Solution - Constrained Optimization#

Data#

All the analysis below applies to the data set,

data/spx_weekly_returns.xlsxThe file has weekly returns.

For annualization, use 52 periods per year.

Consider only the following 10 stocks…

TICKS = ['AAPL','NVDA','MSFT','GOOGL','AMZN','META','TSLA','AVGO','BRK/B','LLY']

As well as the ETF,

TICK_ETF = 'SPY'

Data Processing#

import pandas as pd

INFILE = '../data/spx_returns_weekly.xlsx'

SHEET_INFO = 's&p500 names'

SHEET_RETURNS = 's&p500 rets'

SHEET_BENCH = 'benchmark rets'

FREQ = 52

info = pd.read_excel(INFILE,sheet_name=SHEET_INFO)

info.set_index('ticker',inplace=True)

info.loc[TICKS]

| name | mkt cap | |

|---|---|---|

| ticker | ||

| AAPL | Apple Inc | 3.008822e+12 |

| NVDA | NVIDIA Corp | 3.480172e+12 |

| MSFT | Microsoft Corp | 3.513735e+12 |

| GOOGL | Alphabet Inc | 2.145918e+12 |

| AMZN | Amazon.com Inc | 2.303536e+12 |

| META | Meta Platforms Inc | 1.745094e+12 |

| TSLA | Tesla Inc | 9.939227e+11 |

| AVGO | Broadcom Inc | 1.148592e+12 |

| BRK/B | Berkshire Hathaway Inc | 1.064240e+12 |

| LLY | Eli Lilly & Co | 7.332726e+11 |

rets = pd.read_excel(INFILE,sheet_name=SHEET_RETURNS)

rets.set_index('date',inplace=True)

rets = rets[TICKS]

bench = pd.read_excel(INFILE,sheet_name=SHEET_BENCH)

bench.set_index('date',inplace=True)

rets[TICK_ETF] = bench[TICK_ETF]

1 Constrained Optimization for Mean-Variance#

Continue working with the data above. Suppose we want to constrain the weights such that

there are no short positions beyond negative

20%, \(w_i\ge -.20\) for all \(i\)none of the positions may have weight over

35%, \(w_i \le .35\) for all \(i\).all the asset weights must sum to 1

Furthermore,

The targeted mean return is

20%per year.Be careful; the target is an annualized mean.

Consider using the code below as a starting point.

1.1.#

Report the weights of the constrained portfolio.

Report the mean, volatility, and Sharpe ratio of the resulting portfolio.

1.2.#

Compare these weights to the assets’ Sharpe ratios and means.

Do the most extreme positions also have the most extreme Sharpe ratios and means?

Why?

1.3.#

Compare the bounded portfolio weights to the unbounded portfolio weights (obtained from optimizing without the inequality constraints, keeping the equality constraints.)

Report the mean, volatility, and Sharpe ratio of both.

Code Help#

The minimize function will be how we optimize.

from scipy.optimize import minimize

Build the objective functions.

Before doing this, you will need to define

TARGET_MEANFREQcovmean

# def objective(w):

# return (w.T @ cov @ w)

# def fun_constraint_capital(w):

# return np.sum(w) - 1

# def fun_constraint_mean(w):

# return (mean @ w) - TARGET_MEAN

Build the constraints

sum of weights add to one

weighted average of means is the target mean

# constraint_capital = {'type': 'eq', 'fun': fun_constraint_capital}

# constraint_mean = {'type': 'eq', 'fun': fun_constraint_mean}

# constraints = ([constraint_capital, constraint_mean])

Build the upper and lower bounds on each asset.

You will need to use the minimize function along with these contraints, bounds, and an initial guess.

Solutions#

import pandas as pd

import numpy as np

import datetime

import warnings

import matplotlib.pyplot as plt

%matplotlib inline

plt.rcParams['figure.figsize'] = (10,5)

plt.rcParams['font.size'] = 13

plt.rcParams['legend.fontsize'] = 13

from matplotlib.ticker import (MultipleLocator,

FormatStrFormatter,

AutoMinorLocator)

from cmds.portfolio import *

from cmds.risk import *

#from cmds.plot_tools import plot_triangular_matrix

from cmds.mvportfolio import MVweights

def optimized_weights(returns,dropna=True,scale_cov=1):

if dropna:

returns = returns.dropna()

covmat_full = returns.cov()

covmat_diag = np.diag(np.diag(covmat_full))

covmat = scale_cov * covmat_full + (1-scale_cov) * covmat_diag

weights = np.linalg.solve(covmat,returns.mean())

weights = weights / weights.sum()

if returns.mean() @ weights < 0:

weights = -weights

return pd.DataFrame(weights, index=returns.columns)

1. Optimized Portfolios#

DO_EXCESS = True

USE_RF_ZERO = True

if USE_RF_ZERO:

rf = 0

else:

rf = bench['SHV']

retsx = rets.sub(rf)

if DO_EXCESS:

r = retsx

else:

r = rets

temp = performanceMetrics(r,annualization=FREQ).drop(columns=['Min','Max'])

temp.sort_values('Sharpe',ascending=False).style.format('{:.2%}',na_rep='')

| Mean | Vol | Sharpe | |

|---|---|---|---|

| NVDA | 64.56% | 46.33% | 139.35% |

| MSFT | 26.14% | 24.00% | 108.93% |

| AVGO | 39.49% | 37.51% | 105.26% |

| LLY | 28.15% | 28.30% | 99.49% |

| AMZN | 29.34% | 30.60% | 95.90% |

| AAPL | 23.87% | 27.66% | 86.29% |

| TSLA | 46.98% | 58.64% | 80.10% |

| GOOGL | 21.68% | 27.99% | 77.47% |

| SPY | 13.13% | 17.09% | 76.82% |

| META | 26.19% | 35.13% | 74.55% |

| BRK/B | 13.50% | 19.07% | 70.82% |

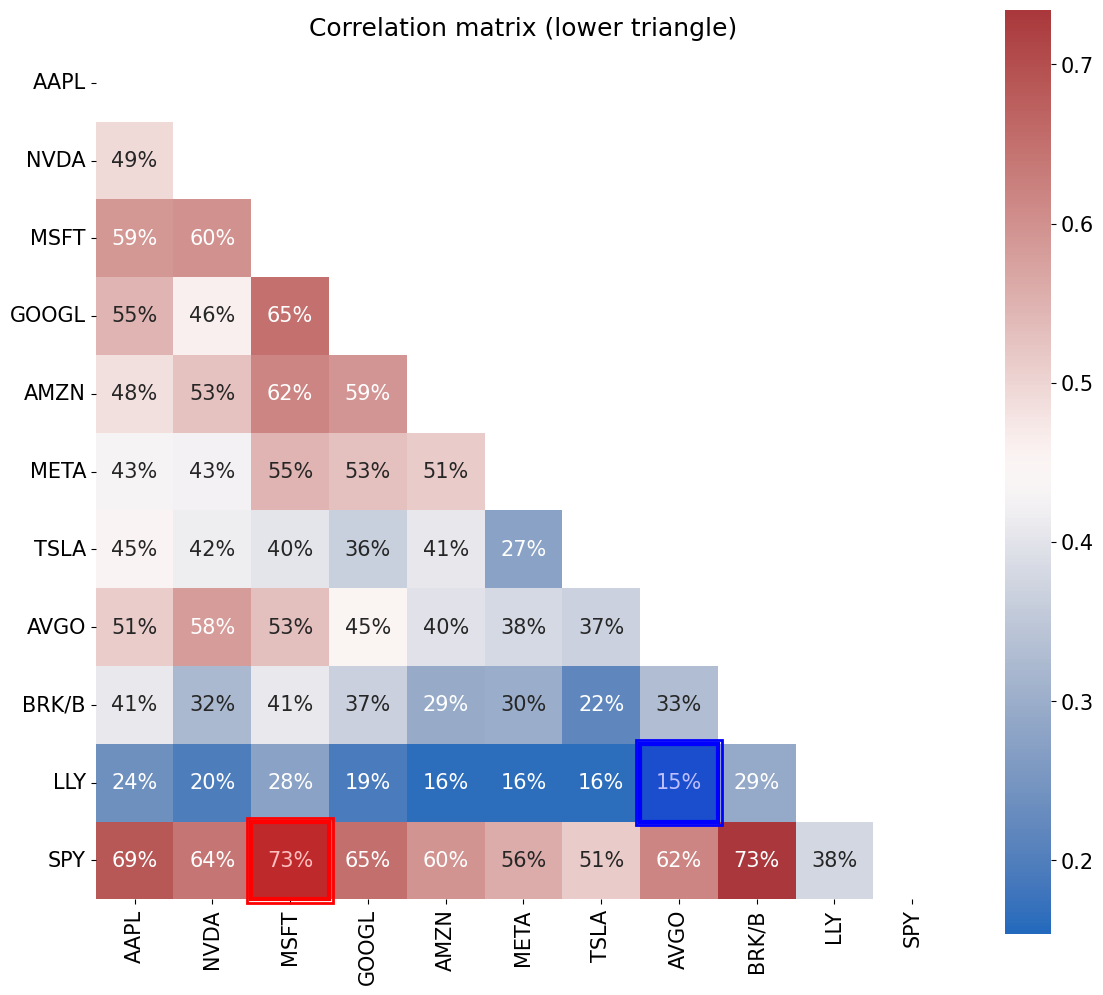

corr_matrix = r.corr()

from cmds.plot_tools import plot_corr_matrix

plot_corr_matrix(r,triangle='lower',figsize=(12,12))

plt.show()

mean = r.mean() * FREQ

cov = r.cov() * FREQ

Nassets = r.shape[1]

MINBOUND = -.10

MAXBOUND = .35

TARGET_MEAN = .20

def objective(w):

return (w.T @ cov @ w)

def fun_constraint_capital(w):

return np.sum(w) - 1

def fun_constraint_mean(w):

return (mean @ w) - TARGET_MEAN

constraint_capital = {'type': 'eq', 'fun': fun_constraint_capital}

constraint_mean = {'type': 'eq', 'fun': fun_constraint_mean}

if DO_EXCESS:

constraints = ([constraint_mean])

else:

constraints = ([constraint_capital, constraint_mean])

bounds_df = pd.DataFrame(index=rets.columns,columns=['Min','Max'],dtype=float)

bounds_df['Min'] = MINBOUND

bounds_df['Max'] = MAXBOUND

bounds = [tuple(bounds_df.iloc[i,:].values) for i in range(Nassets)]

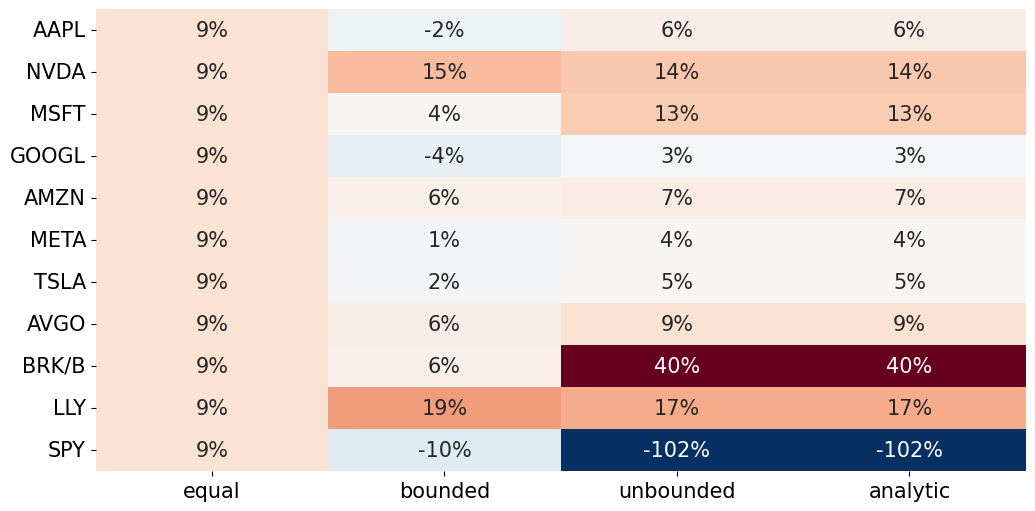

wstar = pd.DataFrame(index=temp.index,columns=['equal','bounded','unbounded'],dtype=float)

wstar['equal'] = np.ones(len(wstar.index))/Nassets

TOL = 1e-8

METHOD = 'SLSQP'

#METHOD = 'trust-constr'

w0 = np.ones(Nassets) / Nassets

solution_unbounded = minimize(objective, w0, method=METHOD, constraints=constraints, tol=TOL)

solution_bounded = minimize(objective, w0, method=METHOD, bounds=bounds, constraints=constraints, tol=TOL)

wstar['bounded'] = solution_bounded.x

wstar['unbounded'] = solution_unbounded.x

#wstar['analytic'] = optimized_weights(r,dropna=True,scale_cov=1)

wstar['analytic'] = MVweights(mean=mean,cov=cov,isexcess=DO_EXCESS,target=TARGET_MEAN)

if solution_bounded.success and solution_unbounded.success:

print('Optimization SUCCESSFUL.')

else:

print('Optimization FAILED.')

print(f'Iterations: {solution_bounded.nit}.')

Optimization SUCCESSFUL.

Iterations: 19.

1.1, 1.3. Portfolio Stats#

wstar.sort_values('bounded',ascending=False).style.format('{:.2%}')

| equal | bounded | unbounded | analytic | |

|---|---|---|---|---|

| LLY | 9.09% | 19.03% | 17.12% | 17.09% |

| NVDA | 9.09% | 15.30% | 13.55% | 13.56% |

| AVGO | 9.09% | 6.30% | 9.25% | 9.24% |

| AMZN | 9.09% | 5.80% | 6.52% | 6.55% |

| BRK/B | 9.09% | 5.75% | 39.63% | 39.63% |

| MSFT | 9.09% | 4.38% | 13.04% | 13.03% |

| TSLA | 9.09% | 2.07% | 4.76% | 4.76% |

| META | 9.09% | 0.66% | 4.27% | 4.26% |

| AAPL | 9.09% | -1.71% | 6.29% | 6.29% |

| GOOGL | 9.09% | -3.55% | 2.98% | 2.97% |

| SPY | 9.09% | -10.00% | -102.02% | -102.02% |

corr_weights = wstar.drop(columns=['equal']).corr().iloc[0,1]

display(f'Correlation between BOUNDED and UNBOUNDED is: {corr_weights:.1%}')

'Correlation between BOUNDED and UNBOUNDED is: 63.8%'

from cmds.plot_tools import plot_triangular_matrix

plot_triangular_matrix(wstar, full_matrix=True)

plt.show()

optimized = pd.DataFrame(index=['equal', 'bounded', 'unbounded'], columns=['mean','vol'],dtype=float)

optimized.loc['equal','mean'] = wstar['equal'] @ mean

optimized.loc['equal','vol'] = np.sqrt(wstar['equal'] @ cov @ wstar['equal'])

optimized.loc['bounded','mean'] = wstar['bounded'] @ mean

optimized.loc['bounded','vol'] = np.sqrt(wstar['bounded'] @ cov @ wstar['bounded'])

optimized.loc['unbounded','mean'] = wstar['unbounded'] @ mean

optimized.loc['unbounded','vol'] = np.sqrt(wstar['unbounded'] @ cov @ wstar['unbounded'])

optimized.loc['analytic','mean'] = wstar['analytic'] @ mean

optimized.loc['analytic','vol'] = np.sqrt(wstar['analytic'] @ cov @ wstar['analytic'])

optimized['sharpe'] = optimized['mean'] / optimized['vol']

optimized.style.format('{:.2%}')

| mean | vol | sharpe | |

|---|---|---|---|

| equal | 30.28% | 22.16% | 136.64% |

| bounded | 20.00% | 11.92% | 167.83% |

| unbounded | 20.00% | 9.67% | 206.85% |

| analytic | 20.00% | 9.67% | 206.85% |

1.2. Comparison with Stand-alone Metrics#

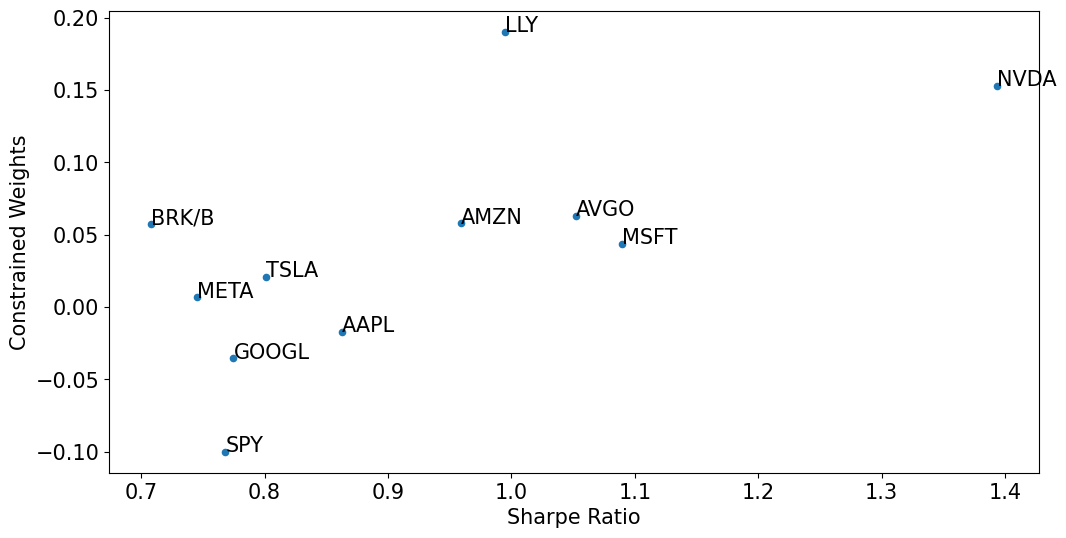

Consider how the most extreme positions compare to the most extreme Sharpe Ratios.

df = pd.concat([wstar[['bounded']],temp[['Sharpe']]],axis=1).sort_values('Sharpe',ascending=False)

ax = df.plot.scatter(x='Sharpe',y='bounded')

ax.set_xlabel('Sharpe Ratio')

ax.set_ylabel('Constrained Weights')

for idx, row in df.iterrows():

ax.annotate(idx, (row['Sharpe'], row['bounded']))

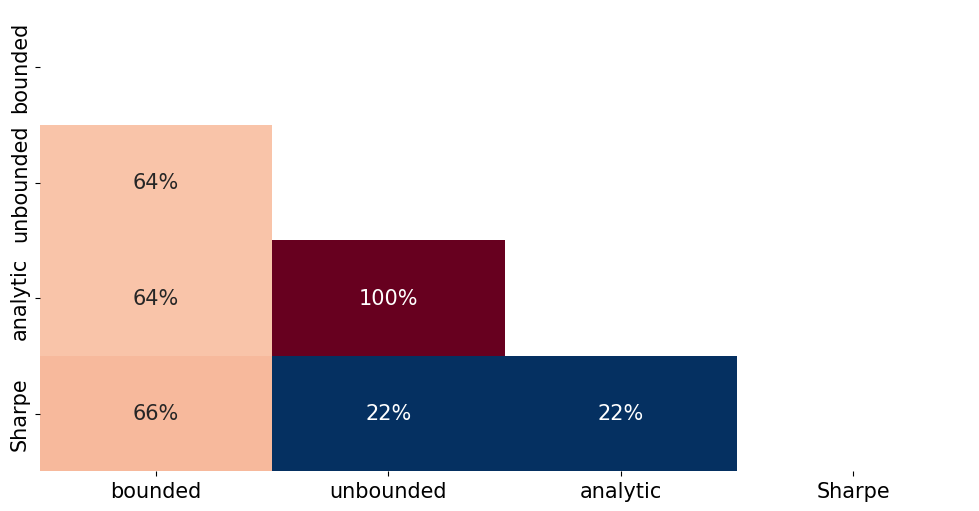

temp = pd.concat([wstar,temp[['Sharpe']]],axis=1).drop(columns=['equal']).corr()

plot_triangular_matrix(temp,full_matrix=False)

Costs of the Bounds#

Using the LaGrangian…

warnings.filterwarnings("ignore", message="delta_grad == 0.0. Check if the approximated function is linear.")

TOL = 1e-12

METHOD = 'trust-constr'

w0 = wstar['bounded']

solutionALT = minimize(objective, w0, method=METHOD, bounds=bounds,constraints=constraints, tol=TOL)

pd.DataFrame(solutionALT.v[-1], index=mean.index, columns=['Lagrange Multipliers']).sort_values('Lagrange Multipliers',ascending=False).style.format('{:.2%}'.format)

| Lagrange Multipliers | |

|---|---|

| MSFT | 0.00% |

| AMZN | 0.00% |

| GOOGL | 0.00% |

| AAPL | 0.00% |

| AVGO | 0.00% |

| META | 0.00% |

| TSLA | 0.00% |

| BRK/B | -0.00% |

| NVDA | -0.00% |

| LLY | -0.00% |

| SPY | -1.05% |