Solution - VaR#

Data#

This problem uses weekly return data from data/spx_returns_weekly.xlsx.

Choose any 4 stocks to evaluate below.

For example,

AAPLMETANVDATSLA

1 Diversification#

1.1#

Using the full sample, calculate for each series the (unconditional)

volatility

empirical VaR (.05)

empirical CVaR (.05)

Recall that by empirical we refer to the direct quantile estimation. (For example, using .quantile() in pandas.

1.2#

Form an equally-weighted portfolio of the investments.

Calculate the statistics of 1.1 for this portfolio, and compare the results to the individual return statistics. What do you find? What is driving this result?

1.3#

Re-calculate 1.2, but this time drop your most volatile asset, and replace the portion it was getting with 0. (You could imagine we’re replacing the most volatile asset with a negligibly small risk-free rate.)

In comparing the answer here to 1.2, how much risk is your most volatile asset adding to the portfolio? Is this in line with the amount of risk we measured in the stand-alone risk-assessment of 1.1?

2. Dynamic Measures#

2.1#

Let’s measure the conditional statistics of the equally-weighted portfolio of 1.2, as of the end of the sample.

Volatility#

For each security, calculate the rolling volatility series, \(\sigma_t\), with a window of \(m=26\).

The value at \(\sigma_t\) in the notes denotes the estimate using data through time \(t-1\), and thus (potentially) predicting the volatility at \(\sigma_{t}\).

Mean#

Suppose we can approximate that the daily mean return is zero.

VaR#

Calculate the normal VaR and normal CVaR for \(q=.05\) and \(\tau=1\) as of the end of the sample.Use the approximation, \(\texttt{z}_{.05} = -1.65\).

Notation Note#

In this setup, we are using a forecasted volatility, \(\sigma_t\) to estimate the VaR return we would have estimated at the end of \(t-1\) in prediction of time \(t\).

Conclude and Compare#

Report

volatility (annualized).

normal VaR (.05)

normal CVaR (.05)

How do these compare to the answers in 1.2?

2.2#

Backtest the VaR using the hit test. Namely, check how many times the realized return at \(t\) was smaller than the VaR return calculated using \(\sigma_t\), (where again remember the notation in the notes uses \(\sigma_t\) as a vol based on data through \(t-1\).)

Report the percentage of “hits” using both the

expanding volatility

rolling volatility

Solutions#

import pandas as pd

import numpy as np

import datetime

import warnings

import matplotlib.pyplot as plt

%matplotlib inline

plt.rcParams['figure.figsize'] = (12,6)

plt.rcParams['font.size'] = 15

plt.rcParams['legend.fontsize'] = 13

from matplotlib.ticker import (MultipleLocator,

FormatStrFormatter,

AutoMinorLocator)

import sys

sys.path.insert(0,'../cmds')

from portfolio import *

from risk import *

Solution 1#

LOADFILE = '../data/spx_returns_weekly.xlsx'

TICKS = [

'AAPL',

'META',

'NVDA',

'TSLA'

]

FREQ = 52

WINDOW = 26

QUANTILE = .05

mu = 0

SHEET = 's&p500 rets'

rets = pd.read_excel(LOADFILE,sheet_name=SHEET).set_index('date')

rets = rets[TICKS]

rets.dropna(inplace=True)

ANNUALIZE = np.sqrt(252)

rtab = rets.copy()

TICK_MAX_VOL = rets.std().idxmax()

rtab['portfolio'] = rtab.mean(axis=1)

rtab[f'portfolio-ex {TICK_MAX_VOL}'] = rtab.drop(columns=[TICK_MAX_VOL]).sum(axis=1)/4

rtab[f'stand-alone {TICK_MAX_VOL}'] = rtab[[TICK_MAX_VOL]]/4

risk0 = pd.DataFrame(index=['vol'],columns=rtab.columns,dtype=float)

risk0.loc['vol'] = rtab.std() * ANNUALIZE

risk0.loc[f'VaR {QUANTILE}'] = rtab.quantile(QUANTILE)

risk0.loc[f'CVaR {QUANTILE}'] = rtab[rtab<rtab.quantile(QUANTILE)].mean()

risk0.style.format('{:.2%}')

| AAPL | META | NVDA | TSLA | portfolio | portfolio-ex TSLA | stand-alone TSLA | |

|---|---|---|---|---|---|---|---|

| vol | 60.90% | 77.34% | 101.99% | 129.10% | 69.46% | 64.31% | 32.27% |

| VaR 0.05 | -5.64% | -7.00% | -8.69% | -11.74% | -6.19% | -5.58% | -2.93% |

| CVaR 0.05 | -8.31% | -10.32% | -11.65% | -14.78% | -8.50% | -8.06% | -3.70% |

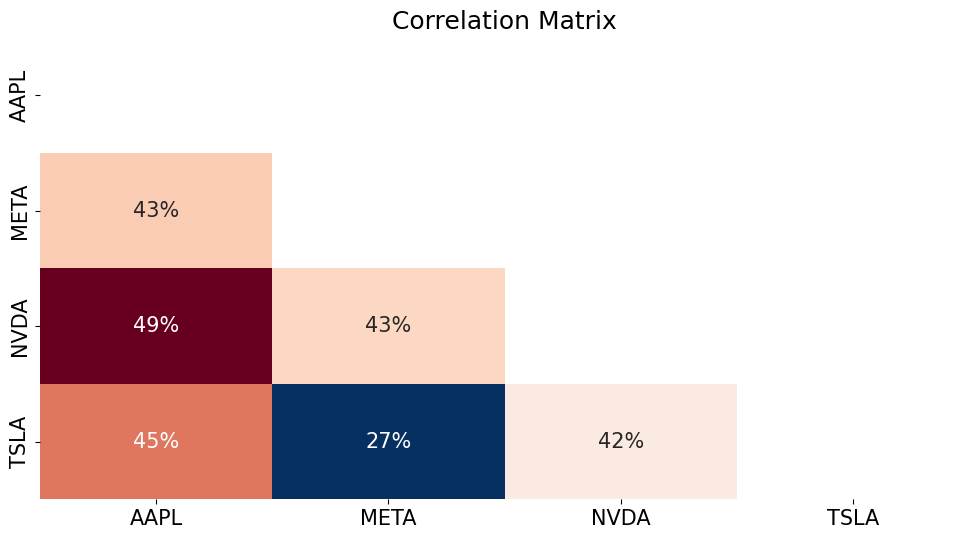

The explanation for this diversifiction is easiest seen for the case of volatility, which due to imperfect correlations, is strictly subadditive.

The relatively low correlations of the chosen futures contracts means the diversification effect is substantial.

Though VaR is not subadditive in general, it is in many specific cases, including here.

from matplotlib.colors import TwoSlopeNorm

corr_matrix = rets.corr()

# Set upper triangle and diagonal to NaN

mask = np.triu(np.ones_like(corr_matrix), k=0) # Using triu to get upper triangle including diagonal

corr_matrix[mask.astype(bool)] = np.nan

center = corr_matrix.mean().mean()

vmin = corr_matrix.min().min()

vmax = corr_matrix.max().max()

norm = TwoSlopeNorm(vmin=vmin, vcenter=center, vmax=vmax)

sns.heatmap(corr_matrix, annot=True, fmt='.0%', norm=norm, cmap='RdBu_r', cbar=False)

plt.title('Correlation Matrix')

plt.show()

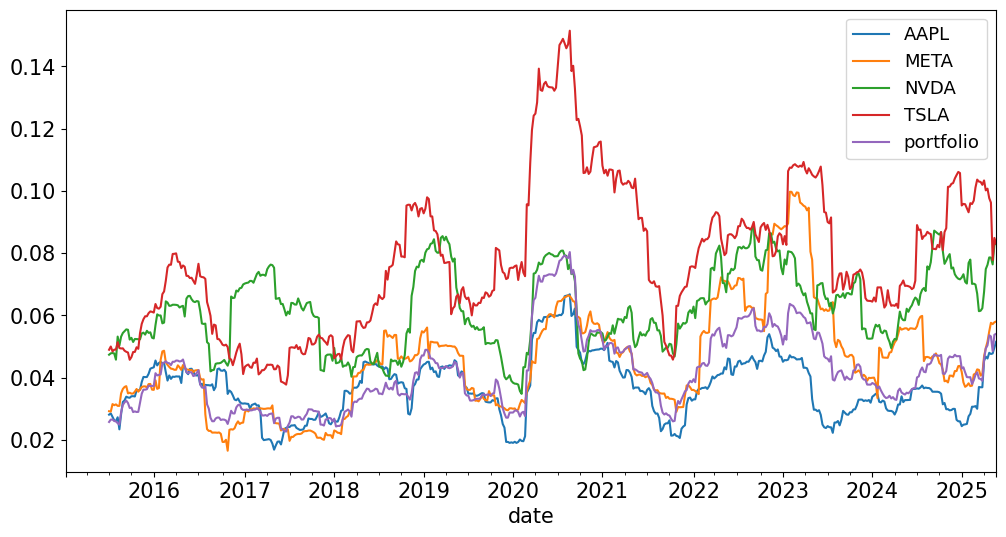

Solution 2#

method = 'rolling'

rets['portfolio'] = rets.mean(axis=1)

if method == 'rolling':

sigma = rets.rolling(WINDOW).std()

elif method == 'expanding':

sigma = rets.expanding(WINDOW).std()

sigma.plot();

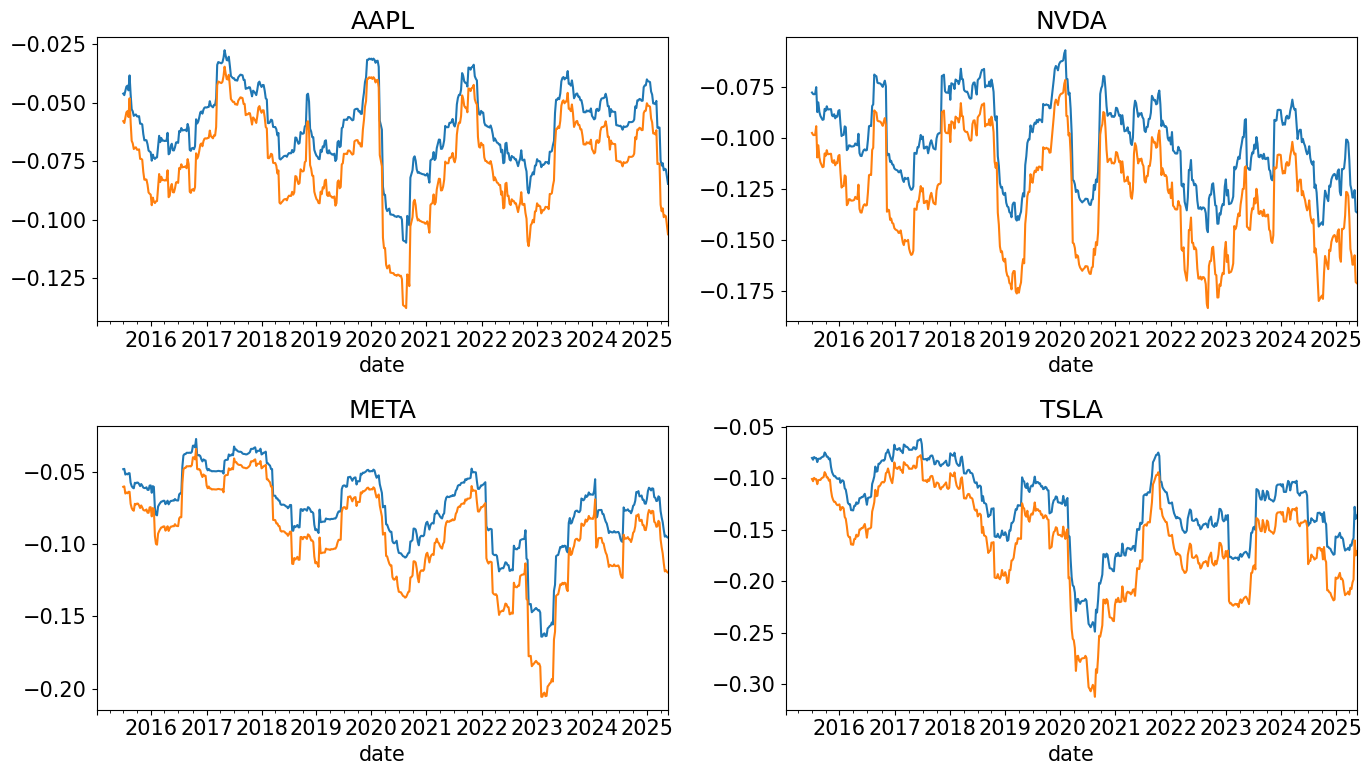

from scipy.stats import norm

zscore = norm.ppf(QUANTILE)

phi = norm.pdf(zscore)

VaRret = mu + zscore * sigma

CVaRret = mu - phi / QUANTILE * sigma

fig, ax = plt.subplots(2,2,figsize=(14,8))

for i,tick in enumerate(TICKS):

VaRret[tick].plot(ax=ax[i%2,int(np.floor(i/2))],title=f'{tick}')

CVaRret[tick].plot(ax=ax[i%2,int(np.floor(i/2))],title=f'{tick}')

plt.tight_layout()

tabcomp = risk0.iloc[1,:-2].to_frame('unconditional').join(VaRret.iloc[-1,:].to_frame('conditional'))

tabcvar = risk0.iloc[2,:-2].to_frame('unconditional').join(CVaRret.iloc[-1,:].to_frame('conditional'))

tabcomp = pd.concat([tabcomp,tabcvar],keys=['VaR','CVaR'],axis=1)

tabcomp.style.format('{:.1%}')

| VaR | CVaR | |||

|---|---|---|---|---|

| unconditional | conditional | unconditional | conditional | |

| AAPL | -5.6% | -8.5% | -8.3% | -10.6% |

| META | -7.0% | -9.5% | -10.3% | -12.0% |

| NVDA | -8.7% | -13.6% | -11.6% | -17.1% |

| TSLA | -11.7% | -13.7% | -14.8% | -17.1% |

| portfolio | -6.2% | -8.9% | -8.5% | -11.1% |

hits = rets < VaRret.shift()

(hits.sum()/hits.shape[0]).to_frame('Hit Ratio').style.format('{:.2%}')

| Hit Ratio | |

|---|---|

| AAPL | 4.98% |

| META | 4.24% |

| NVDA | 4.24% |

| TSLA | 4.98% |

| portfolio | 4.06% |