Solution - Unconstrained Optimization#

Data#

All the analysis below applies to the data set,

data/spx_weekly_returns.xlsxThe file has weekly returns.

For annualization, use 52 periods per year.

Consider only the following 10 stocks…

TICKS = ['AAPL','NVDA','MSFT','GOOGL','AMZN','META','TSLA','AVGO','BRK/B','LLY']

As well as the ETF,

TICK_ETF = 'SPY'

Data Processing#

import pandas as pd

INFILE = '../data/spx_returns_weekly.xlsx'

SHEET_INFO = 's&p500 names'

SHEET_RETURNS = 's&p500 rets'

SHEET_BENCH = 'benchmark rets'

FREQ = 52

info = pd.read_excel(INFILE,sheet_name=SHEET_INFO)

info.set_index('ticker',inplace=True)

temp_mkt_cap = info.loc[TICKS].copy()

temp_mkt_cap['mkt cap'] /= 1e9

temp_mkt_cap.rename(columns={'mkt cap':'mkt cap (billions $)'},inplace=True)

temp_mkt_cap.style.format({'mkt cap (billions $)':'{:,.0f}'})

| name | mkt cap (billions $) | |

|---|---|---|

| ticker | ||

| AAPL | Apple Inc | 3,009 |

| NVDA | NVIDIA Corp | 3,480 |

| MSFT | Microsoft Corp | 3,514 |

| GOOGL | Alphabet Inc | 2,146 |

| AMZN | Amazon.com Inc | 2,304 |

| META | Meta Platforms Inc | 1,745 |

| TSLA | Tesla Inc | 994 |

| AVGO | Broadcom Inc | 1,149 |

| BRK/B | Berkshire Hathaway Inc | 1,064 |

| LLY | Eli Lilly & Co | 733 |

rets = pd.read_excel(INFILE,sheet_name=SHEET_RETURNS)

rets.set_index('date',inplace=True)

rets = rets[TICKS]

bench = pd.read_excel(INFILE,sheet_name=SHEET_BENCH)

bench.set_index('date',inplace=True)

rets[TICK_ETF] = bench[TICK_ETF]

1. Risk Statistics#

1.1.#

Display a table with the following metrics for each of the return series.

mean (annualized)

volatility (annualized)

Sharpe ratio (annualized)

skewness

kurtosis

maximum drawdown

Note#

We have total returns, and Sharpe ratio is technically defined for excess returns. Don’t worry about the difference. (Or subtract SHV if you prefer.)

1.2.#

As a standalone investment, which is most attractive? And least? Justify your answer.

1.3.#

For each investment, estimate a regression against SPY. Report the

alpha (annualized as a mean)

beta

info ratio

r-squared

Based on this table, which investment seems most attractive relative to holding SPY?

import numpy as np

pd.options.display.float_format = "{:,.4f}".format

import matplotlib.pyplot as plt

import seaborn as sns

import statsmodels.api as sm

from sklearn.linear_model import LinearRegression

%matplotlib inline

plt.rcParams['figure.figsize'] = (12,6)

plt.rcParams['font.size'] = 15

plt.rcParams['legend.fontsize'] = 13

from cmds.portfolio import performanceMetrics, maximumDrawdown, get_ols_metrics

from cmds.risk import *

Solution 1.1.#

mets = performanceMetrics(rets,annualization=FREQ)

mets['skewness'] = rets.skew()

mets['kurtosis'] = rets.kurtosis()

mets['max drawdown'] = maximumDrawdown(rets)['Max Drawdown']

mets.style.format('{:.1%}')

| Mean | Vol | Sharpe | Min | Max | skewness | kurtosis | max drawdown | |

|---|---|---|---|---|---|---|---|---|

| AAPL | 23.9% | 27.7% | 86.3% | -17.5% | 14.7% | -21.9% | 182.6% | -34.6% |

| NVDA | 64.6% | 46.3% | 139.3% | -20.1% | 30.2% | 34.5% | 138.9% | -65.9% |

| MSFT | 26.1% | 24.0% | 108.9% | -14.4% | 15.0% | 7.2% | 234.2% | -35.1% |

| GOOGL | 21.7% | 28.0% | 77.5% | -12.0% | 25.8% | 58.3% | 372.1% | -41.9% |

| AMZN | 29.3% | 30.6% | 95.9% | -14.5% | 18.5% | 6.3% | 178.2% | -54.8% |

| META | 26.2% | 35.1% | 74.6% | -23.7% | 24.5% | 5.2% | 402.4% | -76.0% |

| TSLA | 47.0% | 58.6% | 80.1% | -25.9% | 33.3% | 54.8% | 159.4% | -72.2% |

| AVGO | 39.5% | 37.5% | 105.3% | -18.3% | 25.2% | 66.2% | 350.4% | -40.0% |

| BRK/B | 13.5% | 19.1% | 70.8% | -13.4% | 9.8% | -20.1% | 251.3% | -26.5% |

| LLY | 28.2% | 28.3% | 99.5% | -12.2% | 17.5% | 21.6% | 168.3% | -25.3% |

| SPY | 13.1% | 17.1% | 76.8% | -14.5% | 12.1% | -57.9% | 599.6% | -31.8% |

Solution 1.2.#

As a standalone investment, NVDA has

the best Sharpe, which is the best vol-adjusted return.

large positive skewness which is attractive.

large kurtosis, which would be bad with negative skewness but is appealing with positive skewness.

a large max drawdown.

If worried about the max drawdown, LLY may be a good choice.

smallest max drawdown

still has 4th hgihest Sharpe.

Solution 1.3.#

get_ols_metrics(rets['SPY'],rets,FREQ).style.format('{:.1%}',na_rep='-')

| alpha | SPY | r-squared | Treynor Ratio | Info Ratio | |

|---|---|---|---|---|---|

| AAPL | 9.3% | 111.3% | 47.3% | 21.4% | 46.1% |

| NVDA | 41.8% | 173.5% | 41.0% | 37.2% | 117.4% |

| MSFT | 12.6% | 103.2% | 54.0% | 25.3% | 77.4% |

| GOOGL | 7.7% | 106.6% | 42.4% | 20.3% | 36.2% |

| AMZN | 15.3% | 106.6% | 35.5% | 27.5% | 62.4% |

| META | 11.1% | 114.8% | 31.2% | 22.8% | 38.2% |

| TSLA | 23.8% | 176.2% | 26.4% | 26.7% | 47.4% |

| AVGO | 21.7% | 135.7% | 38.2% | 29.1% | 73.5% |

| BRK/B | 2.8% | 81.7% | 53.6% | 16.5% | 21.4% |

| LLY | 19.9% | 62.7% | 14.3% | 44.9% | 76.1% |

| SPY | 0.0% | 100.0% | 100.0% | 13.1% | - |

Based on this table, NVDA is the most attractive. It not only has (by far) the highest alpha, but also the highest Info Ratio (which is the risk-adjusted alpha.)

Solution .#

get_ols_metrics(rets[['SPY','NVDA']],rets[['AAPL']],FREQ).style.format('{:.1%}',na_rep='-')

| alpha | SPY | NVDA | r-squared | Info Ratio | |

|---|---|---|---|---|---|

| AAPL | 7.1% | 102.2% | 5.3% | 47.7% | 35.3% |

For every $100 in AAPL, we would short 97.9 dollars of SPY and short 7.4 dollars of NVDA.

Solution 1.5.#

The r-squared indicates how highly correlated our replication is to the target.

2. Portfolio Allocation#

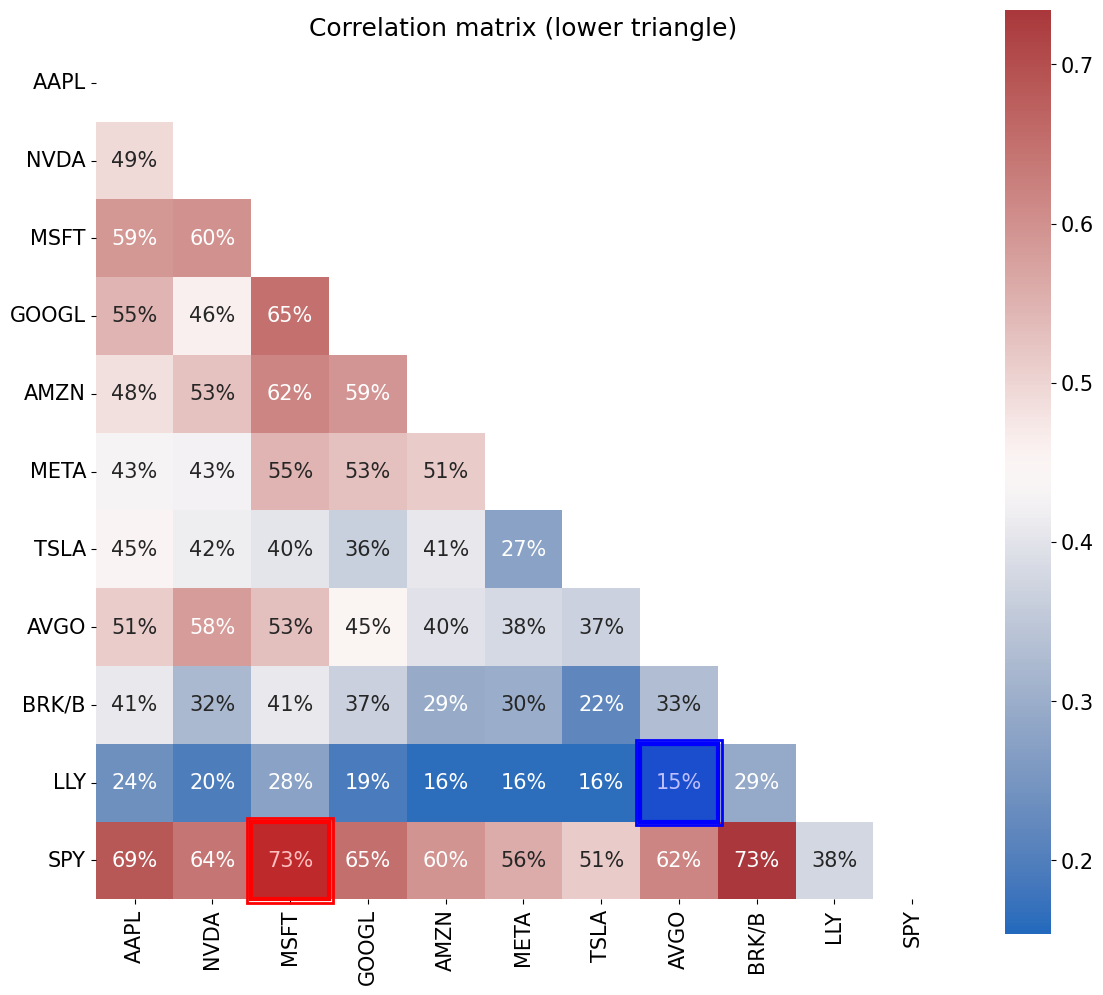

2.1.#

Display the correlation matrix of the returns.

Based on this information, which investment do you anticipate will get extra weight in the portfolio, beyond what it would merit for its mean return?

Report the maximally correlated assets and the minimally correlated assets.

2.2.#

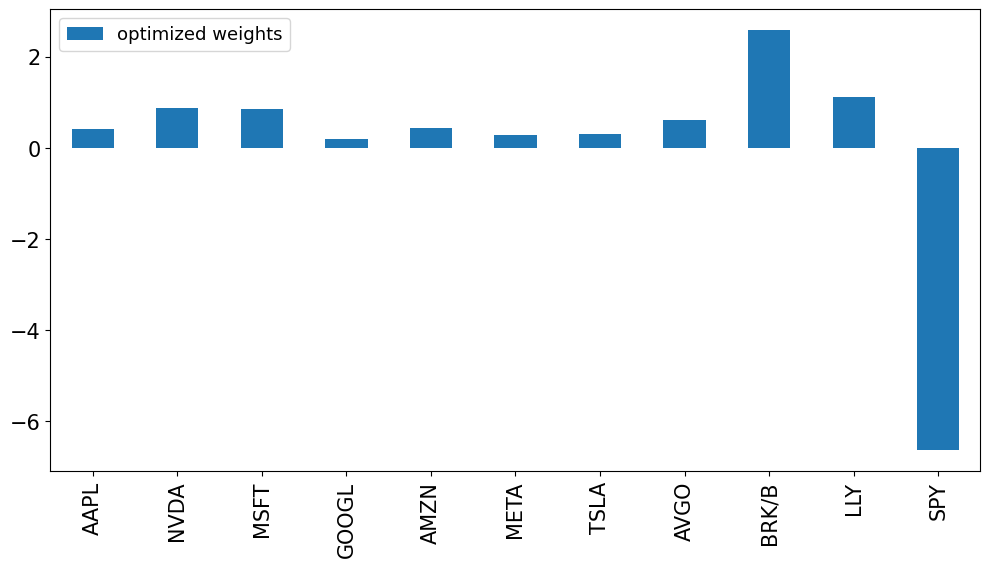

Calculate the weights of the mean-variance optimized portfolio, also called the tangency portfolio.

Display a table indexed by each investment, with the optimal weights in one column and the Sharpe ratios in another column.

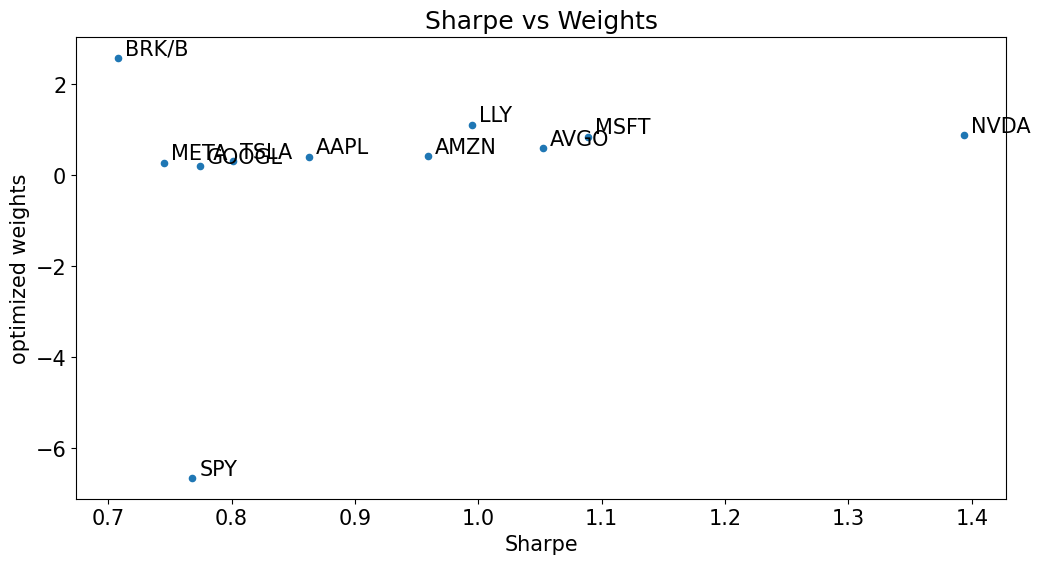

Do the investments with the best Sharpe ratios tend to get the biggest weights?

Note:#

To estimate the optimal weights, consider using the provided function below.

def optimized_weights(returns,dropna=True,scale_cov=1):

if dropna:

returns = returns.dropna()

covmat_full = returns.cov()

covmat_diag = np.diag(np.diag(covmat_full))

covmat = scale_cov * covmat_full + (1-scale_cov) * covmat_diag

weights = np.linalg.solve(covmat,returns.mean())

weights = weights / weights.sum()

if returns.mean() @ weights < 0:

weights = -weights

return pd.DataFrame(weights, index=returns.columns)

2.3.#

Report the following performance statistics of the portfolio achieved with the optimized weights calculated above.

mean

volatility

Sharpe

(Annualize all three statistics.)

2.4.#

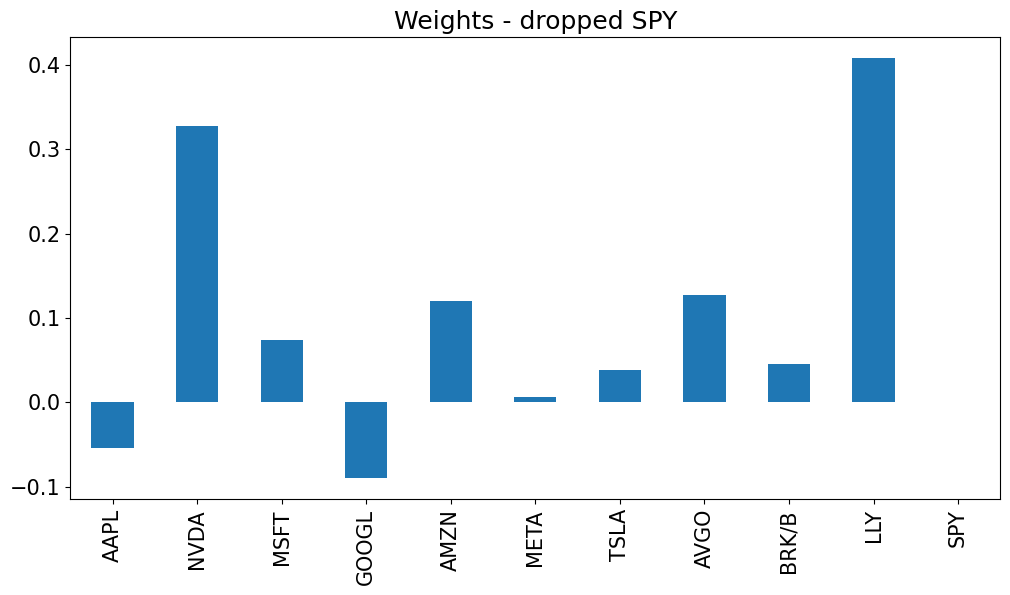

Try dropping the asset which had the biggest short position from the investment set. Re-run the optimization. What do you think of these new weights compared to the original optimized weights?

What is going on?

Solution 2.1#

from cmds.plot_tools import plot_corr_matrix

plot_corr_matrix(rets,triangle='lower',figsize=(12,12))

(<Figure size 1200x1200 with 2 Axes>,

<Axes: title={'center': 'Correlation matrix (lower triangle)'}>)

Solution 2.2#

wts = pd.DataFrame(index=rets.columns)

wts['optimized weights'] = optimized_weights(rets)

wts.plot.bar();

sharpe_vs_wts = pd.concat([wts['optimized weights'],mets['Sharpe']],axis=1)

sharpe_vs_wts.sort_values('optimized weights',ascending=False).style.format('{:.1%}')

| optimized weights | Sharpe | |

|---|---|---|

| BRK/B | 258.0% | 70.8% |

| LLY | 111.3% | 99.5% |

| NVDA | 88.3% | 139.3% |

| MSFT | 84.9% | 108.9% |

| AVGO | 60.2% | 105.3% |

| AMZN | 42.6% | 95.9% |

| AAPL | 40.9% | 86.3% |

| TSLA | 31.0% | 80.1% |

| META | 27.7% | 74.6% |

| GOOGL | 19.3% | 77.5% |

| SPY | -664.3% | 76.8% |

sharpe_vs_wts.plot.scatter(x='Sharpe',y='optimized weights')

for idx in sharpe_vs_wts.index:

x_value = sharpe_vs_wts.loc[idx, "Sharpe"]

y_value = sharpe_vs_wts.loc[idx, "optimized weights"]

plt.annotate(

text=idx,

xy=(x_value, y_value),

xytext=(5, 2),

textcoords="offset points"

)

plt.xlabel("Sharpe")

plt.ylabel("optimized weights")

plt.title("Sharpe vs Weights")

plt.show()

Solution 2.3#

port = pd.DataFrame(rets @ wts['optimized weights'],columns=['optimized weights'])

performanceMetrics(port,annualization=FREQ).style.format('{:.2%}')

| Mean | Vol | Sharpe | Min | Max | |

|---|---|---|---|---|---|

| optimized weights | 130.22% | 62.95% | 206.85% | -27.41% | 32.35% |

Solution 2.4#

The optimization is unrealistic in that it prescribes massive positions.

SPYis short nearly 600%.BRK-Bis long nearly 200%.

Solution 2.5#

The optimizer is shorting SPY because…

it has lower mean return than the tech stocks (

NVDA)it is highly correlated to the tech stocks and can offset much of their risk.

The optimizer is massively long BRK…

even though

BRKhas the worst Sharpe ratio of the investments.But

BRKis highly correlated toSPYwhile having relatively low correlation to tech. Thus it lowers total risk.

Extra: Sensitivity to dropping SPY#

DROPTICK = 'SPY'

wts[f'optimized ex {DROPTICK}'] = optimized_weights(rets.drop(columns=[DROPTICK]))

wts.loc[f'{DROPTICK}',f'optimized ex {DROPTICK}'] = 0

port[f'optimized ex {DROPTICK}'] = pd.DataFrame(rets @ wts[f'optimized ex {DROPTICK}'],columns=[f'optimized ex {DROPTICK}'])

wts[f'optimized ex {DROPTICK}'].plot.bar();

plt.title(f'Weights - dropped {DROPTICK}');

These weights are much more realistic. They are reasonable magnitudes and don’t include massive short positions.

Without SPY, the correlation matrix has relatively low correlations. Thus, the optimizer doesn’t think it can achieve such balanced (hedged) offsets, so it doesn’t prescribe extremes.

performanceMetrics(port,annualization=FREQ).style.format('{:.1%}')

| Mean | Vol | Sharpe | Min | Max | |

|---|---|---|---|---|---|

| optimized weights | 130.2% | 63.0% | 206.9% | -27.4% | 32.3% |

| optimized ex SPY | 42.4% | 26.2% | 161.6% | -11.9% | 15.2% |

wts.abs().sum().to_frame('gross mkt weight').style.format('{:,.1%}')

| gross mkt weight | |

|---|---|

| optimized weights | 1,428.6% |

| optimized ex SPY | 128.9% |