CAPM on Industry Portfolios#

import pandas as pd

import numpy as np

from pandas_datareader import data as pdr

import statsmodels.api as sm

import matplotlib.pyplot as plt

import warnings

warnings.filterwarnings('ignore', category=FutureWarning)

START_DATE = '1926-01'

END_DATE = '2025-09'

factors_raw = pdr.DataReader('F-F_Research_Data_Factors', 'famafrench', start=START_DATE, end=END_DATE)

ports_raw = pdr.DataReader('49_Industry_Portfolios', 'famafrench', start=START_DATE, end=END_DATE)

facs = factors_raw[0]/100

ports = ports_raw[0]/100

# Eliminate portfolios with suspicious returns (e.g., -1 or very close)

ports_clean = ports.mask(ports < -0.95, np.nan)

rx = ports_clean.sub(facs['RF'], axis=0)

betas = pd.Series(index=rx.columns, dtype=float)

alphas = pd.Series(index=rx.columns, dtype=float)

for col in rx.columns:

y = rx[col].dropna()

X = facs.loc[y.index, 'Mkt-RF']

X = sm.add_constant(X)

model = sm.OLS(y, X).fit()

betas[col] = model.params['Mkt-RF']

alphas[col] = model.params['const']

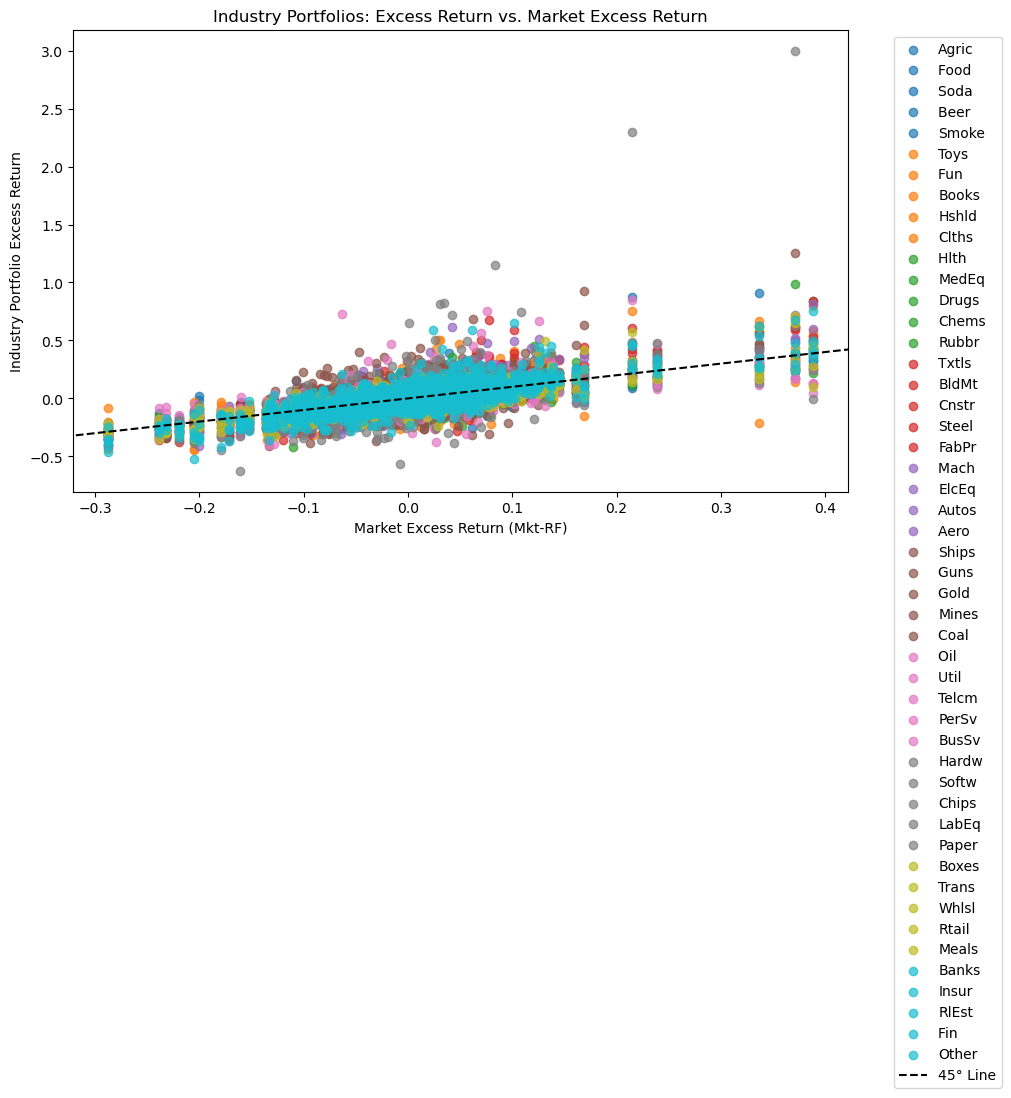

Timeseries#

Consider the variation of return data against the MKT factor.

Note that this is a time-series plot.

plt.figure(figsize=(10, 6))

colors = plt.cm.get_cmap('tab10', rx.shape[1])

for idx, col in enumerate(rx.columns):

plt.scatter(facs['Mkt-RF'], rx[col], label=col, color=colors(idx), alpha=0.7)

# Add a black dashed 45-degree line

xlim = plt.gca().get_xlim()

ylim = plt.gca().get_ylim()

lim_min = min(xlim[0], ylim[0])

lim_max = max(xlim[1], ylim[1])

plt.plot([lim_min, lim_max], [lim_min, lim_max], 'k--', label="45° Line")

plt.xlim(xlim)

plt.ylim(ylim)

plt.xlabel('Market Excess Return (Mkt-RF)')

plt.ylabel('Industry Portfolio Excess Return')

plt.title('Industry Portfolios: Excess Return vs. Market Excess Return')

plt.legend(bbox_to_anchor=(1.05, 1), loc='upper left')

plt.tight_layout()

plt.show()

/var/folders/zx/3v_qt0957xzg3nqtnkv007d00000gn/T/ipykernel_37091/2851721156.py:2: MatplotlibDeprecationWarning: The get_cmap function was deprecated in Matplotlib 3.7 and will be removed in 3.11. Use ``matplotlib.colormaps[name]`` or ``matplotlib.colormaps.get_cmap()`` or ``pyplot.get_cmap()`` instead.

colors = plt.cm.get_cmap('tab10', rx.shape[1])

/var/folders/zx/3v_qt0957xzg3nqtnkv007d00000gn/T/ipykernel_37091/2851721156.py:20: UserWarning: Tight layout not applied. The bottom and top margins cannot be made large enough to accommodate all Axes decorations.

plt.tight_layout()

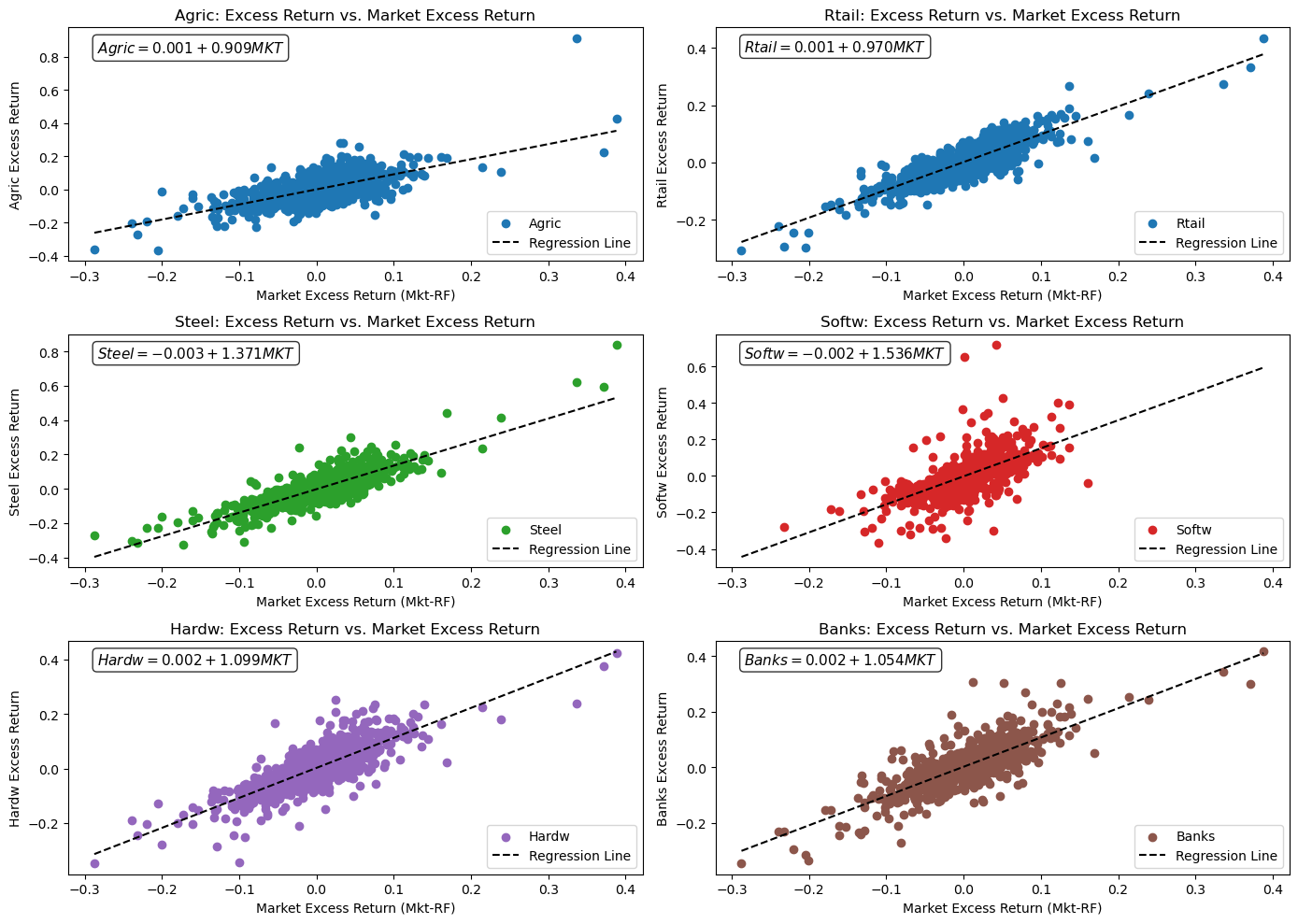

Time-series Regression#

Fit a time-series regression for each industry portfolio.

selected_cols = ["Agric", "Rtail", "Steel", "Softw", "Hardw", "Banks"]

colors_map = {

"Agric": "tab:blue",

"Util": "tab:orange",

"Steel": "tab:green",

"Softw": "tab:red",

"Hardw": "tab:purple",

"Banks": "tab:brown"

}

fig, axes = plt.subplots(3, 2, figsize=(14, 10))

axes = axes.flatten()

for i, col in enumerate(selected_cols):

ax = axes[i]

beta = betas[col]

alpha = alphas[col]

y = rx[col].dropna()

X = facs.loc[y.index, 'Mkt-RF']

ax.scatter(X, y, color=colors_map.get(col, None), label=col)

x_vals = np.linspace(facs['Mkt-RF'].min(), facs['Mkt-RF'].max(), 100)

y_fit = alpha + beta * x_vals

ax.plot(x_vals, y_fit, color='black', linestyle='--', label='Regression Line')

eqn_text = f"${col} = {alpha:.3f} + {beta:.3f} MKT$"

ax.annotate(eqn_text,

xy=(0.05, 0.95), xycoords='axes fraction',

fontsize=11,

ha='left', va='top',

bbox=dict(boxstyle='round', facecolor='white', alpha=0.8))

ax.set_xlabel('Market Excess Return (Mkt-RF)')

ax.set_ylabel(f'{col} Excess Return')

ax.set_title(f'{col}: Excess Return vs. Market Excess Return')

ax.legend()

plt.tight_layout()

plt.show()

rx_avg = rx.mean() * 12

y_cs = rx_avg.values

x_cs = betas.values.reshape(-1, 1)

# Without intercept: E[R] = lambda * beta

model_noi = sm.OLS(y_cs, x_cs).fit()

lambda_noi = model_noi.params.item()

# With intercept: E[R] = gamma + lambda * beta

X_with_const = sm.add_constant(x_cs)

model_i = sm.OLS(y_cs, X_with_const).fit()

alpha_i, lambda_i = model_i.params.tolist()

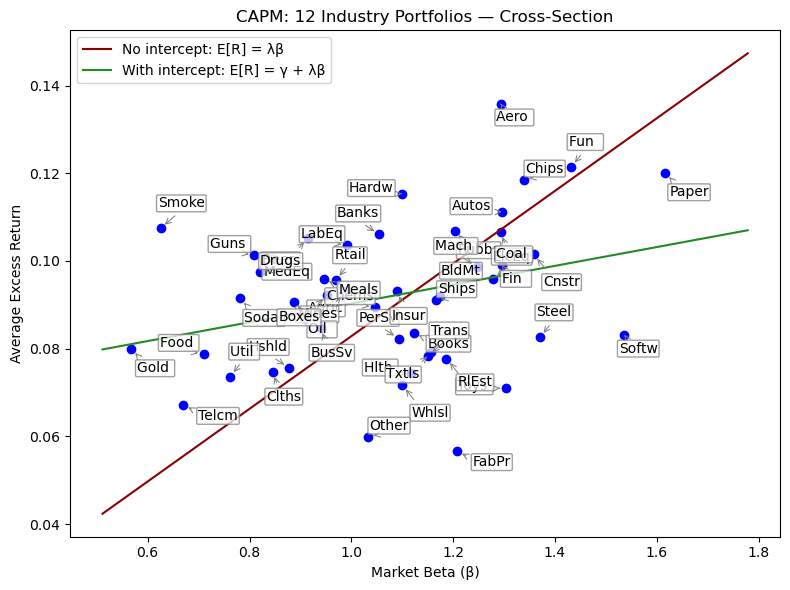

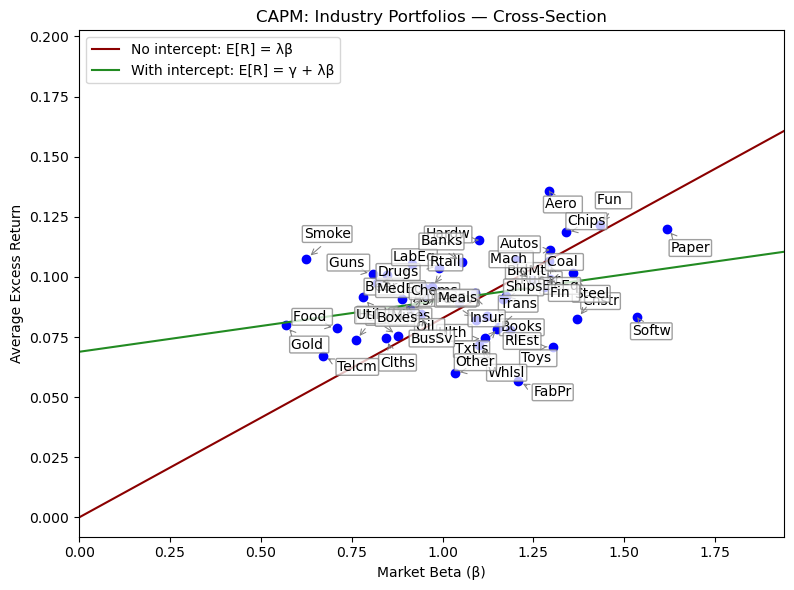

The Cross-Section#

The CAPM makes no claim about the goodness of fit of the time-series regressions. Rather, it implies that the cross-sectional regressions should fit perfectly.

Other considerations#

CAPM implies…

Time-series intercept (alpha) is zero

Cross-sectional fit (r-squared) is high

Cross-sectional slope (lambda) is the market factor premium

Cross-sectional intercept (gamma) is zero

FIG_MAX_SCALE = 1.2

# Scatter plot

fig = plt.figure(figsize=(8, 6))

plt.scatter(betas.values, rx_avg.values, color="blue")

# Improved annotation dispersion to reduce overlap/readability issues

offsets = [

(15, 8), (-18, 8), (17, -14), (-20, -16), (15, 18), (20, -20), (10, 18),

(25, -8), (-15, 15), (8, -18), (-22, 4), (10, -10)

]

for idx, (name, b) in enumerate(betas.items()):

offset = offsets[idx % len(offsets)] # Cycle offsets if >12 industries

plt.annotate(

name,

(b, rx_avg[name]),

textcoords='offset points',

xytext=offset,

ha='center', va='center',

bbox=dict(boxstyle="round,pad=0.1", edgecolor='grey', facecolor='white', alpha=0.75),

arrowprops=dict(arrowstyle="->", color='grey', lw=0.75, relpos=(0.5,0), shrinkA=4, shrinkB=4)

)

plt.xlabel('Market Beta (β)')

plt.ylabel('Average Excess Return')

plt.title('CAPM: Industry Portfolios — Cross-Section')

x_min = 0

x_max = betas.max() * FIG_MAX_SCALE

xgrid = np.linspace(x_min, x_max, 200)

y_noi = (lambda_noi * xgrid)

y_i = (alpha_i + lambda_i * xgrid)

plt.plot(xgrid, y_noi, color="darkred", label='No intercept: E[R] = λβ')

plt.plot(xgrid, y_i, color="forestgreen", label='With intercept: E[R] = γ + λβ')

plt.legend(loc='upper left')

plt.tight_layout()

# Set plot coordinates to match full view including lines

ylim = plt.ylim()

plt.xlim(left=0, right=x_max)

plt.ylim(bottom=min(0, ylim[0]), top=max(ylim[1]*FIG_MAX_SCALE, y_i.max()*FIG_MAX_SCALE, y_noi.max()*FIG_MAX_SCALE))

plt.show()

FIG_MIN_SCALE = 0.9

FIG_MAX_SCALE = 1.1

# Scatter plot

fig = plt.figure(figsize=(8, 6))

plt.scatter(betas.values, rx_avg.values, color="blue")

# Improved annotation dispersion to reduce overlap/readability issues

offsets = [

(15, 8), (-18, 8), (17, -14), (-20, -16), (15, 18), (20, -20), (10, 18),

(25, -8), (-15, 15), (8, -18), (-22, 4), (10, -10)

]

for idx, (name, b) in enumerate(betas.items()):

offset = offsets[idx % len(offsets)] # Cycle offsets if >12 industries

plt.annotate(

name,

(b, rx_avg[name]),

textcoords='offset points',

xytext=offset,

ha='center', va='center',

bbox=dict(boxstyle="round,pad=0.1", edgecolor='grey', facecolor='white', alpha=0.75),

arrowprops=dict(arrowstyle="->", color='grey', lw=0.75, relpos=(0.5,0), shrinkA=4, shrinkB=4)

)

plt.xlabel('Market Beta (β)')

plt.ylabel('Average Excess Return')

plt.title('CAPM: 12 Industry Portfolios — Cross-Section')

x_min = betas.min() * FIG_MIN_SCALE

x_max = betas.max() * FIG_MAX_SCALE

xgrid = np.linspace(x_min, x_max, 200)

y_noi = (lambda_noi * xgrid)

y_i = (alpha_i + lambda_i * xgrid)

plt.plot(xgrid, y_noi, color="darkred", label='No intercept: E[R] = λβ')

plt.plot(xgrid, y_i, color="forestgreen", label='With intercept: E[R] = γ + λβ')

plt.legend(loc='upper left')

plt.tight_layout()