325.4% | 26.8% | 63.8% |

| 2001 - 2025 | 0.5% | 10.0% | 4.9% | 56.9% | 9.2% | 68.8% |

1.2.#

mom_long = (tercile_port[f'BIG {TAG_LONG}PRIOR'] + tercile_port[f'SMALL {TAG_LONG}PRIOR'])/2 - rf['RF']

mom_names = ['long_and_short','long_only']

temp = ff_factors.copy().rename(columns={f'{KEY}':'long_and_short'})

temp['long_only'] = mom_long

summary =calc_summary_statistics(

temp.loc[YR_CUTOFF:, mom_names], annual_factor=ANN_SCALE, provided_excess_returns=True,

keep_columns=summary_col_names

)

summary['mkt_corr'] = temp.loc[YR_CUTOFF:].corr().loc['MKT', mom_names]

summary['val_corr'] = temp.loc[YR_CUTOFF:].corr().loc['HML', mom_names]

summary.style.format('{:.1%}')

| Annualized Mean | Annualized Vol | Annualized Sharpe | Skewness | mkt_corr | val_corr | |

|---|---|---|---|---|---|---|

| long_and_short | 0.5% | 10.0% | 4.9% | 56.9% | 9.2% | 68.8% |

| long_only | 10.4% | 21.0% | 49.4% | -31.9% | 88.7% | 32.9% |

1.3.#

fig, ax = plt.subplots(figsize=(8,5))

(100 * ((1 + temp[mom_names + ['MKT']].loc[YR_CUTOFF:]).cumprod() -1 )).plot(ax=ax)

ax.set_ylabel('Cumulative Returns (%)')

ax.set_title('Cumulative Returns')

Text(0.5, 1.0, 'Cumulative Returns')

1.4.#

ls_1decile = mom_deciles[f'{TAG_LONG} PRIOR'] - mom_deciles[f'{TAG_SHORT} PRIOR']

ls_3decile = mom_deciles.iloc[:,-3:].mean(axis = 1) - mom_deciles.iloc[:,:3].mean(axis = 1)

ls_5decile = mom_deciles.iloc[:,-5:].mean(axis = 1) - mom_deciles.iloc[:,:5].mean(axis = 1)

ls_names = ['mom_D1','mom_D3','mom_D5']

temp = ff_factors.copy()

temp[ls_names] = pd.concat([ls_1decile, ls_3decile, ls_5decile], axis=1)

summary = calc_summary_statistics(temp.loc[YR_CUTOFF:, ls_names + [KEY]], annual_factor=ANN_SCALE, provided_excess_returns=True)[summary_col_names]

summary['mkt_corr'] = temp.corr().loc['MKT', ls_names + [KEY]]

summary['val_corr'] = temp.corr().loc['HML', ls_names + [KEY]]

summary.style.format('{:.1%}')

| Annualized Mean | Annualized Vol | Annualized Sharpe | Skewness | mkt_corr | val_corr | |

|---|---|---|---|---|---|---|

| mom_D1 | -1.2% | 20.5% | -5.9% | 26.8% | 20.0% | 60.6% |

| mom_D3 | 0.1% | 12.7% | 0.5% | -36.0% | -24.7% | -62.3% |

| mom_D5 | 0.7% | 8.8% | 8.2% | -19.7% | -24.8% | -61.0% |

| REV | 0.5% | 10.0% | 4.9% | 56.9% | 23.5% | 64.8% |

mom_small = tercile_port[f'SMALL {TAG_LONG}PRIOR'] - tercile_port[f'SMALL {TAG_SHORT}PRIOR']

mom_large = tercile_port[f'BIG {TAG_LONG}PRIOR'] - tercile_port[f'BIG {TAG_SHORT}PRIOR']

mom_size_name = ['Small_stocks','Big_stocks']

temp = ff_factors.copy()

temp[mom_size_name] = pd.concat([mom_small, mom_large], axis=1)

summary = calc_summary_statistics(temp.loc[YR_CUTOFF:, [KEY] + mom_size_name], annual_factor=ANN_SCALE, provided_excess_returns=True)[summary_col_names]

summary['mkt_corr'] = temp.corr().loc['MKT', [KEY] + mom_size_name]

summary['val_corr'] = temp.corr().loc['HML', [KEY] + mom_size_name]

summary.rename({'UMD':'All_stocks'}).style.format('{:.1%}')

| Annualized Mean | Annualized Vol | Annualized Sharpe | Skewness | mkt_corr | val_corr | |

|---|---|---|---|---|---|---|

| REV | 0.5% | 10.0% | 4.9% | 56.9% | 23.5% | 64.8% |

| Small_stocks | 1.4% | 9.4% | 14.8% | 66.9% | 24.7% | 53.5% |

| Big_stocks | -0.4% | 12.6% | -3.4% | 73.7% | 18.5% | 63.5% |

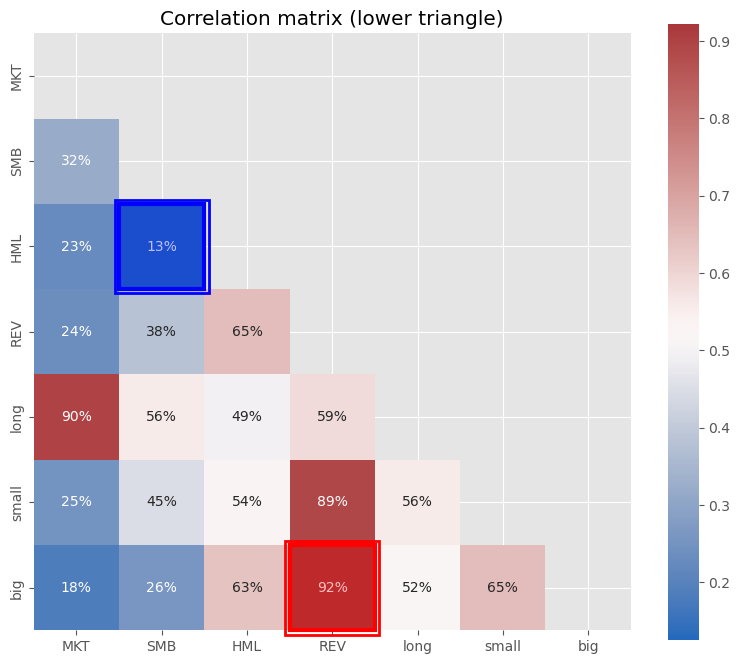

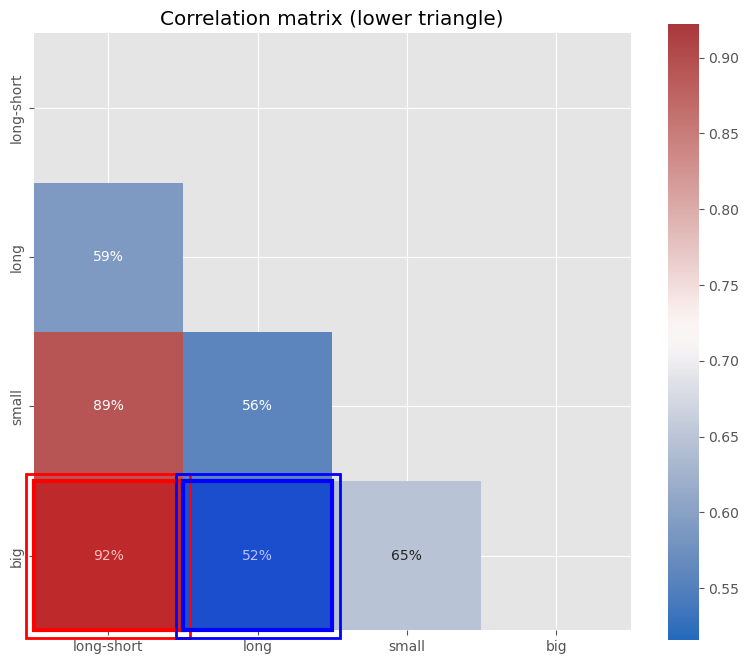

from cmds.plot_tools import plot_corr_matrix

temp = pd.concat([ff_factors[KEY], mom_long, mom_small, mom_large], axis=1)

temp.columns = ['long-short','long','small','big']

display(plot_corr_matrix(ff_factors,triangle='lower'));

display(plot_corr_matrix(temp,triangle='lower'));

(<Figure size 800x800 with 2 Axes>,

<Axes: title={'center': 'Correlation matrix (lower triangle)'}>)

(<Figure size 800x800 with 2 Axes>,

<Axes: title={'center': 'Correlation matrix (lower triangle)'}>)

display(plot_corr_matrix(pd.concat([ff_factors,temp.iloc[:,1:]],axis=1),triangle='lower'));

(<Figure size 800x800 with 2 Axes>,

<Axes: title={'center': 'Correlation matrix (lower triangle)'}>)