Constrained Optimization of the Harvard Endowment#

HBS Case#

The Harvard Management Company and Inflation-Indexed Bonds#

import pandas as pd

import numpy as np

import warnings

from scipy.optimize import minimize

Data Processing#

Organize Return Statistics as provided in the Harvard Case#

Assumed (Exhibit 4)

Historic (Exhibit 2)

The exhibits are a mess when loaded, function below cleans them up and returns the relevant data.

Problem with Data in Exhibit 2#

Note: The historic correlation matrix in Exhibit 2 is not positive definite!

This is clearly a mistake in the exhibit.

It does not cause an obvious problem with the results below.

But if you compare the analytic MV solution with a numerical optimization of the classic MV problem (no bounds) one sees that the numerical optimizer can take advantage of the matrix being negative definite to achieve a negative variance!

Thus, the numerically optimized solution with constraints is suspect.

Thus, the analysis with “Historic” data from Exhibit 2 should be taken with a grain of salt. Yet it still illustrates the concept.

def read_harvard_stats_exhibit(df,description=None):

# get the portion of the exhibit with actual data

df.dropna(subset=[df.columns[0]],axis=0,how='any',inplace=True)

df.set_index(df.columns[0],inplace=True)

df.dropna(axis=1,how='all',inplace=True)

df.dropna(axis=0,how='all',inplace=True)

df.set_index(df.columns[0],inplace=True)

df.index.name = description

# deal with typos and bad formatting from the case exhbit

if description == 'Assumed Stats':

df.rename({'Infl-Indexed Bonds':'Inflation-Indexed Bonds'},axis=0,inplace=True)

elif description == 'Historic Stats':

df.rename({'Absolute Returnb':'Absolute Return', 'High Yieldb':'High Yield', 'Foreign Bondsb':'Foreign Bonds'},axis=0, inplace=True)

# organize data

df.columns = ['Mean','Vol'] + list(df.index)

df = df.astype('float64')

corr = df.drop(columns=['Mean','Vol'])

### Force the correlation matrix in Exhibit 2 to be positive definite

HIST_CORR_FIX = [.80,.85]

if description == 'Historic Stats':

corr.loc['Absolute Return',['Domestic Equity','Foreign Equity']] = HIST_CORR_FIX

corr.loc[['Domestic Equity','Foreign Equity'],'Absolute Return'] = HIST_CORR_FIX

vol = df['Vol'] / 100

mean = df['Mean'] / 100

cov = corr * (np.outer(vol, vol.T))

return {'mean':mean, 'vol':vol, 'cov':cov, 'corr':corr}

Organize Optimization Parameters#

Also read in the HBS Solutions#

def read_harvard_optimization_exhibit(df, description = None):

df = df.dropna(axis=1,how='all').dropna(axis=0,how='all').set_index(df.columns[0])

df.columns = df.iloc[-4,:]/100

df = df.loc[cov.index]

if description == 'Historic Stats':

df.drop(index='Inflation-Indexed Bonds',inplace=True)

hbs_solutions = df.loc[:,df.columns.notnull()]/100

hbs_solutions.index.name = 'weights'

bounds_df = df.iloc[:,-2:]

if description == 'Policy':

bounds_df /= 100

bounds_df.columns = ['Min','Max']

bounds_df.index.name = description

return bounds_df, hbs_solutions

Case has 4 combinations#

Two types of statistics#

Historic

Assumed

Two sets of bounds#

Long-only

Policy

Our main focus, like that of case, is

Assumed stats

Policy constraints

DATAFILE = '../data/harvard_tips_exhibits.xlsx'

USE_HISTORIC_STATS = False

USE_LONGONLY_CONSTRAINT = False

if USE_HISTORIC_STATS:

sheet_stats = 'Exhibit 2'

stats_description = 'Historic Stats'

else:

sheet_stats = 'Exhibit 4'

stats_description = 'Assumed Stats'

if USE_LONGONLY_CONSTRAINT:

sheet_constraint = 'Exhibit 5'

constraint_description = 'Long-Only'

else:

sheet_constraint = 'Exhibit 6'

constraint_description = 'Policy'

with warnings.catch_warnings():

warnings.simplefilter('ignore')

rawdata_stats = pd.read_excel(DATAFILE,sheet_name=sheet_stats)

rawdata_opt = pd.read_excel(DATAFILE,sheet_name=sheet_constraint)

output_stats = read_harvard_stats_exhibit(rawdata_stats, description = stats_description)

mean = output_stats['mean']

cov = output_stats['cov']

nAssets = mean.shape[0]

bounds_df, hbs_solutions = read_harvard_optimization_exhibit(rawdata_opt, description = constraint_description)

Constrained Optimization#

Objective#

Minimize portfolio variance.

Portfolio weights: \(\boldsymbol{w}\)

Return covariance matrix: \(\boldsymbol{\Sigma}\)

def objective(w):

return (w.T @ cov @ w)

Constraints#

Equality Constraints#

Targeted mean for the optimized portfolio: \(\mu_p\) Define the following two functions:

These are imposed as equality constraints:

Target mean#

Below we analyze the problem for a target mean return of

8% if using the assume stats

12% if using the historic stats

The reason for the difference is that the historic stats are much more favorable, and it is easy to generate high mean returns.

if USE_HISTORIC_STATS:

TARGET_MEAN = 0.12

else:

TARGET_MEAN = 0.07

def fun_constraint_capital(w):

return np.sum(w) - 1

def fun_constraint_mean(w):

return (mean @ w) - TARGET_MEAN

constraint_capital = {'type': 'eq', 'fun': fun_constraint_capital}

constraint_mean = {'type': 'eq', 'fun': fun_constraint_mean}

cons = ([constraint_capital, constraint_mean])

Inequality Constraints#

This cell’s notation and setup is overkill for the simplicity of these constraints, but is noted here for more general problems.

Denote the \(k\times k\) identity matrix as \(\mathcal{I}_k\)

Denote the \(i\) column of the identity matrix as \(\boldsymbol{\iota}_i\)

Define the following \(k\) functions, for \(1\le i\le n\):

For each \(i\), we use the upper and lower inequality constraints:

Stack the constraints into matrix notation. The inequality constraint functions are linear:

and there are \(2n\) total of them–\(n\) upper and \(n\) lower:

Boundary Constraints#

Given that the inequality constraint functions are all linear, these constraints are simply boundary conditions.

The scipy package minimize implements boundary constraints specifically, via an iteration of tuples:

bounds = [tuple(bounds_df.iloc[i,:].values) for i in range(nAssets)]

Solution#

Default Tolerance#

Default tolerance is fine here, but be careful. Variance minimization for daily or even monthly variance leads to extremely small scaling of the objective function, and often the default tolerance will not be sufficient.

Even in the example below, making the tolerance stricter impacts the weights to the second decimal place.

Method#

For the data given here the problem is not too hard to solve, so many methods will work fine.

If using high dimensionality, nearly singular determinant, etc, it may matter more.

Below we use

SLSQPas it is fast and fairly robust for this application.At the end, we redo the optimization using

trust-constrsolely for the fact that this method automatically returns the Lagrange Multipliers which are useful for pedagogical reasons.

Initialize#

Try equally-weighted portfolio

This satisfies the Long-Only constraint.

May not satisfy the Policy constraint, but this problem is well-behaved, so it will be good enough as an initial guess

Verify!#

In a serious application, we would code the problem to verify that the answer returned by the solution is a “success” (obeys all the constraints) rather than a failed attempt. Try changing

TARGET_MEANto a big number, and you will see the optimizer fail to hit the target and obey the constraints.

TOL = 1e-12

METHOD = 'SLSQP'

w0 = np.ones(nAssets) / nAssets

solution = minimize(objective, w0, method=METHOD, bounds=bounds,constraints=cons, tol=TOL)

wstar = pd.DataFrame(data=solution.x, index=cov.columns, columns=['Bounded: Numerical'])

if solution.success:

print('Optimization SUCCESSFUL.')

else:

print('Optimization FAILED.')

print(f'Iterations: {solution.nit}.')

Optimization SUCCESSFUL.

Iterations: 31.

Other Solutions for Comparison#

HBS Case Exhibit Solution#

Compare to Exhibits 5 and 6.

Only applicable if

USE_HISTORIC_STATSisFalse.(Case does not provide their solutions when using Historic data.)

Classic MV via Numerical Optimization#

Solve numerically by dropping the inequality (bounds) constraints in minimize.

Only applicable if

USE_HISTORIC_STATSisFalse.(Exhibit 2 correlation matrix is not positive definite.)

Analytic MV solution for verification.#

Calculate this on your own.

The function doing it below is not available to you.

If

USE_HISTORIC_STATSisTrue, computation may not work correctly, but it is attempted.

Equal-weighted#

Just for illustration.

if sheet_stats == 'Exhibit 4' and TARGET_MEAN in hbs_solutions.columns:

wstar['Bounded: Case'] = hbs_solutions[TARGET_MEAN]

if not USE_HISTORIC_STATS:

METHOD = 'SLSQP'

TOL = 1e-12

w0 = np.ones(nAssets) / nAssets

solutionMV = minimize(objective, w0, method=METHOD, constraints=cons, tol=TOL)

wstar['MV: Numerical'] = solutionMV.x

if solutionMV.success:

print('Optimization SUCCESSFUL.')

else:

print('Optimization FAILED.')

print(f'Iterations: {solutionMV.nit}.')

Optimization SUCCESSFUL.

Iterations: 63.

def tangency_weights(returns,dropna=True,scale_cov=1):

if dropna:

returns = returns.dropna()

covmat_full = returns.cov()

covmat_diag = np.diag(np.diag(covmat_full))

covmat = scale_cov * covmat_full + (1-scale_cov) * covmat_diag

weights = np.linalg.solve(covmat,returns.mean())

weights = weights / weights.sum()

return pd.DataFrame(weights, index=returns.columns)

def MVweights(mean, cov, isexcess=True, target='TAN'):

vecOnes = np.ones([len(mean)])

wtsTan = np.linalg.solve(cov,mean)

wtsGMV = np.linalg.solve(cov,vecOnes)

wtsTan = wtsTan / wtsTan.sum()

wtsGMV = wtsGMV / wtsGMV.sum()

if type(target)==str:

if target=='TAN':

delta = 1

else:

delta = 0

else:

if isexcess:

delta = target * (vecOnes.T @ np.linalg.solve(cov,mean)) / (mean.T @ np.linalg.solve(cov,mean))

else:

delta = (target - mean @ wtsGMV) / (mean @ wtsTan - mean @ wtsGMV)

if isexcess:

wstar = wtsTan * delta

else:

wstar = wtsTan * delta + wtsGMV * (1-delta)

return wstar

wstar['MV: Analytic'] = MVweights(mean=mean.values,cov=cov.values,isexcess=False,target=TARGET_MEAN)

wstar.insert(0,'Equally-Weighted',w0)

Results#

Optimized Weights Comparison#

display(wstar.style.format('{:.2%}'.format))

| Equally-Weighted | Bounded: Numerical | Bounded: Case | MV: Numerical | MV: Analytic | |

|---|---|---|---|---|---|

| Domestic Equity | 8.33% | 22.00% | 22.00% | -0.05% | -0.05% |

| Foreign Equity | 8.33% | 5.00% | 5.00% | 5.74% | 5.74% |

| Emerging Markets | 8.33% | 19.00% | 19.00% | 19.87% | 19.87% |

| Private Equity | 8.33% | 22.83% | 22.80% | 22.01% | 22.01% |

| Absolute Return | 8.33% | -6.00% | -6.00% | -0.65% | -0.65% |

| High Yield | 8.33% | -6.92% | -6.90% | 4.15% | 4.15% |

| Commodities | 8.33% | 15.00% | 15.00% | 14.21% | 14.21% |

| Real Estate | 8.33% | 16.42% | 16.40% | 17.35% | 17.35% |

| Domestic Bonds | 8.33% | 1.00% | 1.00% | -19.98% | -19.98% |

| Foreign Bonds | 8.33% | 2.90% | 2.90% | 15.95% | 15.95% |

| Inflation-Indexed Bonds | 8.33% | 23.77% | 23.80% | 97.73% | 97.73% |

| Cash | 8.33% | -15.00% | -15.00% | -76.31% | -76.31% |

Using Bounds of…#

display(bounds_df.style.format('{:.2%}'.format))

| Min | Max | |

|---|---|---|

| Policy | ||

| Domestic Equity | 22.00% | 42.00% |

| Foreign Equity | 5.00% | 25.00% |

| Emerging Markets | -1.00% | 19.00% |

| Private Equity | 5.00% | 25.00% |

| Absolute Return | -6.00% | 14.00% |

| High Yield | -8.00% | 12.00% |

| Commodities | -5.00% | 15.00% |

| Real Estate | -3.00% | 17.00% |

| Domestic Bonds | 1.00% | 21.00% |

| Foreign Bonds | -5.00% | 15.00% |

| Inflation-Indexed Bonds | 0.00% | 100.00% |

| Cash | -15.00% | 5.00% |

Performance Stats#

meanP = (mean.T @ wstar)

volP = pd.Series(np.diag(wstar.T @ cov @ wstar),index=wstar.columns).apply(np.sqrt)

sharpeP = (meanP-mean.loc['Cash'])/volP

performance = pd.DataFrame({'mean':meanP,'vol':volP,'Sharpe':sharpeP})

display(performance.style.format('{:.2%}'.format))

| mean | vol | Sharpe | |

|---|---|---|---|

| Equally-Weighted | 5.67% | 6.58% | 33.05% |

| Bounded: Numerical | 7.00% | 9.84% | 35.57% |

| Bounded: Case | 7.00% | 9.84% | 35.57% |

| MV: Numerical | 7.00% | 9.08% | 38.54% |

| MV: Analytic | 7.00% | 9.08% | 38.54% |

In the case of Assumed Statistics (Exhibit 4)…#

The Bounded and Classic MV answers have similar Sharpe ratios.

Bounded optimization does a good job?

For these targeted mean returns, yes.

But for large target mean, classic MV can get there with huge long-short positions, and the bounded solution will fail or will do so with bigger penalty.

Try TARGET_MEAN of 10%, 15%, 20% to get an idea of this.

Additionally, this analysis is impacted by the strange assumed mean return. Domestic equities are assumed to only have a 3% premium over cash!

Which Constraints are most costly?#

The Lagrange Multipliers give us a clue.

Each is the derivative of the objective function with respect to the constraint boundary.

Magnitude shows impact.

Sign is an indication of whether constraint is upper or lower bound.

Showing impact on objective (variance) so numbers are small.

Focus on their relative magnitudes.

The importance of the constraints changes a lot#

between using the Long-Only or Policy Constraints

between using the Historic and Assumed Stats

warnings.filterwarnings("ignore", message="delta_grad == 0.0. Check if the approximated function is linear.")

TOL = 1e-12

METHOD = 'trust-constr'

w0 = wstar['Bounded: Numerical']

solutionALT = minimize(objective, w0, method=METHOD, bounds=bounds,constraints=cons, tol=TOL)

pd.DataFrame(solutionALT.v[-1], index=mean.index, columns=['Lagrange Multipliers']).sort_values('Lagrange Multipliers',ascending=False).style.format('{:.2%}'.format)

| Lagrange Multipliers | |

|---|---|

| Assumed Stats | |

| Commodities | 0.14% |

| Emerging Markets | 0.08% |

| Real Estate | 0.00% |

| Private Equity | 0.00% |

| Inflation-Indexed Bonds | -0.00% |

| Foreign Bonds | -0.00% |

| High Yield | -0.00% |

| Absolute Return | -0.13% |

| Domestic Bonds | -0.16% |

| Foreign Equity | -0.17% |

| Cash | -0.18% |

| Domestic Equity | -0.68% |

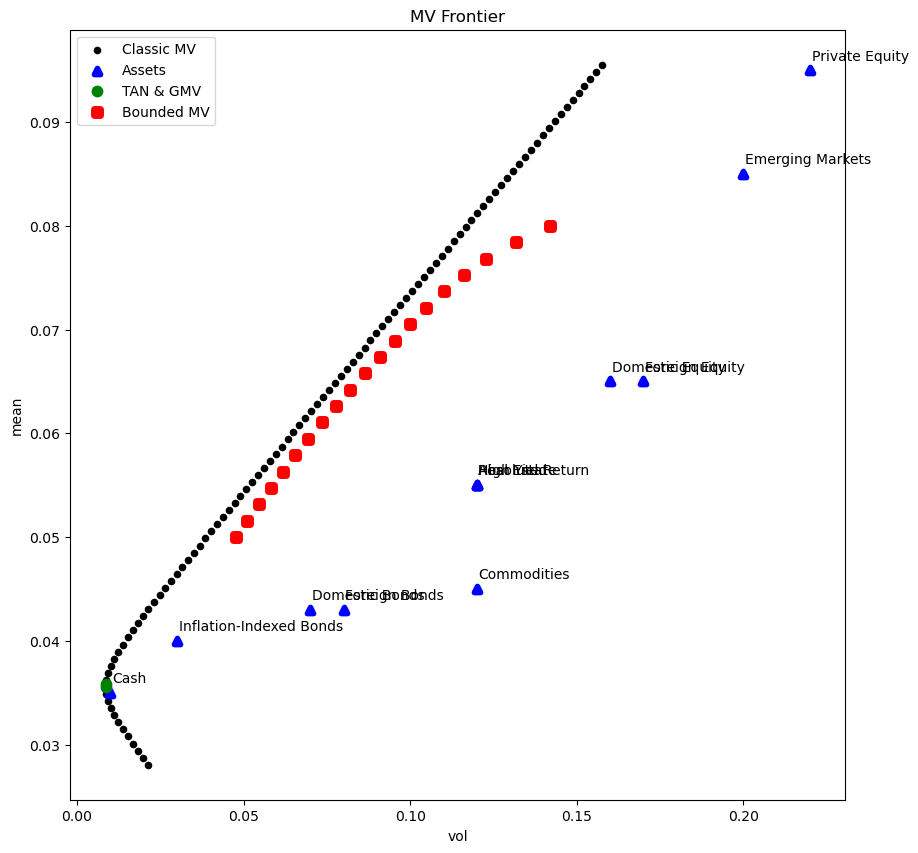

Figures#

import matplotlib.pyplot as plt

import seaborn as sns

warnings.filterwarnings('ignore')

omega = pd.DataFrame(MVweights(mean=mean.values,cov=cov.values,isexcess=False,target='TAN'), index=mean.index).rename({0:'Tangency'},axis=1)

mean_ex = mean-mean['Cash']

cov_ex = cov.drop(columns=['Cash'],index=['Cash'])

omega['GMV'] = MVweights(mean=mean.values,cov=cov.values,isexcess=False,target='GMV')

omega_tan = omega['Tangency']

omega_gmv = omega['GMV']

vols = pd.Series(np.sqrt(np.diag(cov)), index=cov.index)

special_vols = pd.Series(np.sqrt(np.diag(omega.T @ cov @ omega)), index=omega.columns)

special_means = mean.T @ omega

if USE_LONGONLY_CONSTRAINT:

MVgridmax = 350

else:

MVgridmax = 200

delta_grid = np.linspace(-25,MVgridmax,100)

mv_frame = pd.DataFrame(columns=['mean','vol'],index=delta_grid)

for i, delta in enumerate(delta_grid):

omega_mv = delta * omega_tan + (1-delta) * omega_gmv

mv_frame['mean'].iloc[i] = omega_mv.T @ mean.T

mv_frame['vol'].iloc[i] = np.sqrt(omega_mv.T @ cov @ omega_mv)

mv_assets = pd.concat([mean, vols],axis=1)

mv_special = pd.concat([special_means, special_vols],axis=1)

mv_assets.columns = ['mean','vol']

mv_special.columns = ['mean','vol']

ax = mv_frame.plot.scatter(x='vol',y='mean', c='k', figsize=(10,10), title='MV Frontier')

mv_assets.plot.scatter(x='vol',y='mean',ax=ax, c='b', marker='^', linewidth=4)

mv_special.plot.scatter(x='vol',y='mean',ax=ax, c='g', marker='o', linewidth=4)

for i in range(mv_assets.shape[0]):

plt.text(x=mv_assets['vol'][i]+.0005, y=mv_assets['mean'][i]+.001, s=mv_assets.index[i])

TOL = 1e-12

METHOD = 'SLSQP'

w0 = np.ones(nAssets) / nAssets

if USE_LONGONLY_CONSTRAINT:

maxmu = .12

minmu = 0

else:

maxmu = .08

minmu = .05

mu_grid = np.linspace(minmu,maxmu,20)

mvcon_frame = pd.DataFrame(columns=['mean','vol'],index=mu_grid)

for i, mu in enumerate(mu_grid):

TARGET_MEAN = mu

omega_con = minimize(objective, w0, method=METHOD, bounds=bounds,constraints=cons, tol=TOL).x

mvcon_frame['mean'].iloc[i] = omega_con.T @ mean.T

mvcon_frame['vol'].iloc[i] = np.sqrt(omega_con.T @ cov @ omega_con)

mvcon_frame.plot.scatter(x='vol',y='mean', c='r', marker = 's', ax=ax, linewidth=5)

plt.legend(['Classic MV', 'Assets', 'TAN & GMV', 'Bounded MV'])

full_fig = plt.gcf()