Solution to Smart Beta Factors#

1. READING#

Describe how each of the factors (other than MKT) is measured. That is, each factor is a portfolio of stocks–which stocks are included in the factor portfolio?

The factors are constructed using:

Size Factor (Small minus Big – SMB): Small cap minus big cap. Split stocks into 5 quantiles, long smallest quantile and short largest quantile (by market cap).

Value Factor (High minus Low – HML): High book-to-market ratio minus low book-to-market ratio. Split stocks into 5 quantiles, long highest quantile and short lowest quantile (by book-to-market ratio).

Quality Factor (Robust minus Weak – RMW): Robust operating profitability minus weak operating profitability. Split stocks into 5 quantiles, long highest quantile and short lowest quantile (by operating profitability).

Investment Factor (Conservative minus Aggressive – CMA): Conservative investment minus aggressive investment. Split stocks into 5 quantiles, long lowest quantile and short lowest highest (by investment).

Momentum (Up minus Down – UMD): Up minus down. Split stocks into 5 quantiles, long highest quantile and short lowest quantile (by returns in previous year).

Is the factor portfolio…

long-only

long-short

value-weighted

equally-weighted

Long Short.

What steps are taken in the factor construction to try to reduce the correlation between the factors?

Picking distinct metrics, going long-short (to represent low correlation with the market which is long only).

What is the point of figures 1-6?

Showing the difference in returns between the highest and lowest quantiles for the factors.

How is a “smart beta” ETF different from a traditional ETF?

From Page 9 of the case:

Smart beta ETFs are a combination of passive and active investing. Whereas a passive ETF tracks an index, and is almost always long-only, a smart beta ETF will track a factor index, and will thus be long-short. This is compared to just market cap weighted ETFs (passive).

Is it possible for all investors to have exposure to the “value” factor?

Not everyone can invest in the value factor simultaneously.

However, we can all invest in the market factor: the market, by definition, represents the portfolio of all investors combined.

Factors such as momentum, value, and size involve tilting away from the market by going long in certain stocks and shorting others. We cannot all be short certain stocks since the net buys and sells must equal the total shares outstanding.

In contrast, being long the market doesn’t require anyone to be short the market for it to make sense. We can all be long the market!

Thus, not everyone can be a momentum or value investor. Whatever premium is gained from these factors must be sustained by someone taking the opposite position.

How does factor investing differ from traditional diversification?

A factor investor believes that all risk-premium is related to a limited set of factors. Therefore, they see no reason to invest in particular assets, but only in the factors themselves.

Traditional diversification is done using assets. Factors investors can also use MV optimization and aim to diversify. Nonetheless, they will do it with factors (instead of individual stocks, bonds, currencies, etc…).

Footnote:#

If you need more info in how these factor portfolios are created, see Ken French’s website, and the follow- details:

https://mba.tuck.dartmouth.edu/pages/faculty/ken.french/Data_Library/f-f_5_factors_2x3.html

https://mba.tuck.dartmouth.edu/pages/faculty/ken.french/Data_Library/det_mom_factor.html

2. The Factors#

Data#

Use the data found in factor_pricing_data.xlsx.

FACTORS: Monthly excess return data for the overall equity market, \(\tilde{r}^{\text{MKT}}\).

The column header to the market factor is

MKTrather thanMKT-RF, but it is indeed already in excess return form.The sheet also contains data on five additional factors.

All factor data is already provided as excess returns

1.#

Analyze the factors, similar to how you analyzed the three Fama-French factors in Homework 4.

You now have three additional factors, so let’s compare there univariate statistics.

mean

volatility

Sharpe

MKT has the best annualized excess return, averaging 8% per year.

import pandas as pd

import numpy as np

import os

import sys

import seaborn as sns

from matplotlib.ticker import PercentFormatter

sns.set_style("whitegrid")

import matplotlib.pyplot as plt

#current_dir = os.getcwd()

#parent_dir = os.path.abspath(os.path.join(current_dir, os.pardir))

#sys.path.insert(0, parent_dir)

import cmds.portfolio_management_helper as pmh

EXCEL_PATH = "../data/factor_pricing_data_monthly.xlsx"

FACTORS_SHEET_NUMBER = 1

FACTORS_DESCRIPTION_SHEET_NUMBER = 0

PORTFOLIOS_SHEET_NUMBER = 2

factors_excess_returns = pmh.read_excel_default(EXCEL_PATH, sheet_name=FACTORS_SHEET_NUMBER)

factors_excess_returns.tail(3)

| MKT | SMB | HML | RMW | CMA | UMD | |

|---|---|---|---|---|---|---|

| date | ||||||

| 2025-06-30 | 0.0486 | -0.0002 | -0.0160 | -0.0319 | 0.0145 | -0.0264 |

| 2025-07-31 | 0.0198 | -0.0015 | -0.0127 | -0.0029 | -0.0207 | -0.0096 |

| 2025-08-31 | 0.0185 | 0.0488 | 0.0441 | -0.0069 | 0.0207 | -0.0354 |

pmh.read_excel_default(EXCEL_PATH, sheet_name=FACTORS_DESCRIPTION_SHEET_NUMBER)

| Name | Unit | Construction | Description | |

|---|---|---|---|---|

| MKT | Market | Excess Return | Market-cap-weighted | US Equities |

| SMB | Size | Excess Return | Small Minus Big | Long small stocks and short big stocks |

| HML | Value | Excess Return | High Minus Low | Long value (high book-to-market) stocks and sh... |

| RMW | Profitability | Excess Return | Robust Minus Weak | Long profitability (income statement) and shor... |

| CMA | Investment | Excess Return | Conservative Minus Agressive | Long stocks with low (conservative) investment... |

| UMD | Momentum | Excess Return | Up Minus Down | Long stocks that have high recent returns and ... |

| RF | Risk-free rate | Total Return | Tbills | NaN |

(

pmh.calc_summary_statistics(

factors_excess_returns,

annual_factor=12,

provided_excess_returns=True,

keep_columns=["Annualized Mean", "Annualized Vol", "Annualized Sharpe"]

)

.sort_values('Annualized Sharpe', ascending=False)

)

| Annualized Mean | Annualized Vol | Annualized Sharpe | |

|---|---|---|---|

| MKT | 0.0876 | 0.1561 | 0.5607 |

| RMW | 0.0440 | 0.0829 | 0.5311 |

| UMD | 0.0603 | 0.1534 | 0.3933 |

| CMA | 0.0283 | 0.0725 | 0.3903 |

| HML | 0.0260 | 0.1088 | 0.2392 |

| SMB | 0.0061 | 0.1013 | 0.0604 |

pmh.calc_summary_statistics(

factors_excess_returns,

annual_factor=12,

provided_excess_returns=True,

timeframes={

"1980-2001": ["1980", "2001"],

"2002-2025": ["2002", "2025"],

},

keep_columns=["Annualized Mean", "Annualized Vol", "Annualized Sharpe"]

)

| Annualized Mean | Annualized Vol | Annualized Sharpe | |

|---|---|---|---|

| MKT 1980-2001 | 0.0835 | 0.1592 | 0.5242 |

| SMB 1980-2001 | 0.0028 | 0.1092 | 0.0257 |

| HML 1980-2001 | 0.0528 | 0.1110 | 0.4751 |

| RMW 1980-2001 | 0.0487 | 0.0912 | 0.5341 |

| CMA 1980-2001 | 0.0460 | 0.0772 | 0.5958 |

| UMD 1980-2001 | 0.1088 | 0.1497 | 0.7272 |

| MKT 2002-2025 | 0.0914 | 0.1535 | 0.5952 |

| SMB 2002-2025 | 0.0092 | 0.0935 | 0.0984 |

| HML 2002-2025 | 0.0012 | 0.1064 | 0.0113 |

| RMW 2002-2025 | 0.0397 | 0.0745 | 0.5326 |

| CMA 2002-2025 | 0.0118 | 0.0676 | 0.1749 |

| UMD 2002-2025 | 0.0152 | 0.1558 | 0.0976 |

2.#

Based on the factor statistics above, answer the following.

Does each factor have a positive risk premium (positive expected excess return)?

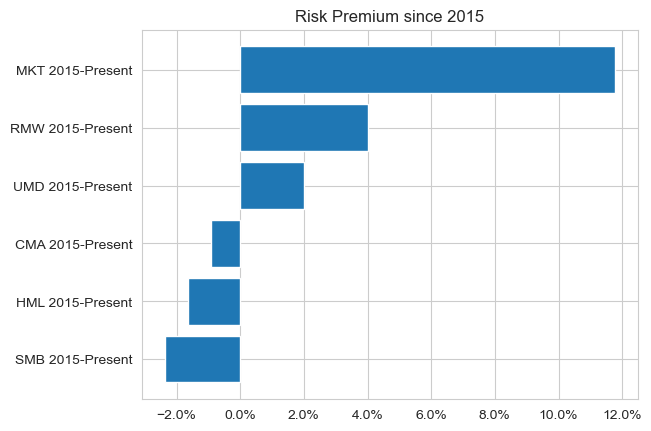

How have the factors performed since the time of the case, (2015-present)?

The same is true in the subsamples specified in HW4 (from 1980 to 2001 and 2002 to 2024). Nonetheless, from 2015 to 2024 HML (Value Factor) and SMB (Size Factor) had negative risk premium.

factors_recent_statistics = pmh.calc_summary_statistics(

factors_excess_returns,

annual_factor=12,

provided_excess_returns=True,

timeframes={

"2015-Present": ["2015", None],

},

keep_columns=["Annualized Mean", "Annualized Vol", "Annualized Sharpe"]

)

factors_recent_statistics.sort_values("Annualized Mean", inplace=True)

plt.barh(factors_recent_statistics.index, factors_recent_statistics['Annualized Mean'])

plt.gca().xaxis.set_major_formatter(PercentFormatter(1))

plt.title('Risk Premium since 2015')

plt.show();

factors_recent_statistics.sort_values("Annualized Mean", ascending=False)

| Annualized Mean | Annualized Vol | Annualized Sharpe | |

|---|---|---|---|

| MKT 2015-Present | 0.1179 | 0.1574 | 0.7491 |

| RMW 2015-Present | 0.0400 | 0.0726 | 0.5509 |

| UMD 2015-Present | 0.0201 | 0.1374 | 0.1464 |

| CMA 2015-Present | -0.0091 | 0.0821 | -0.1114 |

| HML 2015-Present | -0.0163 | 0.1299 | -0.1255 |

| SMB 2015-Present | -0.0238 | 0.1032 | -0.2305 |

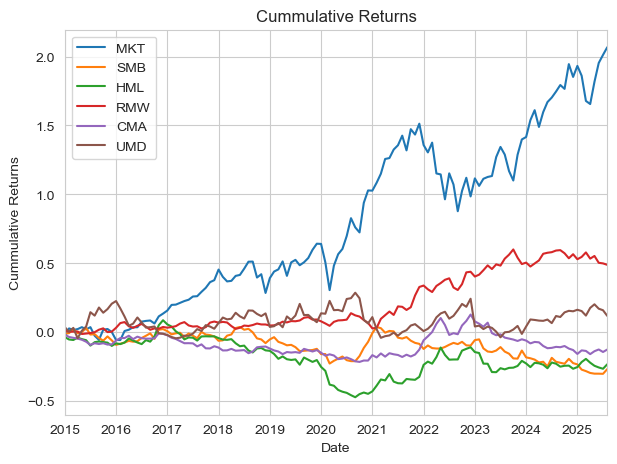

pmh.calc_cummulative_returns(factors_excess_returns.loc["2015":])

3.#

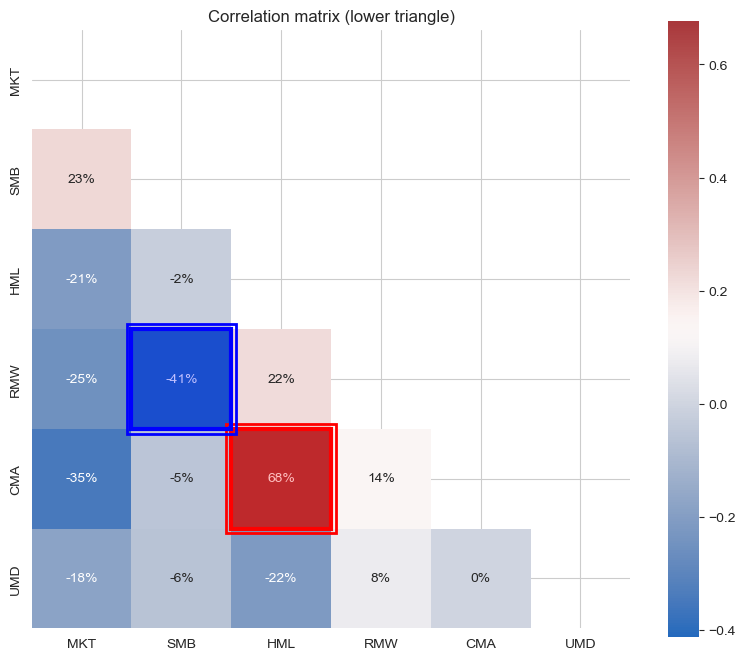

Report the correlation matrix across the six factors.

Does the construction method succeed in keeping correlations small?

Fama and French say that HML is somewhat redundant in their 5-factor model. Does this seem to be the case?

Fama and French correctly mentioned that HML is relatively redundant for the FF5: the correlation with CMA (Investment factor) is almost 70% and the correlation with RMW is 22%.

Nonetheless, one should be careful to drop HML. Prior to doing that, it is necessary to check the cross-sectional test with and without the Value factor and calculate the weights of the tangency portfolio. If HML shows relevant results, it should not be dropped and, thus, is not redundant.

from cmds.plot_tools import plot_corr_matrix

plot_corr_matrix(factors_excess_returns,triangle='lower')

plt.show()

4.#

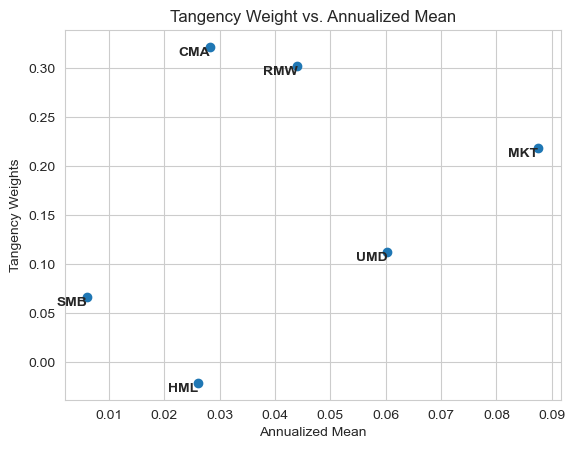

Report the tangency weights for a portfolio of these 6 factors.

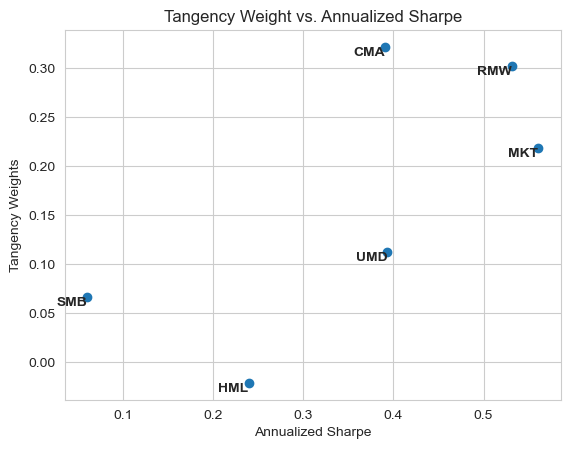

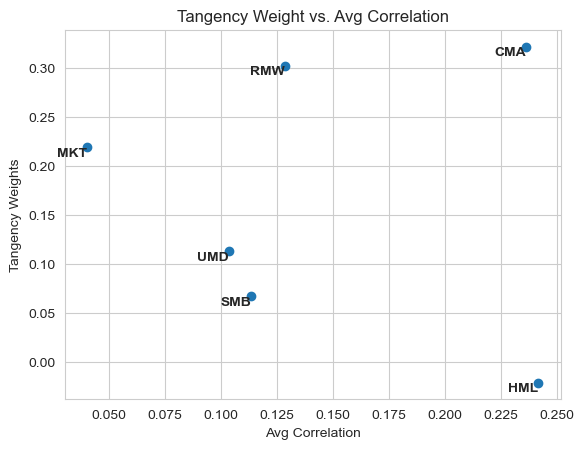

Which factors seem most important? And Least?

Are the factors with low mean returns still useful?

Re-do the tangency portfolio, but this time only include MKT, SMB, HML, and UMD. Which factors get high/low tangency weights now?

What do you conclude about the importance or unimportance of these styles?

The most important factors are CMA (Investment), RMW (Profitability) and MKT (Market).SMB and HML (Size and Value are the least important).

RMW has the second third lowest average return, nonetheless, it is among the most important. This happens due to its high Sharpe.

In the graphics above, we can also see that Market is not only weighted more heavily due to its good Sharpe but also due to its average correlation with other factors. While all other factors are long-short, Market is the only factor long-only, making it different from the rest.

Without using the factors of the FF5F, HML becomes drastically important, which agrees with the redundancy previously mentioned. Furthermore, the Sharpe of the tangency portfolio not using CMA and RMW and the tangency portfolio not using HML are statistically the same, pointing out that it is not clear that we should drop Value and prefer Investment and Profitability factors.

factors_tangency_weights = pd.concat([

pmh.calc_tangency_weights(factors_excess_returns),

pmh.calc_summary_statistics(

factors_excess_returns, annual_factor=12, provided_excess_returns=True,

keep_columns=["Annualized Sharpe", "Annualized Mean"]

)

], axis=1)

factors_tangency_weights.sort_values('Tangency Weights', ascending=False)

| Tangency Weights | Annualized Mean | Annualized Sharpe | |

|---|---|---|---|

| CMA | 0.3214 | 0.0283 | 0.3903 |

| RMW | 0.3018 | 0.0440 | 0.5311 |

| MKT | 0.2186 | 0.0876 | 0.5607 |

| UMD | 0.1125 | 0.0603 | 0.3933 |

| SMB | 0.0668 | 0.0061 | 0.0604 |

| HML | -0.0212 | 0.0260 | 0.2392 |

plt.plot(

factors_tangency_weights['Annualized Mean'],

factors_tangency_weights['Tangency Weights'],

marker='o', linestyle=''

)

for i, label in enumerate(factors_tangency_weights.index):

plt.text(

factors_tangency_weights['Annualized Mean'][i],

factors_tangency_weights['Tangency Weights'][i],

label,

fontweight='bold',

ha='right',

va='top'

)

plt.xlabel("Annualized Mean")

plt.ylabel("Tangency Weights")

plt.title("Tangency Weight vs. Annualized Mean")

plt.show();

plt.plot(

factors_tangency_weights['Annualized Sharpe'],

factors_tangency_weights['Tangency Weights'],

marker='o', linestyle=''

)

for i, label in enumerate(factors_tangency_weights.index):

plt.text(

factors_tangency_weights['Annualized Sharpe'][i],

factors_tangency_weights['Tangency Weights'][i],

label,

fontweight='bold',

ha='right',

va='top'

)

plt.xlabel("Annualized Sharpe")

plt.ylabel("Tangency Weights")

plt.title("Tangency Weight vs. Annualized Sharpe")

plt.show();

factors_tangency_weights_vs_corr = (

pd.concat([

pmh.calc_tangency_weights(factors_excess_returns),

pmh.calc_summary_statistics(

factors_excess_returns, annual_factor=12, provided_excess_returns=True,

keep_columns=["Annualized Sharpe", "Annualized Mean", "Corr"]

)

], axis=1)

.sort_values('Tangency Weights', ascending=False)

.assign(avg_correlation=lambda df: (

df.loc[:, [c for c in df.columns if c.endswith('Correlation')]].mean(axis=1)

))

.rename({'avg_correlation': 'Avg Correlation'}, axis=1)

.pipe(lambda df: pd.concat([df.iloc[:, :3], df["Avg Correlation"], df.iloc[:, 3:-1]], axis=1))

)

factors_tangency_weights_vs_corr.style.format('{:.1%}')

| Tangency Weights | Annualized Mean | Annualized Sharpe | Avg Correlation | MKT Correlation | SMB Correlation | HML Correlation | RMW Correlation | CMA Correlation | UMD Correlation | |

|---|---|---|---|---|---|---|---|---|---|---|

| CMA | 32.1% | 2.8% | 39.0% | 23.6% | -34.7% | -5.1% | 67.7% | 13.9% | 100.0% | 0.0% |

| RMW | 30.2% | 4.4% | 53.1% | 12.9% | -25.1% | -41.2% | 21.9% | 100.0% | 13.9% | 7.7% |

| MKT | 21.9% | 8.8% | 56.1% | 4.0% | 100.0% | 22.7% | -20.8% | -25.1% | -34.7% | -17.9% |

| UMD | 11.2% | 6.0% | 39.3% | 10.3% | -17.9% | -6.1% | -21.6% | 7.7% | 0.0% | 100.0% |

| SMB | 6.7% | 0.6% | 6.0% | 11.4% | 22.7% | 100.0% | -2.2% | -41.2% | -5.1% | -6.1% |

| HML | -2.1% | 2.6% | 23.9% | 24.2% | -20.8% | -2.2% | 100.0% | 21.9% | 67.7% | -21.6% |

plt.plot(

factors_tangency_weights_vs_corr['Avg Correlation'],

factors_tangency_weights_vs_corr['Tangency Weights'],

marker='o', linestyle=''

)

for i, label in enumerate(factors_tangency_weights_vs_corr.index):

plt.text(

factors_tangency_weights_vs_corr['Avg Correlation'][i],

factors_tangency_weights_vs_corr['Tangency Weights'][i],

label,

fontweight='bold',

ha='right',

va='top'

)

plt.xlabel("Avg Correlation")

plt.ylabel("Tangency Weights")

plt.title("Tangency Weight vs. Avg Correlation")

plt.show();

(

pd.concat([

pmh.calc_tangency_weights(factors_excess_returns.loc[:, ['MKT', 'SMB', 'HML', 'UMD']]),

pmh.calc_tangency_weights(factors_excess_returns),

], axis=1)

.set_axis(["Tangency Weights with 4 Factors", "Tangency Weights with 6 Factors"], axis=1)

)

| Tangency Weights with 4 Factors | Tangency Weights with 6 Factors | |

|---|---|---|

| MKT | 0.3765 | 0.2186 |

| SMB | -0.0512 | 0.0668 |

| HML | 0.3653 | -0.0212 |

| UMD | 0.3094 | 0.1125 |

| RMW | NaN | 0.3018 |

| CMA | NaN | 0.3214 |

pmh.calc_summary_statistics(

returns=[

pmh.calc_tangency_weights(

factors_excess_returns.loc[:, ['MKT', 'SMB', 'HML', 'UMD']], return_port_ret=True,

name="Tangency Portfolio with 4 Factors"

),

pmh.calc_tangency_weights(

factors_excess_returns, return_port_ret=True,

name="Tangency Portfolio with 6 Factors"

),

pmh.calc_tangency_weights(

factors_excess_returns.drop('HML', axis=1), return_port_ret=True,

name="Tangency Portfolio without HML"

),

],

annual_factor=12,

provided_excess_returns=True,

keep_columns=["Annualized Mean", "Annualized Vol", "Annualized Sharpe"]

)

| Annualized Mean | Annualized Vol | Annualized Sharpe | |

|---|---|---|---|

| Tangency Portfolio with 4 Factors Portfolio | 0.0608 | 0.0666 | 0.9138 |

| Tangency Portfolio with 6 Factors Portfolio | 0.0482 | 0.0401 | 1.2013 |

| Tangency Portfolio without HML Portfolio | 0.0482 | 0.0402 | 1.2003 |

3. Testing Modern LPMs#

Consider the following factor models:

CAPM: MKT

Fama-French 3F: MKT, SMB, HML

Fama-French 5F: MKT, SMB, HML, RMW, CMA

AQR: MKT, HML, RMW, UMD

We are not saying this is “the” AQR model, but it is a good illustration of their most publicized factors: value, momentum, and more recently, profitability.

For instance, for the AQR model is…

We will test these models with the time-series regressions. Namely, for each asset i, estimate the following regression to test the AQR model:

Data

PORTFOLIOS: Monthly excess return data on 49 equity portfolios sorted by their industry. Denote these as \(\tilde{r}^i\) , for \(n = 1, . . . , 49.\)

You do NOT need the risk-free rate data. It is provided only for completeness. The other two tabs are already in terms of excess returns.

portfolios_excess_returns = pmh.read_excel_default(EXCEL_PATH, sheet_name=PORTFOLIOS_SHEET_NUMBER)

portfolios_excess_returns.tail()

| Agric | Food | Soda | Beer | Smoke | Toys | Fun | Books | Hshld | Clths | ... | Boxes | Trans | Whlsl | Rtail | Meals | Banks | Insur | RlEst | Fin | Other | |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| date | |||||||||||||||||||||

| 2025-04-30 | -0.0103 | -0.0214 | 0.0116 | -0.0616 | 0.0483 | -0.0671 | 0.1377 | 0.0164 | -0.0383 | -0.0801 | ... | -0.0179 | -0.0308 | 0.0163 | 0.0097 | -0.0299 | -0.0245 | -0.0851 | -0.0792 | -0.0054 | -0.0030 |

| 2025-05-31 | 0.1264 | -0.0326 | -0.0009 | -0.0382 | 0.0424 | 0.0517 | 0.0615 | 0.0380 | 0.0372 | 0.0989 | ... | 0.0211 | 0.0689 | 0.0200 | 0.0609 | 0.0330 | 0.0706 | -0.0499 | 0.0089 | 0.0752 | 0.0009 |

| 2025-06-30 | 0.0500 | -0.0170 | -0.0117 | -0.0201 | 0.0041 | 0.0627 | 0.0992 | 0.0327 | -0.0425 | 0.0167 | ... | 0.0143 | 0.0441 | 0.0121 | 0.0241 | 0.0162 | 0.0616 | -0.0028 | 0.1014 | 0.0819 | -0.0192 |

| 2025-07-31 | -0.0228 | -0.0072 | -0.0446 | 0.0304 | -0.0618 | 0.0147 | -0.0908 | -0.0367 | -0.0344 | 0.0216 | ... | -0.0076 | -0.0239 | -0.0020 | 0.0278 | -0.0285 | 0.0048 | -0.1008 | 0.1033 | 0.0415 | -0.0266 |

| 2025-08-31 | 0.0243 | -0.0025 | 0.0305 | 0.0311 | 0.0349 | 0.0651 | 0.0462 | 0.0531 | 0.0289 | 0.0387 | ... | 0.0161 | 0.0383 | 0.0116 | 0.0047 | 0.0050 | 0.0473 | 0.0711 | 0.0541 | -0.0058 | 0.0407 |

5 rows × 49 columns

Test the AQR 4-Factor Model using the time-series test. (We are not doing the cross-sectional regression tests.)

For each regression, report the estimated α and r-squared.

Calculate the mean-absolute-error of the estimated alphas.

If the pricing model worked, should these alpha estimates be large or small? Why?

Based on your MAE stat, does this seem to support the pricing model or not?

This should be the case because all risk premium of any asset should be associated with the risk of the pricing factors.

An alpha means that there is positive (or negative) excess return not associated with pricing factors.

In the time-series, the annualized MAE is 2.3%, which does not support the idea that the pricing model is able to capture all systematic risk.

This mean that, on average, assets have taken 2.3% excess return uncorrelated with any of the pricing factors.

AQR_FACTORS = ['MKT', 'HML', 'RMW', 'UMD']

aqr_time_series_test = pmh.calc_iterative_regression(

multiple_y=portfolios_excess_returns,

X=factors_excess_returns[AQR_FACTORS],

annual_factor=12,

warnings=False,

keep_columns=['Alpha', 'Annualized Alpha', 'R-Squared']

)

aqr_time_series_test

| Alpha | Annualized Alpha | R-Squared | |

|---|---|---|---|

| Agric | 0.0010 | 0.0117 | 0.3421 |

| Food | 0.0001 | 0.0015 | 0.4551 |

| Soda | 0.0013 | 0.0154 | 0.3025 |

| Beer | 0.0008 | 0.0099 | 0.4148 |

| Smoke | 0.0034 | 0.0411 | 0.2654 |

| Toys | -0.0028 | -0.0337 | 0.5102 |

| Fun | 0.0033 | 0.0391 | 0.6072 |

| Books | -0.0031 | -0.0367 | 0.6889 |

| Hshld | -0.0011 | -0.0127 | 0.5547 |

| Clths | -0.0019 | -0.0227 | 0.6190 |

| Hlth | -0.0034 | -0.0407 | 0.4409 |

| MedEq | 0.0014 | 0.0164 | 0.5958 |

| Drugs | 0.0021 | 0.0256 | 0.4894 |

| Chems | -0.0029 | -0.0351 | 0.7452 |

| Rubbr | -0.0004 | -0.0045 | 0.6453 |

| Txtls | -0.0031 | -0.0367 | 0.5470 |

| BldMt | -0.0024 | -0.0286 | 0.7525 |

| Cnstr | -0.0029 | -0.0353 | 0.6315 |

| Steel | -0.0027 | -0.0324 | 0.6283 |

| FabPr | -0.0024 | -0.0287 | 0.4245 |

| Mach | -0.0004 | -0.0053 | 0.7540 |

| ElcEq | -0.0004 | -0.0048 | 0.7372 |

| Autos | 0.0011 | 0.0127 | 0.5278 |

| Aero | -0.0006 | -0.0070 | 0.5994 |

| Ships | -0.0032 | -0.0389 | 0.5046 |

| Guns | 0.0003 | 0.0041 | 0.3245 |

| Gold | 0.0013 | 0.0151 | 0.0495 |

| Mines | -0.0016 | -0.0196 | 0.4589 |

| Coal | -0.0033 | -0.0396 | 0.2126 |

| Oil | -0.0024 | -0.0288 | 0.4556 |

| Util | 0.0003 | 0.0040 | 0.3614 |

| Telcm | 0.0005 | 0.0062 | 0.5804 |

| PerSv | -0.0041 | -0.0496 | 0.5848 |

| BusSv | -0.0007 | -0.0081 | 0.8463 |

| Hardw | 0.0035 | 0.0420 | 0.6669 |

| Softw | 0.0057 | 0.0684 | 0.7450 |

| Chips | 0.0053 | 0.0636 | 0.7498 |

| LabEq | 0.0017 | 0.0201 | 0.7279 |

| Paper | -0.0036 | -0.0430 | 0.6730 |

| Boxes | -0.0003 | -0.0041 | 0.5829 |

| Trans | -0.0019 | -0.0226 | 0.7088 |

| Whlsl | -0.0014 | -0.0166 | 0.7523 |

| Rtail | 0.0018 | 0.0211 | 0.6866 |

| Meals | -0.0002 | -0.0028 | 0.6371 |

| Banks | -0.0018 | -0.0211 | 0.7740 |

| Insur | -0.0013 | -0.0154 | 0.6612 |

| RlEst | -0.0043 | -0.0511 | 0.6054 |

| Fin | 0.0016 | 0.0197 | 0.8129 |

| Other | -0.0035 | -0.0422 | 0.5837 |

pmh.calc_cross_section_regression(

portfolios_excess_returns,

factors_excess_returns[AQR_FACTORS],

annual_factor=12,

keep_columns=["TS MAE", "TS Annualized MAE"],

provided_excess_returns=True,

)

Lambda represents the premium calculated by the cross-section regression and the historical premium is the average of the factor excess returns

| TS MAE | TS Annualized MAE | |

|---|---|---|

| MKT + HML + RMW + UMD Cross-Section Regression | 0.0021 | 0.0246 |

aqr_mae = aqr_time_series_test['Alpha'].abs().mean()

aqr_annualized_mae = aqr_time_series_test['Annualized Alpha'].abs().mean()

print(f"AQR Time-Series Average Absolute Alpha: {aqr_mae:.4f}")

print(f"AQR Time-Series Average Absolute Annualized Alpha: {aqr_annualized_mae:.4f}")

AQR Time-Series Average Absolute Alpha: 0.0021

AQR Time-Series Average Absolute Annualized Alpha: 0.0246

Test the CAPM, FF 3-Factor Model and the the FF 5-Factor Model.

Report the MAE statistic for each of these models and compare it with the AQR Model MAE.

Which model fits best?

The model able to explain the biggest percentage of the cross-section is the FF5F (41%), followed by the FF3 (37%) and the AQR (22%).

FACTOR_MODELS = {

'CAPM': ['MKT'],

'AQR': AQR_FACTORS,

'FF3': ['MKT', 'HML', 'SMB'],

'FF5': ['MKT', 'HML', 'SMB', 'RMW', 'CMA'],

# 'All Factors': ['MKT', 'HML', 'SMB', 'RMW', 'CMA', 'UMD'],

}

cross_sectional_tests = pd.DataFrame({})

for name, factors in FACTOR_MODELS.items():

cross_sectional_test = pmh.calc_cross_section_regression(

portfolios_excess_returns,

factors_excess_returns[factors],

annual_factor=12,

name=name,

provided_excess_returns=True,

)

cross_sectional_tests = pd.concat([cross_sectional_tests, cross_sectional_test])

(

cross_sectional_tests

.loc[:, lambda df: [c for c in df.columns if c.endswith('Eta') or c.endswith('MAE') or c == 'R-Squared']]

.sort_values('R-Squared', ascending=False)

)

Lambda represents the premium calculated by the cross-section regression and the historical premium is the average of the factor excess returns

Lambda represents the premium calculated by the cross-section regression and the historical premium is the average of the factor excess returns

Lambda represents the premium calculated by the cross-section regression and the historical premium is the average of the factor excess returns

Lambda represents the premium calculated by the cross-section regression and the historical premium is the average of the factor excess returns

| Eta | Annualized Eta | R-Squared | TS MAE | TS Annualized MAE | CS MAE | CS Annualized MAE | |

|---|---|---|---|---|---|---|---|

| FF5 Cross-Section Regression | 0.0050 | 0.0599 | 0.3765 | 0.0026 | 0.0314 | 0.0010 | 0.0120 |

| FF3 Cross-Section Regression | 0.0052 | 0.0627 | 0.3504 | 0.0020 | 0.0244 | 0.0010 | 0.0120 |

| AQR Cross-Section Regression | 0.0063 | 0.0755 | 0.2066 | 0.0021 | 0.0246 | 0.0011 | 0.0136 |

| CAPM Cross-Section Regression | 0.0069 | 0.0832 | 0.0093 | 0.0017 | 0.0210 | 0.0013 | 0.0152 |

Does any particular factor seem especially important or unimportant for pricing? Do you think Fama and French should use the Momentum Factor?

In both factor models in which it is included, it has ~10% of absolute average return.

For the FF3, the addition of momentum is particularly important. For the FF5 is not that important. We can validate that by adding the UMD factor to the FF5 and the FF3.

factor_models_tangency_weights = pd.DataFrame({})

for name, factors in FACTOR_MODELS.items():

factor_model_tangency_weights = pmh.calc_tangency_weights(factors_excess_returns[factors], name=name)

factor_models_tangency_weights = pd.concat([factor_models_tangency_weights, factor_model_tangency_weights], axis=1)

factor_models_tangency_weights

| CAPM Weights | AQR Weights | FF3 Weights | FF5 Weights | |

|---|---|---|---|---|

| MKT | 1.0000 | 0.2765 | 0.6142 | 0.2273 |

| HML | NaN | 0.1836 | 0.5019 | -0.0989 |

| RMW | NaN | 0.3546 | NaN | 0.3687 |

| UMD | NaN | 0.1853 | NaN | NaN |

| SMB | NaN | NaN | -0.1161 | 0.0806 |

| CMA | NaN | NaN | NaN | 0.4223 |

pd.concat([

pmh.calc_tangency_weights(factors_excess_returns[FACTOR_MODELS['FF5'] + ['UMD']], name='FF5 + Momentum'),

pmh.calc_tangency_weights(factors_excess_returns[FACTOR_MODELS['FF3'] + ['UMD']], name='FF3 + Momentum')

], axis=1)

| FF5 + Momentum Weights | FF3 + Momentum Weights | |

|---|---|---|

| MKT | 0.2186 | 0.3765 |

| HML | -0.0212 | 0.3653 |

| SMB | 0.0668 | -0.0512 |

| RMW | 0.3018 | NaN |

| CMA | 0.3214 | NaN |

| UMD | 0.1125 | 0.3094 |

This does not matter for pricing, but report the average (across \(n\) estimations) of the time-series regression r-squared statistics.

Do this for each of the three models you tested.

Do these models lead to high time-series r-squared stats? That is, would these factors be good in a Linear Factor Decomposition of the assets?

The best one is the FF5F, followed by AQR, FF3F and, finally, CAPM. The order of the R-Squared is not surprising at all: the factors with the most features have an “in-sample” better fit.

factor_model_time_series_tests = pd.DataFrame({})

for name, factors in FACTOR_MODELS.items():

factor_model_time_series_test = pmh.calc_iterative_regression(

portfolios_excess_returns,

factors_excess_returns[factors],

annual_factor=12,

warnings=False,

keep_columns=['R-Squared']

)

factor_model_time_series_tests = factor_model_time_series_tests.join(

factor_model_time_series_test.rename({'R-Squared': f'{name} R-Squared'}, axis=1),

how='outer'

)

factor_model_time_series_tests

| CAPM R-Squared | AQR R-Squared | FF3 R-Squared | FF5 R-Squared | |

|---|---|---|---|---|

| Aero | 0.5431 | 0.5994 | 0.5776 | 0.5971 |

| Agric | 0.3333 | 0.3421 | 0.3573 | 0.3619 |

| Autos | 0.4828 | 0.5278 | 0.5014 | 0.5030 |

| Banks | 0.6126 | 0.7740 | 0.7666 | 0.7819 |

| Beer | 0.3244 | 0.4148 | 0.3518 | 0.4336 |

| BldMt | 0.6949 | 0.7525 | 0.7492 | 0.7800 |

| Books | 0.6551 | 0.6889 | 0.6911 | 0.7022 |

| Boxes | 0.5549 | 0.5829 | 0.5683 | 0.5787 |

| BusSv | 0.8439 | 0.8463 | 0.8687 | 0.8736 |

| Chems | 0.6845 | 0.7452 | 0.7284 | 0.7461 |

| Chips | 0.6714 | 0.7498 | 0.7323 | 0.7461 |

| Clths | 0.5607 | 0.6190 | 0.5739 | 0.6291 |

| Cnstr | 0.6107 | 0.6315 | 0.6552 | 0.6728 |

| Coal | 0.1926 | 0.2126 | 0.2315 | 0.2342 |

| Drugs | 0.4666 | 0.4894 | 0.4995 | 0.5190 |

| ElcEq | 0.7351 | 0.7372 | 0.7394 | 0.7420 |

| FabPr | 0.4010 | 0.4245 | 0.5041 | 0.5174 |

| Fin | 0.7713 | 0.8129 | 0.7947 | 0.8209 |

| Food | 0.3541 | 0.4551 | 0.4041 | 0.4781 |

| Fun | 0.5861 | 0.6072 | 0.5952 | 0.5995 |

| Gold | 0.0488 | 0.0495 | 0.0556 | 0.0691 |

| Guns | 0.2483 | 0.3245 | 0.2727 | 0.3351 |

| Hardw | 0.5946 | 0.6669 | 0.6354 | 0.6541 |

| Hlth | 0.4058 | 0.4409 | 0.4351 | 0.4905 |

| Hshld | 0.4862 | 0.5547 | 0.5043 | 0.5819 |

| Insur | 0.5518 | 0.6612 | 0.6573 | 0.6653 |

| LabEq | 0.6806 | 0.7279 | 0.7477 | 0.7534 |

| Mach | 0.7400 | 0.7540 | 0.7728 | 0.7731 |

| Meals | 0.5816 | 0.6371 | 0.5919 | 0.6470 |

| MedEq | 0.5855 | 0.5958 | 0.5955 | 0.6045 |

| Mines | 0.4269 | 0.4589 | 0.4667 | 0.4726 |

| Oil | 0.3584 | 0.4556 | 0.4508 | 0.4619 |

| Other | 0.5770 | 0.5837 | 0.5810 | 0.5844 |

| Paper | 0.5991 | 0.6730 | 0.6381 | 0.6858 |

| PerSv | 0.5593 | 0.5848 | 0.5863 | 0.6197 |

| RlEst | 0.5268 | 0.6054 | 0.6735 | 0.6908 |

| Rtail | 0.6643 | 0.6866 | 0.6666 | 0.6889 |

| Rubbr | 0.6343 | 0.6453 | 0.6837 | 0.7044 |

| Ships | 0.4482 | 0.5046 | 0.4999 | 0.5369 |

| Smoke | 0.1821 | 0.2654 | 0.2312 | 0.2944 |

| Soda | 0.2449 | 0.3025 | 0.2734 | 0.3064 |

| Softw | 0.6270 | 0.7450 | 0.7454 | 0.7547 |

| Steel | 0.5857 | 0.6283 | 0.6405 | 0.6450 |

| Telcm | 0.5661 | 0.5804 | 0.5829 | 0.5917 |

| Toys | 0.4963 | 0.5102 | 0.5305 | 0.5509 |

| Trans | 0.6672 | 0.7088 | 0.6955 | 0.7210 |

| Txtls | 0.4311 | 0.5470 | 0.5863 | 0.6183 |

| Util | 0.2723 | 0.3614 | 0.3609 | 0.3805 |

| Whlsl | 0.7393 | 0.7523 | 0.7741 | 0.7974 |

(

factor_model_time_series_tests

.rename(columns=lambda c: c.replace(" R-Squared", ""))

.mean().to_frame('Avg R-Squared')

.sort_values('Avg R-Squared', ascending=False)

)

| Avg R-Squared | |

|---|---|

| FF5 | 0.5918 |

| AQR | 0.5719 |

| FF3 | 0.5679 |

| CAPM | 0.5226 |

We tested three models using the time-series tests (focusing on the time-series alphas.) Re-test these models, but this time use the cross-sectional test.

Report the time-series premia of the factors (just their sample averages,) and compare to the cross-sectionally estimated premia of the factors. Do they differ substantially?

Report the MAE of the cross-sectional regression residuals for each of the four models. How do they compare to the MAE of the time-series alphas?

For instance:

MKT estimated premium in the CAPM is 2.5% lower than in reality.

HML has a negative premium in the cross-section of AQR model and a positive small premium in historical values.

In the FF5, SMB and HML and CMA have premiums diverging in sign between historical and cross-section methodoly.

The smallest TS MAE is found in the time-series. The smallest CS MAE is found in the FF3 and FF5 models.

(

cross_sectional_tests

.loc[:, lambda df: [

c for c in df.columns if c.endswith('Annualized Lambda')

or c.endswith('Annualized Historical Premium')

]]

.transpose()

.sort_index()

.reset_index()

.rename({'index': 'Premium'}, axis=1)

.assign(Factor=lambda df: df['Premium'].map(lambda x: x[:3]))

.assign(Premium=lambda df: df['Premium'].map(lambda x: 'Historical' if x.endswith('Historical Premium') else 'Cross-Sectional'))

.rename(columns=lambda c: c.replace(' Cross-Section Regression', ''))

.set_index(['Factor', 'Premium']).unstack('Premium')

)

| CAPM | AQR | FF3 | FF5 | |||||

|---|---|---|---|---|---|---|---|---|

| Premium | Cross-Sectional | Historical | Cross-Sectional | Historical | Cross-Sectional | Historical | Cross-Sectional | Historical |

| Factor | ||||||||

| CMA | NaN | NaN | NaN | NaN | NaN | NaN | -0.0221 | 0.0283 |

| HML | NaN | NaN | -0.0323 | 0.0260 | -0.0210 | 0.0260 | -0.0259 | 0.0260 |

| MKT | 0.0079 | 0.0876 | 0.0172 | 0.0876 | 0.0388 | 0.0876 | 0.0403 | 0.0876 |

| RMW | NaN | NaN | 0.0175 | 0.0440 | NaN | NaN | 0.0187 | 0.0440 |

| SMB | NaN | NaN | NaN | NaN | -0.0396 | 0.0061 | -0.0414 | 0.0061 |

| UMD | NaN | NaN | 0.0003 | 0.0603 | NaN | NaN | NaN | NaN |

cross_sectional_tests

| Eta | Annualized Eta | R-Squared | MKT Lambda | Treynor Ratio | Annualized Treynor Ratio | MKT Annualized Lambda | MKT Historical Premium | MKT Annualized Historical Premium | TS MAE | ... | RMW Annualized Historical Premium | UMD Annualized Historical Premium | SMB Lambda | SMB Annualized Lambda | SMB Historical Premium | SMB Annualized Historical Premium | CMA Lambda | CMA Annualized Lambda | CMA Historical Premium | CMA Annualized Historical Premium | |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| CAPM Cross-Section Regression | 0.0069 | 0.0832 | 0.0093 | 0.0007 | 11.5196 | 138.2352 | 0.0079 | 0.0073 | 0.0876 | 0.0017 | ... | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN |

| AQR Cross-Section Regression | 0.0063 | 0.0755 | 0.2066 | 0.0014 | NaN | NaN | 0.0172 | 0.0073 | 0.0876 | 0.0021 | ... | 0.0440 | 0.0603 | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN |

| FF3 Cross-Section Regression | 0.0052 | 0.0627 | 0.3504 | 0.0032 | NaN | NaN | 0.0388 | 0.0073 | 0.0876 | 0.0020 | ... | NaN | NaN | -0.0033 | -0.0396 | 0.0005 | 0.0061 | NaN | NaN | NaN | NaN |

| FF5 Cross-Section Regression | 0.0050 | 0.0599 | 0.3765 | 0.0034 | NaN | NaN | 0.0403 | 0.0073 | 0.0876 | 0.0026 | ... | 0.0440 | NaN | -0.0035 | -0.0414 | 0.0005 | 0.0061 | -0.0018 | -0.0221 | 0.0024 | 0.0283 |

4 rows × 33 columns

(

cross_sectional_tests

.loc[:, lambda df: [

c for c in df.columns if c.endswith('CS Annualized MAE')

or c.endswith('TS Annualized MAE')

]]

.rename(index=lambda c: c.replace(' Cross-Section Regression', ''))

)

| TS Annualized MAE | CS Annualized MAE | |

|---|---|---|

| CAPM | 0.0210 | 0.0152 |

| AQR | 0.0246 | 0.0136 |

| FF3 | 0.0244 | 0.0120 |

| FF5 | 0.0314 | 0.0120 |