Solution - Open Midterm 1#

FINM 36700 - 2025#

UChicago Financial Mathematics#

Mark Hendricks

Data#

All data files are found in at the course web-book.

Scoring#

Problem |

Points |

|---|---|

1 |

70 |

2 |

30 |

Numbered problems are worth 5pts unless specified otherwise.

1. Portfolio Analysis#

Data#

Use the data in data/midterm_1_stock_returns.xlsx.

The returns are…

excess returns

weekly

through

May 2025

It has returns for

25single-name equitiesSPY

# Load packages, helper functions

import pandas as pd

import numpy as np

import matplotlib.pyplot as plt

import seaborn as sns

import statsmodels.api as sm

import helper_functions as pmh

import warnings

warnings.filterwarnings("ignore")

# Load data

DATAFILE_STOCKS = 'data/midterm_1_stock_returns.xlsx'

rets = pd.read_excel(DATAFILE_STOCKS, sheet_name='stock rets', index_col='date', parse_dates=['date'])

spy = pd.read_excel(DATAFILE_STOCKS, sheet_name='benchmark rets', index_col='date', parse_dates=['date'])

# Preview data

display(rets.head())

display(spy.tail())

| ADSK | AOS | BKNG | CBRE | CCI | CF | CHRW | DE | DGX | DTE | ... | MRK | MTD | PG | PNR | SBAC | STE | TTWO | VTRS | WM | WMT | |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| date | |||||||||||||||||||||

| 2015-01-09 | -0.021166 | -0.008927 | -0.078893 | -0.000577 | 0.026536 | 0.069378 | -0.024107 | -0.030450 | -0.003635 | -0.002414 | ... | 0.093897 | -0.008843 | -0.002101 | -0.023393 | -0.001091 | 0.013659 | -0.008009 | -0.009050 | -0.004251 | 0.040160 |

| 2015-01-16 | -0.024369 | -0.015313 | -0.041579 | -0.045022 | 0.012374 | 0.001515 | 0.019290 | 0.019265 | 0.019738 | 0.036405 | ... | 0.007512 | -0.024325 | 0.011081 | -0.009830 | -0.012042 | -0.020590 | 0.048080 | 0.002865 | 0.013778 | -0.028873 |

| 2015-01-23 | 0.023571 | 0.016282 | 0.029527 | -0.004231 | 0.050829 | 0.013841 | 0.009121 | 0.012027 | 0.016490 | 0.014229 | ... | -0.008567 | 0.037842 | -0.005804 | -0.003565 | 0.080951 | 0.023033 | 0.022253 | -0.031965 | 0.014548 | 0.020053 |

| 2015-01-30 | -0.071920 | 0.069487 | -0.027466 | -0.018513 | -0.003684 | 0.012031 | -0.039124 | -0.035766 | 0.002540 | -0.017317 | ... | -0.035366 | 0.002970 | -0.064277 | -0.033041 | -0.014190 | -0.014506 | -0.004689 | -0.019552 | -0.029622 | -0.039883 |

| 2015-02-06 | 0.056754 | 0.037577 | 0.012818 | 0.048856 | 0.001733 | -0.028619 | -0.009970 | 0.044489 | -0.020120 | -0.049186 | ... | -0.024717 | 0.016318 | 0.015660 | 0.040609 | 0.010108 | 0.026985 | -0.031460 | 0.013922 | 0.019639 | 0.027653 |

5 rows × 25 columns

| SPY | |

|---|---|

| date | |

| 2025-04-25 | 0.046029 |

| 2025-05-02 | 0.029275 |

| 2025-05-09 | -0.004270 |

| 2025-05-16 | 0.052911 |

| 2025-05-23 | -0.025395 |

1 Performance Stats#

1.1. Calculate the Sharpe ratio for each stock during the sample period#

Recall: the sample period ranges from January 2015 to December 2024 (inclusive).

Report the top 5 stocks with the highest Sharpe ratios.

# Define sample period

start_date, end_date = '2015-01-01', '2024-12-31'

sample_rets = rets[start_date:end_date]

# Calculate Sharpe ratios (annualized)

ANNUAL_FACTOR = 52

mean_ret, std_ret = sample_rets.mean() * ANNUAL_FACTOR, sample_rets.std() * (ANNUAL_FACTOR ** 0.5) # annualized

sharpe_ratios = pd.Series(mean_ret / std_ret, name = 'Sharpe Ratio')

sharpe_ranked = sharpe_ratios.sort_values(ascending=False)

# Display top 5 stocks

print("Top 5 Stocks by Sharpe Ratio:")

print(sharpe_ranked.head(5))

Top 5 Stocks by Sharpe Ratio:

WM 0.929781

GOOGL 0.854801

INTU 0.843681

TTWO 0.785463

WMT 0.773420

Name: Sharpe Ratio, dtype: float64

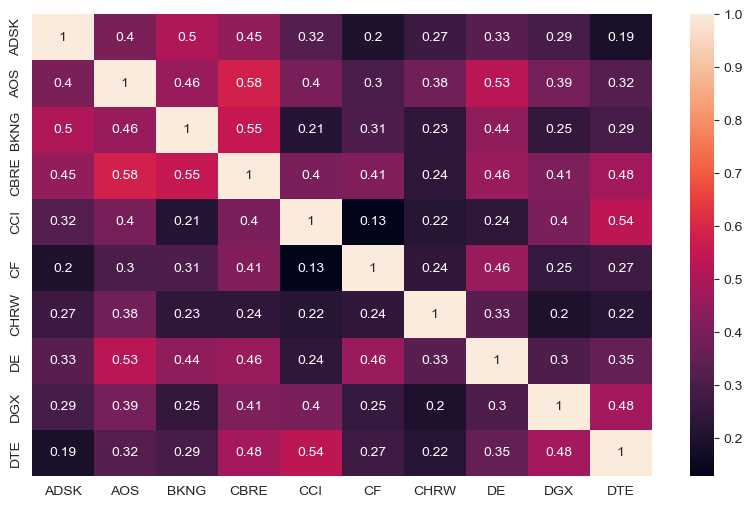

1.2. Display the correlation matrix for the first ten stocks (columns) over the sample period.#

On average, are these stocks highly correlated? Explain.

Which of these stocks offer the best diversification benefits?

There are multiple ways to determine which stocks offer the best diversification benefits. I consider the average pairwise correlations and find that CHRW, CF have substantially lower correlations than the other equities.

# Display correlation matrix

returns = sample_rets.iloc[:, :10].copy()

correlation_matrix = returns.corr()

fig, ax = plt.subplots(figsize=(10,6))

heatmap = sns.heatmap(

correlation_matrix,

xticklabels=correlation_matrix.columns,

yticklabels=correlation_matrix.columns,

annot=True,

)

heatmap; plt.show()

# Calculate average pairwise correlations for each stock

# Subtract the contribution of the diagonal = 1/10 in the average

corr_avg = correlation_matrix.mean() - (1 / len(correlation_matrix))

print("Average Pairwise Correlations:")

print(corr_avg.sort_values(ascending=True))

Average Pairwise Correlations:

CHRW 0.231889

CF 0.257515

CCI 0.284330

ADSK 0.294487

DGX 0.296499

DTE 0.314566

BKNG 0.324785

DE 0.344244

AOS 0.375968

CBRE 0.397587

dtype: float64

2. In-Sample Tangency (excess returns)#

Note#

Consider in-sample to be all the data through the end of 2024.

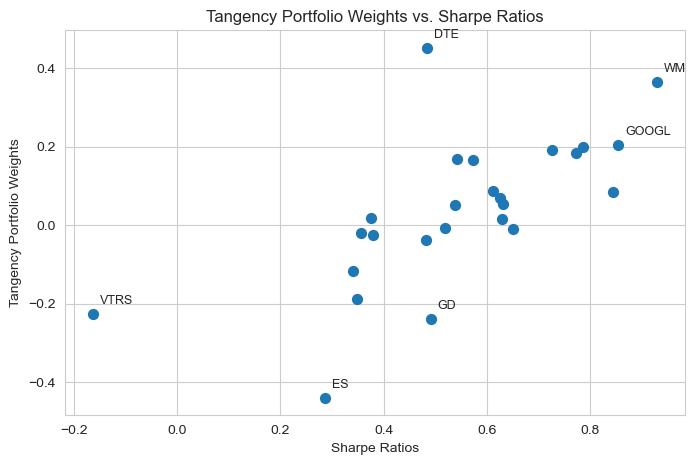

2.1. Construct the tangency portfolio#

Using just the in-sample data (through 2024), calculate the tangency portfolio weights, assuming we have excess returns (existence of a risk-free rate.)

Display the ten largest portfolio weights.

Plot the Sharpe ratios against the portfolio weights.

# Construct the tangency portfolio

tangency_wts = pmh.calc_tangency_weights(returns = sample_rets,

return_port_ret= False,

annual_factor = 52, # weekly data

name = 'Tangency',

expected_returns = None,

expected_returns_already_annualized = False)

# Display the ten largest weights

top_10_weights = tangency_wts['Tangency Weights'].sort_values(ascending=False).head(10)

print("Top 10 Tangency Portfolio Weights:")

print(top_10_weights)

# Plot Sharpe ratios vs. portfolio weights

fig, ax = plt.subplots(figsize=(8,5))

ax.scatter(sharpe_ratios, tangency_wts['Tangency Weights'], s=50)

ax.set_xlabel('Sharpe Ratios'); ax.set_ylabel('Tangency Portfolio Weights')

ax.set_title('Tangency Portfolio Weights vs. Sharpe Ratios')

ax.grid(True)

# label firms with large (absolute) weights >= 0.2 or <= -0.2

for name, wt in tangency_wts['Tangency Weights'].items():

if (wt >= 0.2) or (wt <= -0.2):

sr = sharpe_ratios.loc[name]

ax.annotate(

name, xy=(sr, wt), xytext=(5, 5), textcoords='offset points',

fontsize=9, ha='left', va='bottom')

plt.show()

Top 10 Tangency Portfolio Weights:

DTE 0.452431

WM 0.364931

GOOGL 0.205688

TTWO 0.198862

DE 0.191454

WMT 0.185139

MRK 0.168538

CBRE 0.167008

PG 0.087959

INTU 0.084542

Name: Tangency Weights, dtype: float64

2.2.#

Compare the relationship between tangency portfolio weights and individual sharpe ratios.

Mean variance optimization allocates higher (absolute) weight to assets with: (1) higher expected return, (2) lower volatility, and (3) lower covariances with other assets. Given that (1) and (2) directly determine the Sharpe ratio, there exists a positive relationship between the portfolio weights and Sharpe ratios.

# Regress weights on Sharpe ratios (empirical evidence of relationship)

X = sm.add_constant(sharpe_ratios)

y = tangency_wts['Tangency Weights']

model = sm.OLS(y, X).fit()

display(model.summary())

| Dep. Variable: | Tangency Weights | R-squared: | 0.440 |

|---|---|---|---|

| Model: | OLS | Adj. R-squared: | 0.416 |

| Method: | Least Squares | F-statistic: | 18.09 |

| Date: | Sun, 26 Oct 2025 | Prob (F-statistic): | 0.000300 |

| Time: | 20:38:50 | Log-Likelihood: | 13.499 |

| No. Observations: | 25 | AIC: | -23.00 |

| Df Residuals: | 23 | BIC: | -20.56 |

| Df Model: | 1 | ||

| Covariance Type: | nonrobust |

| coef | std err | t | P>|t| | [0.025 | 0.975] | |

|---|---|---|---|---|---|---|

| const | -0.2631 | 0.077 | -3.412 | 0.002 | -0.423 | -0.104 |

| Sharpe Ratio | 0.5563 | 0.131 | 4.253 | 0.000 | 0.286 | 0.827 |

| Omnibus: | 8.267 | Durbin-Watson: | 2.222 |

|---|---|---|---|

| Prob(Omnibus): | 0.016 | Jarque-Bera (JB): | 9.576 |

| Skew: | 0.528 | Prob(JB): | 0.00833 |

| Kurtosis: | 5.842 | Cond. No. | 5.82 |

Notes:

[1] Standard Errors assume that the covariance matrix of the errors is correctly specified.

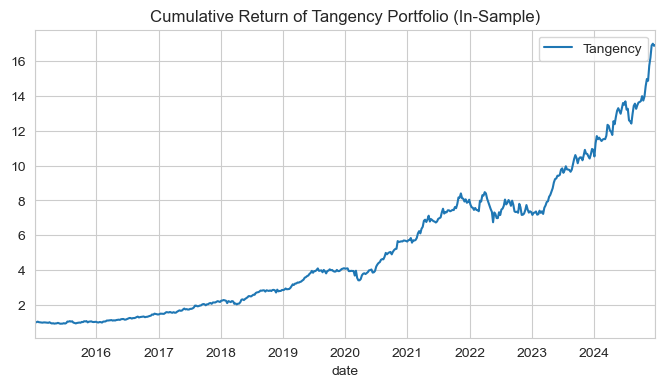

2.3. Performance of the Tangency#

Continue with the in-sample tangency portfolio constructed above, and analyze how it performs in-sample (through 2024.)

Report the (annualized)

mean

volatility

Sharpe ratio

skewness (not annualized)

Plot the cumulative return of the tangency portfolio over the sample period.

# Calculate expected return of tangency portfolio in-sample

portfolio_ret = pd.DataFrame(tangency_wts['Tangency Weights'] @ rets.T) # compute for all returns

portfolio_ret.columns = ['Tangency']

# Tangency portfolio statistics

tangency_stats = pd.DataFrame()

stat_names = ['Mean', 'Volatility', 'Sharpe Ratio', 'Skewness', 'Excess Kurtosis', 'Historical VaR 0.05', 'Historical CVaR 0.05']

tangency_stats['Tangency'] = pmh.stats(portfolio_ret[start_date:end_date], tail_risk_stats = True, annualization = 52)[stat_names].T

display(tangency_stats)

# plot cumulative return of tangency portfolio in-sample

cum_ret_in_sample = (portfolio_ret[start_date:end_date] + 1).cumprod()

cum_ret_in_sample.plot(figsize=(8,4), title='Cumulative Return of Tangency Portfolio (In-Sample)'); plt.show()

| Tangency | |

|---|---|

| Mean | 0.2993 |

| Volatility | 0.1811 |

| Sharpe Ratio | 1.6533 |

| Skewness | -0.0830 |

| Excess Kurtosis | -1.6122 |

| Historical VaR 0.05 | -0.0328 |

| Historical CVaR 0.05 | -0.0490 |

3. Hedging the Tangency Portfolio#

Continue with the in-sample (through 2024) tangency returns calculated in the previous problem.

3.1.#

Compute portfolio returns and regress on SPY to get \(\hat{\beta}\).

Include an intercept in the regression.

Report \(\hat{\beta}\).

# Regress tangency portfolio returns on SPY to get beta

spy_in_sample = spy[start_date:end_date]['SPY']

X = sm.add_constant(spy_in_sample)

y = portfolio_ret[start_date:end_date]['Tangency']

model = sm.OLS(y, X).fit()

beta_hat = model.params['SPY']

print(f"Estimated Beta: {beta_hat:.4f}")

Estimated Beta: 0.6048

3.2.#

Calculate the returns to the hedged position.

Report the (annualized)

mean

volatility

Sharpe ratio

skewness (not annualized)

Using the hedge ratio from the previous question \(\hat{\beta}\), hedged returns equal the tangency portfolio returns less the product of the hedge ratio and SPY returns.

# calculate hedged returns (tangency return

portfolio_ret['Hedged Tangency'] = portfolio_ret['Tangency'] - beta_hat * spy_in_sample

# Performance statistics

tangency_stats['Hedged Tangency'] = pmh.stats(portfolio_ret[['Hedged Tangency']].loc[start_date:end_date], tail_risk_stats = True, annualization = 52)[stat_names].T

display(tangency_stats)

| Tangency | Hedged Tangency | |

|---|---|---|

| Mean | 0.2993 | 0.2160 |

| Volatility | 0.1811 | 0.1499 |

| Sharpe Ratio | 1.6533 | 1.4404 |

| Skewness | -0.0830 | 0.1697 |

| Excess Kurtosis | -1.6122 | -1.9925 |

| Historical VaR 0.05 | -0.0328 | -0.0265 |

| Historical CVaR 0.05 | -0.0490 | -0.0393 |

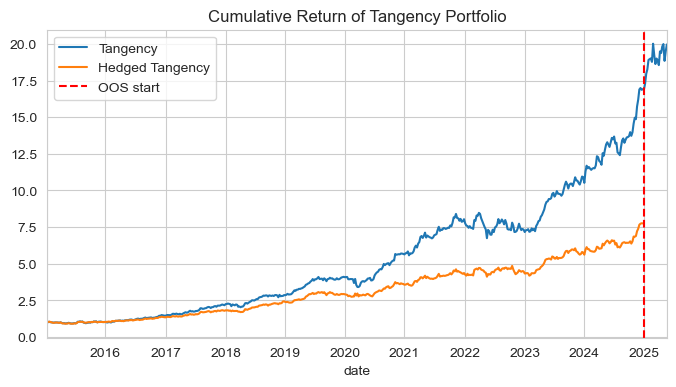

4. Out-of-Sample#

4.1. Tangency Portfolio Performance: Out-of-Sample (OOS)#

Use the weights of the tangency portfolio calculated above.

Compute the out-of-sample returns (2025), and just for this OOS portion, report the (annualized)

mean

volatility

Sharpe ratio

skewness (not annualized)

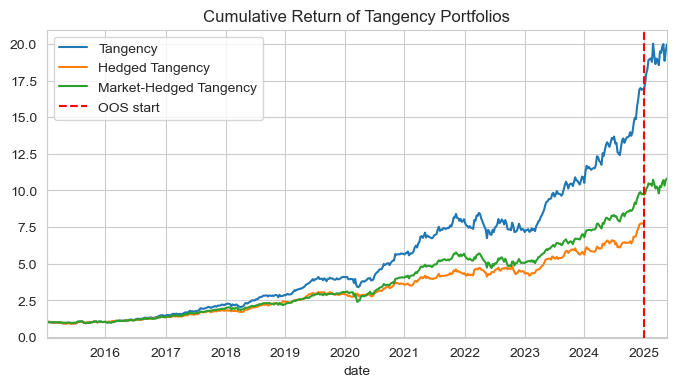

4.2. Cumulative performance#

Include the OOS performance in the cumulative return plot (in addition to the in-sample performance).

Show the plot.

# Calculate out-of-sample tangency portfolio returns

tangency_stats['Tangency OOS'] = pmh.stats(portfolio_ret[['Tangency']].loc[end_date:], tail_risk_stats = True, annualization = 52)[stat_names].T

display(tangency_stats)

# Cumulative performance plot including OOS

# add

cum_ret = (portfolio_ret + 1).cumprod()

ax = cum_ret.plot(figsize=(8,4), title='Cumulative Return of Tangency Portfolio')

ax.axvline(pd.to_datetime('2025-01-01'), color='red', linestyle='--', linewidth=1.5, label='OOS start')

ax.legend(); plt.show()

| Tangency | Hedged Tangency | Tangency OOS | |

|---|---|---|---|

| Mean | 0.2993 | 0.2160 | 0.4346 |

| Volatility | 0.1811 | 0.1499 | 0.2169 |

| Sharpe Ratio | 1.6533 | 1.4404 | 2.0034 |

| Skewness | -0.0830 | 0.1697 | -0.2853 |

| Excess Kurtosis | -1.6122 | -1.9925 | -2.9617 |

| Historical VaR 0.05 | -0.0328 | -0.0265 | -0.0391 |

| Historical CVaR 0.05 | -0.0490 | -0.0393 | -0.0482 |

5. Optimizing Hedged Returns#

5.1. Construct Market-Hedged Returns#

Active managers might optimize their portfolios using market-hedged returns to focus on alpha generation (maximize portion of returns orthogonal to the market). Market-hedged returns are the residuals from regressing each stock’s excess return on the market’s excess return (e.g., SPY), effectively removing market beta to isolate stock-specific (idiosyncratic) performance.

Regress each stock’s excess return on the SPY index (quoted in excess return) over the sample period.

Include an intercept.

Report your betas.

# RUN REGRESSIONS WITH FULL SAMPLE TO GIVE STUDENTS PARTIAL CREDIT IF NEEDED

# Regress each stock's excess return on SPY excess return (& constant) to get market-hedged returns

alphas, betas = pd.Series(index = rets.columns, name = 'Alpha'),pd.Series(index = rets.columns, name = 'Beta')

market_hedged_returns = pd.DataFrame(index=rets.index)

for stock in rets.columns:

tmp_regress = sm.OLS(rets[stock], sm.add_constant(spy)).fit()

alphas[stock] = tmp_regress.params[0]

betas[stock] = tmp_regress.params[1]

market_hedged_returns[stock] = tmp_regress.resid

# Display first 5 betas and alphas

print("Partial Credit: First 5 Betas and Alphas:")

display(pd.DataFrame([betas, alphas]).T.head(5))

# Regress each stock's excess return on SPY excess return (& constant) to get market-hedged returns

alphas, betas = pd.Series(index = sample_rets.columns, name = 'Alpha'),pd.Series(index = sample_rets.columns, name = 'Beta')

market_hedged_returns = pd.DataFrame(index=sample_rets.index)

for stock in sample_rets.columns:

tmp_regress = sm.OLS(sample_rets[stock], sm.add_constant(spy_in_sample)).fit()

alphas[stock] = tmp_regress.params[0]

betas[stock] = tmp_regress.params[1]

market_hedged_returns[stock] = tmp_regress.resid

# Display first 5 betas and alphas

print("Full Credit: First 5 Betas and Alphas:")

display(pd.DataFrame([betas, alphas]).T.head(5))

Partial Credit: First 5 Betas and Alphas:

| Beta | Alpha | |

|---|---|---|

| ADSK | 1.311552 | 0.000821 |

| AOS | 1.026381 | 0.000049 |

| BKNG | 1.254642 | 0.000682 |

| CBRE | 1.302287 | 0.000014 |

| CCI | 0.676221 | 0.000094 |

Full Credit: First 5 Betas and Alphas:

| Beta | Alpha | |

|---|---|---|

| ADSK | 1.346120 | 0.000717 |

| AOS | 1.050560 | -0.000041 |

| BKNG | 1.270031 | 0.000489 |

| CBRE | 1.325140 | 0.000017 |

| CCI | 0.737463 | -0.000341 |

5.2. The residuals#

Save the residuals from each regression as the market-hedged returns.

Report the .tail() (last 5 observations) of the residual dataframe.

# Market hedged returns as regression residuals

display(market_hedged_returns.tail(5))

| ADSK | AOS | BKNG | CBRE | CCI | CF | CHRW | DE | DGX | DTE | ... | MRK | MTD | PG | PNR | SBAC | STE | TTWO | VTRS | WM | WMT | |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| date | |||||||||||||||||||||

| 2024-11-29 | -0.108049 | 0.001919 | -0.010707 | 0.017987 | -0.000695 | -0.013378 | -0.026047 | 0.028463 | -0.015035 | 0.001000 | ... | 0.018365 | 0.013934 | 0.009785 | 0.004557 | 0.015754 | 0.010505 | -0.009923 | -0.028645 | 0.007773 | 0.015156 |

| 2024-12-06 | 0.041694 | -0.034368 | 0.009021 | -0.026658 | -0.047508 | -0.022482 | -0.000899 | -0.058154 | -0.039673 | -0.039778 | ... | 0.009273 | -0.004627 | -0.035752 | -0.018765 | -0.032963 | -0.023136 | -0.001839 | -0.032969 | -0.030388 | 0.028523 |

| 2024-12-13 | -0.005549 | 0.004611 | -0.006689 | 0.003625 | -0.026479 | 0.017587 | 0.059799 | -0.002645 | -0.010962 | 0.001563 | ... | -0.008723 | 0.021033 | -0.013159 | -0.000446 | -0.022560 | -0.002893 | -0.020556 | 0.002421 | -0.038362 | -0.011696 |

| 2024-12-20 | 0.005347 | -0.032718 | -0.011464 | -0.035024 | -0.052567 | -0.032651 | -0.052474 | 0.001304 | 0.001023 | 0.012541 | ... | -0.023388 | -0.016891 | -0.007943 | -0.024171 | -0.034588 | -0.015143 | -0.008179 | 0.012803 | -0.024570 | -0.013826 |

| 2024-12-27 | -0.011285 | -0.011038 | -0.011001 | 0.002711 | -0.005577 | -0.009409 | -0.008351 | -0.014287 | -0.008446 | 0.004969 | ... | 0.012862 | -0.004779 | 0.004561 | -0.015779 | -0.007017 | -0.004276 | 0.017208 | -0.005774 | -0.014627 | -0.011255 |

5 rows × 25 columns

5.3 Diversification Benefits of Market-Hedged Returns#

Display the covariance matrix of the market-hedged returns for the first ten stocks.

Note much lower correlations between market-hedged returns after we removed exposure to the broad market.

# Calculate and display correlation matrix for the first ten market-hedged returns

mh_returns = market_hedged_returns.iloc[:, :10].copy()

mh_cov_matrix = mh_returns.cov()

fig, ax = plt.subplots(figsize=(10,6))

mh_heatmap = sns.heatmap(

mh_cov_matrix,

xticklabels= mh_cov_matrix.columns,

yticklabels= mh_cov_matrix.columns,

annot=True,

)

mh_heatmap; plt.show()

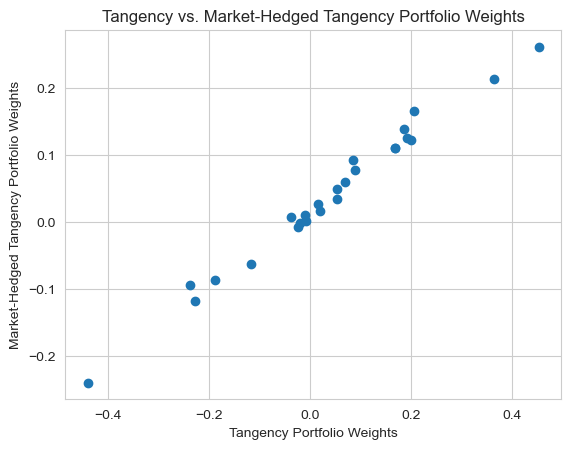

5.4. Portfolio Optimization with Market-Hedged Returns#

Construct the tangency portfolio using the alphas (intercept from previous regression) as expected returns and the covariance matrix of the market-hedged returns. Display the portfolio weights.

Market-hedged tangency weights are very similar, although the position sizes are more moderate, ranging from -0.2 to 0.2.

# Construct tangency portfolio using market-hedged returns

tangency_wts['Market-Hedged Tangency Weights'] = pmh.calc_tangency_weights(returns = market_hedged_returns,

cov_mat = 1, # covariance matrix estimated from return series

return_port_ret= False,

target_ret_rescale_weights = None,

annual_factor = ANNUAL_FACTOR, # monthly data

name = 'Market-Hedged Tangency',

expected_returns = alphas, # use alphas as expected returns

expected_returns_already_annualized = False)

print('Tangency Portfolio Weights using Market-Hedged Returns:')

display(tangency_wts.head())

# Compare with 'vanilla' tangency weights

plt.scatter(tangency_wts['Tangency Weights'], tangency_wts['Market-Hedged Tangency Weights'])

plt.xlabel('Tangency Portfolio Weights')

plt.ylabel('Market-Hedged Tangency Portfolio Weights')

plt.title('Tangency vs. Market-Hedged Tangency Portfolio Weights')

plt.grid(True)

plt.show()

Tangency Portfolio Weights using Market-Hedged Returns:

| Tangency Weights | Market-Hedged Tangency Weights | |

|---|---|---|

| ADSK | 0.015003 | 0.026741 |

| AOS | -0.008088 | 0.000448 |

| BKNG | 0.069375 | 0.058802 |

| CBRE | 0.167008 | 0.110415 |

| CCI | -0.118067 | -0.062549 |

5.5. Performance of the Tangency of the Hedged#

Calculate the returns to the portfolio with weights from the previous question (just in-sample).

Report the (annualized)

mean

volatility

Sharpe ratio

skewness (not annualized)

Note the difference between unhedged tangency portfolio, hedged tangency after the optimization portfolio, and the optimization with market-hedged returns portfolio.

# Calculate out-of-sample tangency portfolio returns

portfolio_ret['Market-Hedged Tangency'] = tangency_wts['Market-Hedged Tangency Weights'] @ rets.T # compute for all returns

tangency_stats['Market-Hedged Tangency'] = pmh.stats(portfolio_ret[['Market-Hedged Tangency']].loc[start_date:end_date], tail_risk_stats = True, annualization = 52)[stat_names].T

display(tangency_stats)

# Cumulative performance plot including OOS

cum_ret = (portfolio_ret + 1).cumprod()

ax = cum_ret.plot(figsize=(8,4), title='Cumulative Return of Tangency Portfolios')

ax.axvline(pd.to_datetime('2025-01-01'), color='red', linestyle='--', linewidth=1.5, label='OOS start')

ax.legend(); plt.show()

| Tangency | Hedged Tangency | Tangency OOS | Market-Hedged Tangency | |

|---|---|---|---|---|

| Mean | 0.2993 | 0.2160 | 0.4346 | 0.2406 |

| Volatility | 0.1811 | 0.1499 | 0.2169 | 0.1588 |

| Sharpe Ratio | 1.6533 | 1.4404 | 2.0034 | 1.5149 |

| Skewness | -0.0830 | 0.1697 | -0.2853 | -0.3642 |

| Excess Kurtosis | -1.6122 | -1.9925 | -2.9617 | -0.2062 |

| Historical VaR 0.05 | -0.0328 | -0.0265 | -0.0391 | -0.0286 |

| Historical CVaR 0.05 | -0.0490 | -0.0393 | -0.0482 | -0.0473 |

2. Managing Risk#

DATAFILE = 'data/midterm_1_fund_returns.xlsx'

df = pd.read_excel(DATAFILE, sheet_name='fund returns').set_index('date')

display(df.head())

| fund | |

|---|---|

| date | |

| 2015-01-09 | 0.003444 |

| 2015-01-16 | -0.000959 |

| 2015-01-23 | 0.004491 |

| 2015-01-30 | 0.010560 |

| 2015-02-06 | -0.001624 |

1. Calculating Volatility#

Given the return data provided, calculate the annual volatility grouped by year. Annualize this volatility. That is, your answer should be a DataFrame with 10 rows (one for each year from 2015 to 2024) and a single column representing the annualized volatility for that year.

What do you notice about the volatility across different years?

Volatility is higher in even years, and lower in odd years. Seems like in even years the volatility is around 20%, while in odd ones it is around 5%.FREQ = 52

annual_volatility = df["fund"].groupby(df.index.year).std() * np.sqrt(FREQ)

annual_volatility.to_frame(name="Annualized Volatility")

| Annualized Volatility | |

|---|---|

| date | |

| 2015 | 0.046374 |

| 2016 | 0.175849 |

| 2017 | 0.048981 |

| 2018 | 0.184665 |

| 2019 | 0.056721 |

| 2020 | 0.196581 |

| 2021 | 0.039123 |

| 2022 | 0.206772 |

| 2023 | 0.051441 |

| 2024 | 0.216405 |

2. Volatility Estimates#

Using the return data, compute the annualized volatility estimate as of the last data point using the following methods:

EWMA volatility with a half-life of 26 weeks.

Rolling window volatility with a window size of 52 weeks.

Note: do not specify a “min_periods” argument anywhere.

ewma_vol = df["fund"].ewm(halflife=26).std()

rolling_vol = df["fund"].rolling(window=52).std()

# Alternatively, using squared returns:

ewma_vol_sq = np.sqrt((df["fund"]**2).ewm(halflife=26).mean())

rolling_vol_sq = np.sqrt((df["fund"]**2).rolling(window=52).mean())

pd.DataFrame({

"EWMA Volatility": ewma_vol.iloc[-1:] * np.sqrt(FREQ),

"Rolling Volatility": rolling_vol.iloc[-1:] * np.sqrt(FREQ),

"EWMA Volatility (Squared Returns)": ewma_vol_sq.iloc[-1:] * np.sqrt(FREQ),

"Rolling Volatility (Squared Returns)": rolling_vol_sq.iloc[-1:] * np.sqrt(FREQ)

}).T

| date | 2024-12-27 |

|---|---|

| EWMA Volatility | 0.179730 |

| Rolling Volatility | 0.216405 |

| EWMA Volatility (Squared Returns) | 0.179708 |

| Rolling Volatility (Squared Returns) | 0.215108 |

3. Dynamic VaR estimates#

Using the return data, compute the 1-week 1% VaR as of the last data point in the series.

You should use two different volatility models to compute the VaR:

EWMA volatility with a half-life of 26 weeks.

Rolling-window volatility with a window of 52 weeks.

Empirical (expanding) VaR.

from scipy.stats import norm

VAR = 0.01

ewma_vol = df["fund"].ewm(halflife=26).std()

rolling_vol = df["fund"].rolling(window=52).std()

ewma_mean = df["fund"].ewm(halflife=26).mean()

rolling_mean = df["fund"].rolling(window=52).mean()

ewma_vol_sq = np.sqrt((df["fund"]**2).ewm(halflife=26).mean())

rolling_vol_sq = np.sqrt((df["fund"]**2).rolling(window=52).mean())

empirical_var = df["fund"].expanding().quantile(VAR)

z_score = norm.ppf(VAR)

ewma_var = z_score * ewma_vol.iloc[-1]

ewma_var_mean = ewma_mean.iloc[-1] + ewma_var

ewma_var_sq = z_score * ewma_vol_sq.iloc[-1]

rolling_var = z_score * rolling_vol.iloc[-1]

rolling_var_mean = rolling_mean.iloc[-1] + rolling_var

rolling_var_sq = z_score * rolling_vol_sq.iloc[-1]

empirical_var_last = empirical_var.iloc[-1]

pd.DataFrame(

{

"EWMA VaR": [ewma_var],

"EWMA VaR (Non-Zero Mean)": [ewma_var_mean],

"Rolling VaR": [rolling_var],

"Rolling VaR (Non-Zero Mean)": [rolling_var_mean],

"Empirical VaR": [empirical_var_last],

"EWMA VaR (Squared Returns)": [ewma_var_sq],

"Rolling VaR (Squared Returns)": [rolling_var_sq],

},

index=["1-Week 1% VaR"],

).T

| 1-Week 1% VaR | |

|---|---|

| EWMA VaR | -0.057982 |

| EWMA VaR (Non-Zero Mean) | -0.060833 |

| Rolling VaR | -0.069814 |

| Rolling VaR (Non-Zero Mean) | -0.072373 |

| Empirical VaR | -0.052816 |

| EWMA VaR (Squared Returns) | -0.057975 |

| Rolling VaR (Squared Returns) | -0.069395 |

4. Dynamic CVaR estimates#

Repeat Question 3, but instead compute the 1-week 1% Conditional VaR (CVaR) as of the last data point in the series using the same three methods.

empirical_cvar = df["fund"][df["fund"] <= empirical_var_last].mean()

ewma_cvar = -(norm.pdf(z_score) / VAR) * ewma_vol.iloc[-1]

ewma_cvar_mean = ewma_mean.iloc[-1] + ewma_cvar

ewma_cvar_sq = -(norm.pdf(z_score) / VAR) * ewma_vol_sq.iloc[-1]

rolling_cvar = -(norm.pdf(z_score) / VAR) * rolling_vol.iloc[-1]

rolling_cvar_mean = rolling_mean.iloc[-1] + rolling_cvar

rolling_cvar_sq = -(norm.pdf(z_score) / VAR) * rolling_vol_sq.iloc[-1]

pd.DataFrame(

{

"EWMA CVaR": [ewma_cvar],

"EWMA CVaR (Non-Zero Mean)": [ewma_cvar_mean],

"Rolling CVaR": [rolling_cvar],

"Rolling CVaR (Non-Zero Mean)": [rolling_cvar_mean],

"Empirical CVaR": [empirical_cvar],

"EWMA CVaR (Squared Returns)": [ewma_cvar_sq],

"Rolling CVaR (Squared Returns)": [rolling_cvar_sq],

},

index=["1-Week 1% CVaR"],

).T

| 1-Week 1% CVaR | |

|---|---|

| EWMA CVaR | -0.066428 |

| EWMA CVaR (Non-Zero Mean) | -0.069279 |

| Rolling CVaR | -0.079983 |

| Rolling CVaR (Non-Zero Mean) | -0.082543 |

| Empirical CVaR | -0.065762 |

| EWMA CVaR (Squared Returns) | -0.066420 |

| Rolling CVaR (Squared Returns) | -0.079504 |

5. Year Choice#

Suppose instead we were interested in our VaR estimates as of the end of 2023 (ie. use all data that is before 2024-01-01). Report your VaR (1-week, 1%) estimates using the same three methods as in Question 3, but now the last data point in 2023.

Hint: You can use df.loc[:'2023'] to filter the DataFrame to only include data up to the end of 2023.

ewma_vol_2023 = df.loc[:"2023", "fund"].ewm(halflife=26).std()

ewma_vol_sq_2023 = np.sqrt((df.loc[:"2023", "fund"]**2).ewm(halflife=26).mean())

rolling_vol_2023 = df.loc[:"2023", "fund"].rolling(window=52).std()

rolling_vol_sq_2023 = np.sqrt((df.loc[:"2023", "fund"]**2).rolling(window=52).mean())

empirical_var_2023 = df.loc[:"2023", "fund"].expanding().quantile(VAR)

ewma_mean_2023 = df.loc[:"2023", "fund"].ewm(halflife=26).mean()

rolling_mean_2023 = df.loc[:"2023", "fund"].rolling(window=52).mean()

ewma_var_2023 = z_score * ewma_vol_2023.iloc[-1]

ewma_var_mean_2023 = ewma_mean_2023.iloc[-1] + ewma_var_2023

ewma_var_sq_2023 = z_score * ewma_vol_sq_2023.iloc[-1]

rolling_var_2023 = z_score * rolling_vol_2023.iloc[-1]

rolling_var_mean_2023 = rolling_mean_2023.iloc[-1] + rolling_var_2023

rolling_var_sq_2023 = z_score * rolling_vol_sq_2023.iloc[-1]

empirical_var_2023_last = empirical_var_2023.iloc[-1]

pd.DataFrame(

{

"EWMA VaR (2023)": [ewma_var_2023],

"EWMA VaR (2023) (Non-Zero Mean)": [ewma_var_mean_2023],

"Rolling VaR (2023)": [rolling_var_2023],

"Rolling VaR (2023) (Non-Zero Mean)": [rolling_var_mean_2023],

"Empirical VaR (2023)": [empirical_var_2023_last],

"EWMA VaR (2023) (Squared Returns)": [ewma_var_sq_2023],

"Rolling VaR (2023) (Squared Returns)": [rolling_var_sq_2023],

},

index=["1-Week 1% VaR as of end 2023"],

).T

| 1-Week 1% VaR as of end 2023 | |

|---|---|

| EWMA VaR (2023) | -0.032412 |

| EWMA VaR (2023) (Non-Zero Mean) | -0.032674 |

| Rolling VaR (2023) | -0.016595 |

| Rolling VaR (2023) (Non-Zero Mean) | -0.016881 |

| Empirical VaR (2023) | -0.049635 |

| EWMA VaR (2023) (Squared Returns) | -0.032201 |

| Rolling VaR (2023) (Squared Returns) | -0.016448 |

6. Compare#

What do you notice about the VaR estimates compared to those from question 2.3?

The EWMA and rolling VaR estimates for the end of 2023 are much lower than those of 2024, which makes sense as normal var is proportional to volatility.

The empirical VaR estimate barely changes (from ~5.2% to 4.9%).

Additionally, the rolling VaR does the best, which makes sense given that it is not including any data from 2024, while the EWMA with a 26-week half-life, still includes data from 2024 (albeit with less than a quarter weight).