Commodity Futures#

import pandas as pd

import numpy as np

import seaborn as sns

import matplotlib.pyplot as plt

%matplotlib inline

plt.rcParams['figure.figsize'] = (10,5)

plt.rcParams['font.size'] = 13

plt.rcParams['legend.fontsize'] = 13

from matplotlib.ticker import (MultipleLocator,

FormatStrFormatter,

AutoMinorLocator)

LOADFILE = '../data/futures_data.xlsx'

futures_info = pd.read_excel(LOADFILE,sheet_name='futures contracts').set_index('symbol')

Definition#

A futures contract is an agreement

entered at \(t\)

to purchase an asset at \(T\)

for a price \(F\)

It is an obligation, not an option!

We will return to some key differences between futures and forwards.

Assets#

Futures contracts are an important way to trade commodities including

energy

metals

grains

livestock

Futures contracts are traded widely on many assets beyond commodities:

interest-rate products

currency

equity indexes

other indexes

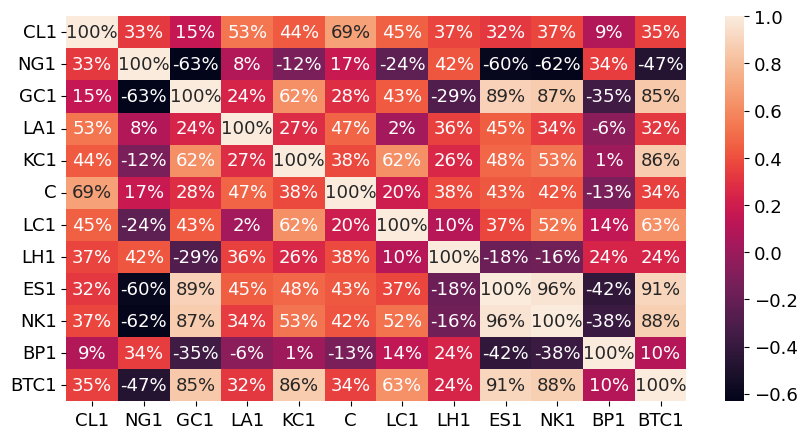

Data on Variety#

The correlation heatmap below gives a sense of the range of products.

Most bond correlations are 80%+

Most stock correlations are 60%+

ADJLAB = 'roll=ratio'

futures_hist = pd.read_excel(LOADFILE,sheet_name=f'continuous futures {ADJLAB}').set_index('date')

corrmat = futures_hist.loc['2015':,:].corr()

sns.heatmap(corrmat,annot=True,fmt='.0%')

plt.show()

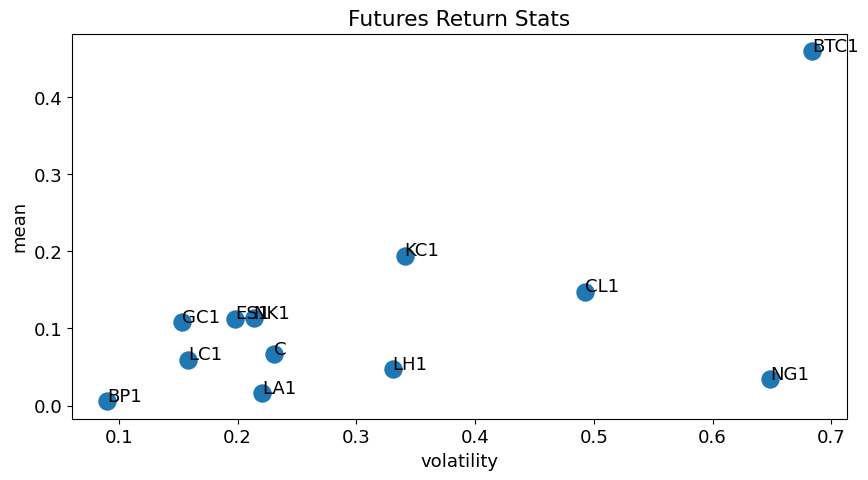

Variety of means and volatilities#

px = futures_hist.copy()

px[px<0] = np.nan

rx = px.pct_change().dropna()

DAYS = rx.resample('YE').size().median()

metrics = pd.DataFrame(columns=['mean','vol'],index=rx.columns,dtype=float)

metrics['mean'] = rx.mean() * DAYS

metrics['vol'] = rx.std() * np.sqrt(DAYS)

/var/folders/zx/3v_qt0957xzg3nqtnkv007d00000gn/T/ipykernel_89789/375234581.py:3: FutureWarning: The default fill_method='pad' in DataFrame.pct_change is deprecated and will be removed in a future version. Either fill in any non-leading NA values prior to calling pct_change or specify 'fill_method=None' to not fill NA values.

rx = px.pct_change().dropna()

df = metrics.copy().reset_index()

fig, ax = plt.subplots()

ax.scatter(x=df['vol'],y=df['mean'],s=150)

ax.set_xlabel('volatility')

ax.set_ylabel('mean')

for idx, row in df.iterrows():

ax.annotate(row['index'], (row['vol'], row['mean']))

plt.title('Futures Return Stats')

plt.show()

Trading#

Exchanges#

Futures trade on exchanges. In U.S. markets, the following two exchanges are of particular note:

Chicago Mercantile Exchange (CME)

Intercontinental Exchange (ICE)

In recent years, the trading has moved to being overwhelmingly (and at many exchanges, completely,) electronic.

Standardization#

One role of an exchange is to standardize the trading, which allows for better liquidity.

This is especially useful in commodities, to set the grade, size, location of the asset.

Clearing#

As part of trading on an exchange, futures are centrally cleared. This is important for

eliminating counterparty risk

achieving better netting and margin requirements

Settlement#

Settlement may be via

delivery of the asset

cash payment equal to the spot price of the asset

Note that there is cash delivery for

equity indexes

bitcoin (index) But there is also cash delivery for some physical assets

Hogs are delivered via cash

Cattle are delivered physically

futures_info[['name','category','delivery type']]

| name | category | delivery type | |

|---|---|---|---|

| symbol | |||

| CL | WTI CRUDE FUTURE Jul25 | Crude Oil | PHYS |

| NG | NATURAL GAS FUTR Jul25 | Natural Gas | PHYS |

| GC | GOLD 100 OZ FUTR Aug25 | Precious Metal | PHYS |

| AH | LME PRI ALUM FUTR Jun25 | Base Metal | PHYS |

| KC | COFFEE 'C' FUTURE Sep25 | Foodstuff | PHYS |

| ZC | CORN FUTURE Dec25 | Corn | PHYS |

| LE | LIVE CATTLE FUTR Aug25 | Livestock | PHYS |

| HE | LEAN HOGS FUTURE Aug25 | Livestock | CASH |

| ES | S&P500 EMINI FUT Jun25 | Equity Index | CASH |

| 225 | NIKKEI 225 (OSE) Sep25 | Equity Index | CASH |

| 6B | BP CURRENCY FUT Jun25 | Currency | PHYS |

| BTC | CME Bitcoin Fut Jun25 | Digital Assets | CASH |

futures_info.style.format({

'contract size': '{:,.0f}',

'last_price': '{:,.2f}',

'contract value': '{:,.0f}',

'contract date': '{:%Y-%m-%d}',

'margin limit': '{:,.0f}',

'tick size': '{:,.3f}',

'tick value': '{:,.2f}',

'open interest': '{:,.0f}',

'volume': '{:,.0f}',

'volume 10d avg': '{:,.0f}',

})

| bb ticker | name | type | category | delivery type | exchange | contract date | contract size | last_price | contract value | crncy | margin limit | tick size | tick value | open interest | volume | volume 10d avg | |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| symbol | |||||||||||||||||

| CL | CLA Comdty | WTI CRUDE FUTURE Jul25 | Physical commodity future. | Crude Oil | PHYS | New York Mercantile Exchange | 2025-07-01 | 1,000 | 67.16 | 67,160 | USD | 5,206 | 0.010 | 10.00 | 165,870 | 103,983 | 313,670 |

| NG | NGA Comdty | NATURAL GAS FUTR Jul25 | Physical commodity future. | Natural Gas | PHYS | New York Mercantile Exchange | 2025-07-01 | 10,000 | 3.60 | 35,980 | USD | 3,514 | 0.001 | 10.00 | 148,262 | 40,318 | 177,381 |

| GC | GCA Comdty | GOLD 100 OZ FUTR Aug25 | Physical commodity future. | Precious Metal | PHYS | Commodity Exchange, Inc. | 2025-08-01 | 100 | 3,410.00 | 341,000 | USD | 15,000 | 0.100 | 10.00 | 319,598 | 130,423 | 184,181 |

| AH | LAA Comdty | LME PRI ALUM FUTR Jun25 | Physical commodity future. | Base Metal | PHYS | London Metal Exchange | 2025-06-01 | 25 | 2,521.40 | 63,035 | USD | nan | 0.010 | 0.25 | 27,661 | 65,358 | 40,852 |

| KC | KCA Comdty | COFFEE 'C' FUTURE Sep25 | Physical commodity future. | Foodstuff | PHYS | ICE Futures US Softs | 2025-09-01 | 37,500 | 348.55 | 130,706 | USD | 10,410 | 0.050 | 18.75 | 64,351 | 5,956 | 14,658 |

| ZC | C A Comdty | CORN FUTURE Dec25 | Physical commodity future. | Corn | PHYS | Chicago Board of Trade | 2025-12-01 | 5,000 | 442.75 | 22,138 | USD | 975 | 0.250 | 12.50 | 516,966 | 13,842 | 111,093 |

| LE | LCA Comdty | LIVE CATTLE FUTR Aug25 | Physical commodity future. | Livestock | PHYS | Chicago Mercantile Exchange | 2025-08-01 | 40,000 | 218.03 | 87,210 | USD | 2,750 | 0.025 | 10.00 | 164,948 | 26,740 | 28,442 |

| HE | LHA Comdty | LEAN HOGS FUTURE Aug25 | Physical commodity future. | Livestock | CASH | Chicago Mercantile Exchange | 2025-08-01 | 40,000 | 110.20 | 44,080 | USD | 1,850 | 0.025 | 10.00 | 105,698 | 29,855 | 25,778 |

| ES | ESA Index | S&P500 EMINI FUT Jun25 | Physical index future. | Equity Index | CASH | Chicago Mercantile Exchange | 2025-06-01 | 50 | 6,014.50 | 300,725 | USD | 20,174 | 0.250 | 12.50 | 2,056,338 | 207,382 | 1,291,841 |

| 225 | NKA Index | NIKKEI 225 (OSE) Sep25 | Physical index future. | Equity Index | CASH | Osaka Exchange | 2025-09-01 | 1,000 | 38,050.00 | 38,050,000 | JPY | nan | 10.000 | 10,000.00 | 139,501 | 3,549 | 15,690 |

| 6B | BPA Curncy | BP CURRENCY FUT Jun25 | Currency future. | Currency | PHYS | Chicago Mercantile Exchange | 2025-06-01 | 62,500 | 136.13 | 85,081 | USD | 2,200 | 0.010 | 6.25 | 92,829 | 85,929 | 94,886 |

| BTC | BTCA Curncy | CME Bitcoin Fut Jun25 | Currency future. | Digital Assets | CASH | Chicago Mercantile Exchange | 2025-06-01 | 5 | 107,265.00 | 536,325 | USD | 130,992 | 5.000 | 25.00 | 21,494 | 2,783 | 8,306 |

Quoting Conventions#

https://www.cmegroup.com/markets/energy/crude-oil/light-sweet-crude.contractSpecs.html

Multiple#

futures_info[['name','contract size','contract value']].style.format({'contract size':'{:,.0f}','contract value':'${:,.0f}'})

| name | contract size | contract value | |

|---|---|---|---|

| symbol | |||

| CL | WTI CRUDE FUTURE Jul25 | 1,000 | $67,160 |

| NG | NATURAL GAS FUTR Jul25 | 10,000 | $35,980 |

| GC | GOLD 100 OZ FUTR Aug25 | 100 | $341,000 |

| AH | LME PRI ALUM FUTR Jun25 | 25 | $63,035 |

| KC | COFFEE 'C' FUTURE Sep25 | 37,500 | $130,706 |

| ZC | CORN FUTURE Dec25 | 5,000 | $22,138 |

| LE | LIVE CATTLE FUTR Aug25 | 40,000 | $87,210 |

| HE | LEAN HOGS FUTURE Aug25 | 40,000 | $44,080 |

| ES | S&P500 EMINI FUT Jun25 | 50 | $300,725 |

| 225 | NIKKEI 225 (OSE) Sep25 | 1,000 | $38,050,000 |

| 6B | BP CURRENCY FUT Jun25 | 62,500 | $85,081 |

| BTC | CME Bitcoin Fut Jun25 | 5 | $536,325 |

Tick Size#

futures_info[['name','tick size','tick value']].style.format({'tick size':'{:.3f}','tick value':'{:.2f}'})

| name | tick size | tick value | |

|---|---|---|---|

| symbol | |||

| CL | WTI CRUDE FUTURE Jul25 | 0.010 | 10.00 |

| NG | NATURAL GAS FUTR Jul25 | 0.001 | 10.00 |

| GC | GOLD 100 OZ FUTR Aug25 | 0.100 | 10.00 |

| AH | LME PRI ALUM FUTR Jun25 | 0.010 | 0.25 |

| KC | COFFEE 'C' FUTURE Sep25 | 0.050 | 18.75 |

| ZC | CORN FUTURE Dec25 | 0.250 | 12.50 |

| LE | LIVE CATTLE FUTR Aug25 | 0.025 | 10.00 |

| HE | LEAN HOGS FUTURE Aug25 | 0.025 | 10.00 |

| ES | S&P500 EMINI FUT Jun25 | 0.250 | 12.50 |

| 225 | NIKKEI 225 (OSE) Sep25 | 10.000 | 10000.00 |

| 6B | BP CURRENCY FUT Jun25 | 0.010 | 6.25 |

| BTC | CME Bitcoin Fut Jun25 | 5.000 | 25.00 |

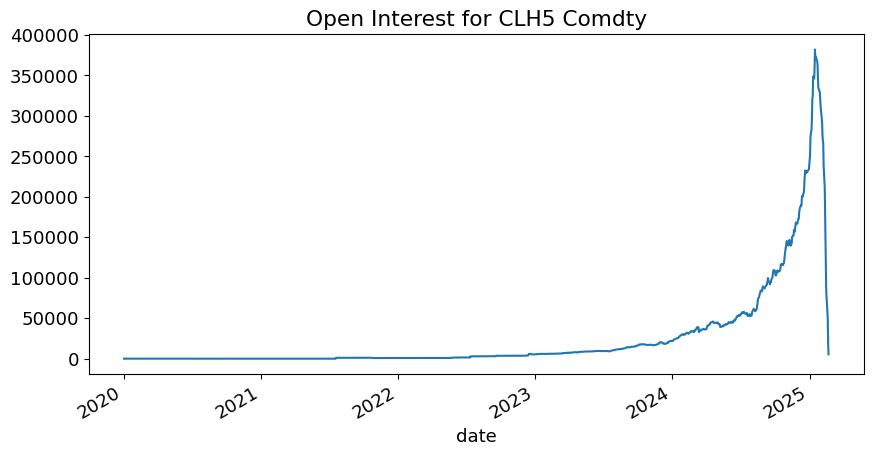

Open Interest#

Open Interest measures the number of open positions for the specific futures contract, cumulated over time.

Volume is the number of contracts traded that period (daily below).

See the chart below for the difference

futures_info[['name','open interest','volume','volume 10d avg']].style.format({'open interest':'{:,.0f}','volume':'{:,.0f}','volume 10d avg':'{:,.0f}'})

| name | open interest | volume | volume 10d avg | |

|---|---|---|---|---|

| symbol | ||||

| CL | WTI CRUDE FUTURE Jul25 | 165,870 | 103,983 | 313,670 |

| NG | NATURAL GAS FUTR Jul25 | 148,262 | 40,318 | 177,381 |

| GC | GOLD 100 OZ FUTR Aug25 | 319,598 | 130,423 | 184,181 |

| AH | LME PRI ALUM FUTR Jun25 | 27,661 | 65,358 | 40,852 |

| KC | COFFEE 'C' FUTURE Sep25 | 64,351 | 5,956 | 14,658 |

| ZC | CORN FUTURE Dec25 | 516,966 | 13,842 | 111,093 |

| LE | LIVE CATTLE FUTR Aug25 | 164,948 | 26,740 | 28,442 |

| HE | LEAN HOGS FUTURE Aug25 | 105,698 | 29,855 | 25,778 |

| ES | S&P500 EMINI FUT Jun25 | 2,056,338 | 207,382 | 1,291,841 |

| 225 | NIKKEI 225 (OSE) Sep25 | 139,501 | 3,549 | 15,690 |

| 6B | BP CURRENCY FUT Jun25 | 92,829 | 85,929 | 94,886 |

| BTC | CME Bitcoin Fut Jun25 | 21,494 | 2,783 | 8,306 |

Closing Positions#

Most open interest is ultimately closed via offsetting contracts, NOT delivery.

Consider the open interest for various contracts on Crude Oil (CL) and Gold (GC).

For each contract, we see the open interest rises about a month before the delivery, and then drops to nearly zero just before delivery.

TICKS = ['CL','GC']

futures_ts = pd.read_excel(LOADFILE,sheet_name='futures timeseries',header=[0,1,2]).droplevel(2,axis=1)

futures_ts.set_index(futures_ts.columns[0],inplace=True)

futures_ts.index.name = 'date'

futures_ts = futures_ts.swaplevel(axis=1)

idx = 0

exname = futures_ts['OPEN_INT'].iloc[:,idx].name

exdata = futures_ts['OPEN_INT'].iloc[:,idx].dropna()

exdata.plot(title=f'Open Interest for {exname}');

intpct = exdata[-1]/exdata.max()

print(f'Open Interest at close is {intpct:.2%} of its peak!')

Open Interest at close is 1.40% of its peak!

/var/folders/zx/3v_qt0957xzg3nqtnkv007d00000gn/T/ipykernel_89789/2823046234.py:1: FutureWarning: Series.__getitem__ treating keys as positions is deprecated. In a future version, integer keys will always be treated as labels (consistent with DataFrame behavior). To access a value by position, use `ser.iloc[pos]`

intpct = exdata[-1]/exdata.max()

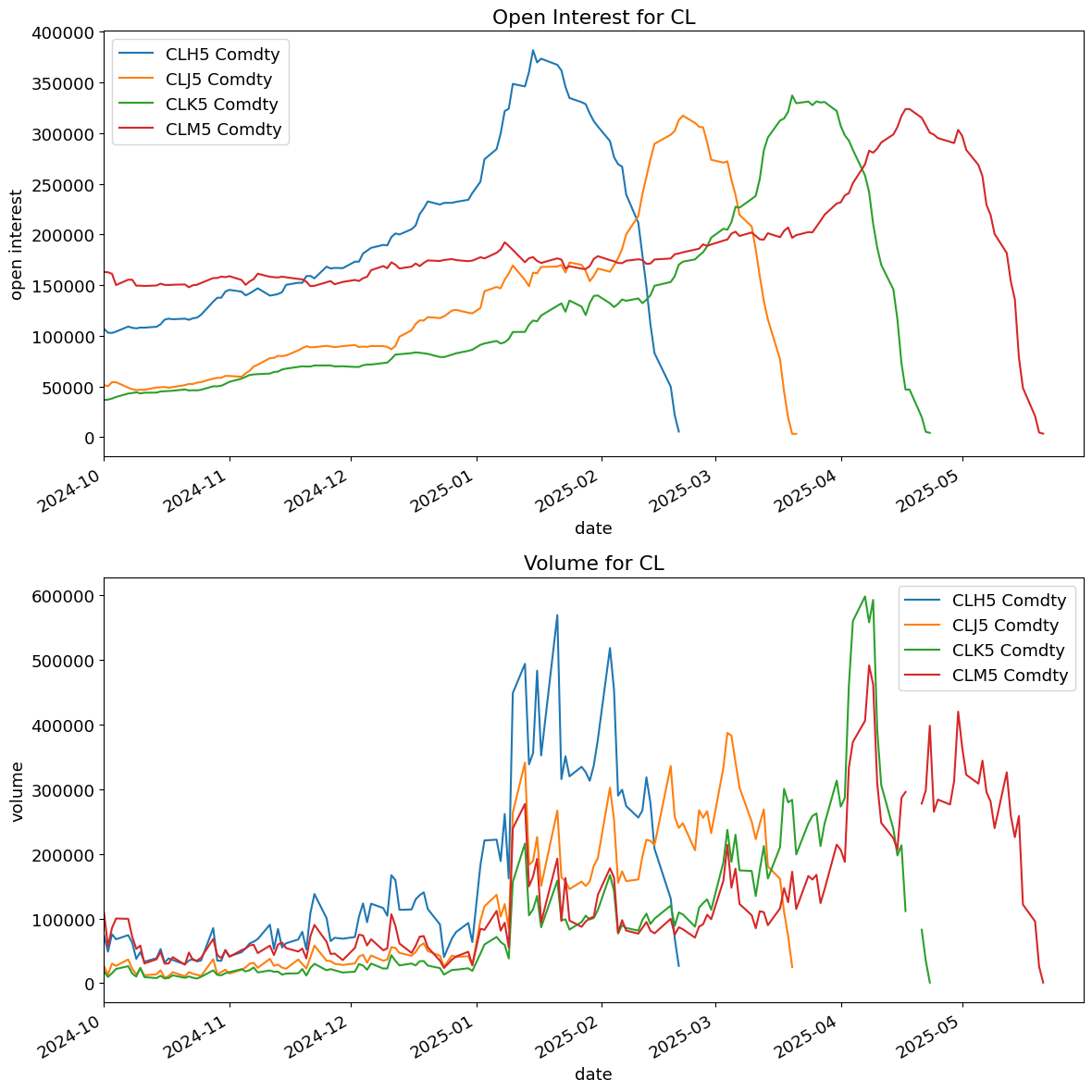

Active Contract#

For a given futures chain, only a few are liquid.

The active contract is typically denoted as the front-month (nearest expiration) which typically corresponds with the contract with the highest open interest.

For the two examples below, we see that the soonest-to-expiry sees a spike in open interest, with the second-nearest expiry rising in anticipation of being the active contract.

Liquidity#

Thus, the active contract tends to be much more liquid , as measured by volume or open interest.

As a corollary, a contract will be listed, yet may receive almost zero interest or volume for months or years.

In the example above, note that the open interest is miniscule for a year.

PLOTDATESTART = '2024-10'

PLOTDATEEND = '2025-05-31'

fig, ax = plt.subplots(2,1,figsize=(12,12))

futures_ts['OPEN_INT'].iloc[:,0:4].plot(ax=ax[0],xlim=(PLOTDATESTART,PLOTDATEEND),title=f'Open Interest for {TICKS[0]}',ylabel='open interest')

futures_ts['VOLUME'].iloc[:,0:4].plot(ax=ax[1],xlim=(PLOTDATESTART,PLOTDATEEND),title=f'Volume for {TICKS[0]}',ylabel='volume')

plt.tight_layout()

plt.show()

Margins and Marking to Market#

marg = futures_info[['name']].copy()

marg['margin limit %'] = futures_info['margin limit']/futures_info['contract value']

marg['vol'] = rx.std().values

marg['margin sigma'] = marg['margin limit %'] / marg['vol']

marg.set_index('name',inplace=True)

marg.index = [' '.join(row.split()[:-2]) for row in marg.index]

marg.dropna().sort_values('margin sigma').style.format({'margin limit %':'{:.1%}','vol':'{:.1%}','margin sigma':'{:.1f}'})

| margin limit % | vol | margin sigma | |

|---|---|---|---|

| LEAN HOGS | 4.2% | 2.0% | 2.0 |

| NATURAL GAS | 9.8% | 4.0% | 2.4 |

| WTI CRUDE | 7.8% | 3.1% | 2.5 |

| CORN | 4.4% | 1.4% | 3.1 |

| LIVE CATTLE | 3.2% | 1.0% | 3.2 |

| COFFEE 'C' | 8.0% | 2.1% | 3.8 |

| BP CURRENCY | 2.6% | 0.6% | 4.6 |

| GOLD 100 OZ | 4.4% | 1.0% | 4.6 |

| S&P500 EMINI | 6.7% | 1.2% | 5.5 |

| CME Bitcoin | 24.4% | 4.2% | 5.8 |

Futures References#

The CME provides a helpful series of videos for an introduction to Futures

Pricing#

Forward Price#

The basic model of a futures price is:

This equation is derived by no-arbitrage, in a simplified setting of

no market frictions

a constant risk-free rate, \(r_f\)

no financing considerations (margin, marking to market, etc)

This is just the forward pricing equation.

It says that the futures price should be the spot price compounded by the risk-free rate until delivery.

Carry#

The pricing formula above accounts for the time-value of money, but it does not account for the carry cost of the asset.

Dividend yield#

Suppose that the asset pays a dividend yield of \(q\)

dividends on stock index

lease rate on metals

Storage cost#

The asset may be costly to store, such that it has a negative carry.

oil, grains, etc

Carry#

Let carry, \(c\), denote the net difference of the storage costs minus income.

Then,

That is, the

higher the storage costs, the higher the futures price.

higher the income, the lower the futures price.

Convenience Yield#

For consumption assets, the no-arbitrage argument is more complicated.

This is due to the fact that the asset has a convenience yield, \(y\).

This convenience yield is not explicit income to the owner, but rather potential income should the consumption use of the asset be important during the contract period.

The equation can make explicit note of this,

or simply include the convenience yield as part of the carry.

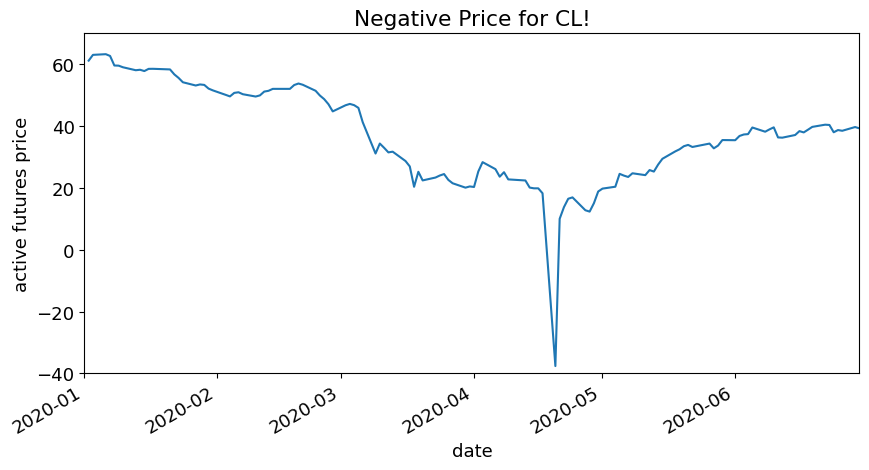

Negative Price for Oil?#

Typically, carry costs are a second-order factor for prices.

But sometimes market frictions cause them to be of high importance.

TICK = 'CL'

data_comp = pd.read_excel(LOADFILE,sheet_name=f'roll conventions {TICK}',header=[0,1,2]).droplevel(2,axis=1)

data_comp.set_index(data_comp.columns[0],inplace=True)

data_comp.index.name = 'date'

data_comp = data_comp.swaplevel(axis=1).droplevel(0,axis=1)

data_comp['CL1 Comdty'].plot(xlim=('2020-01-01','2020-06-30'),ylim=(-40,70),title=f'Negative Price for {TICK}!',ylabel='active futures price');

References#

https://www.nytimes.com/2020/04/20/business/oil-prices.html https://www.forbes.com/sites/sarahhansen/2020/04/21/heres-what-negative-oil-prices-really-mean/?sh=5530d0185a85

Complications#

There are various complications to the simple model.

Moving Interest Rates#

The formulas above assume a constant interest rate.

If the interest rate moves, then we would have the following adjustments:

Higher price if asset is positively correlated to the asset value

Lower price if asset is negatively correlated to the asset value Why?

Daily Settlement#

Futures contracts are settled daily, which means the cashflows are paid/received day-by-day rather than all at delivery.

Terminology#

Daily Settlement: The profit/loss of the day is settled via an accrual / deduction from the margin account. This payment is irrevocable. That is to say that it is not collateral but a permanent payment based on the day’s movement.

Variation Margin: To reduce counterparty risk in some collateralized trades, (such as repo,) you might need to pay a variation margin when the collateral value goes down. This is a form of collateral: it earns interest on your behalf, and it will be returned at the end of the trade.

Mark-to-market: Revising the price of an asset in the financial records, (such as a balance sheet,) to reflect the market movements in the price. This has no implications for cashflow but rather is a financial accounting revision. This term is often used to refer to teh daily settlement mentioned above, but this term is more general.

Futures vs Forwards#

The CME video compares and contrasts.

For each difference, would it cause the price of the future contract to be more or less than the comparable forward?

Which differences do you think are of most practical importance?

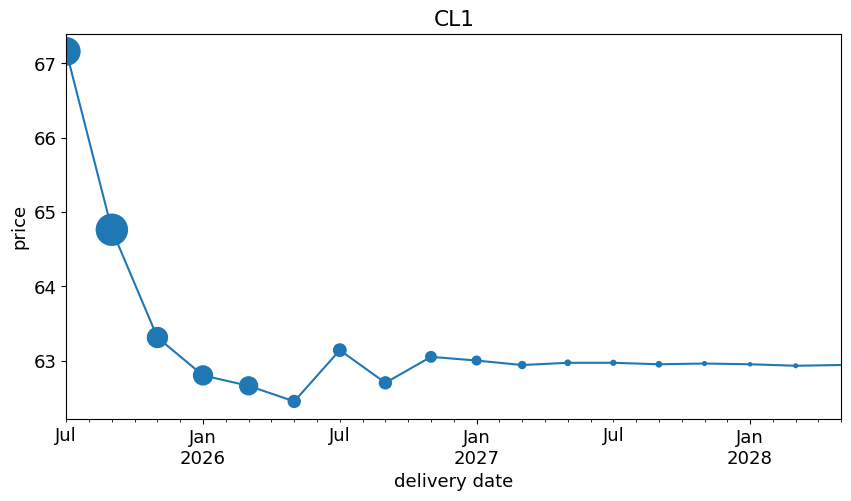

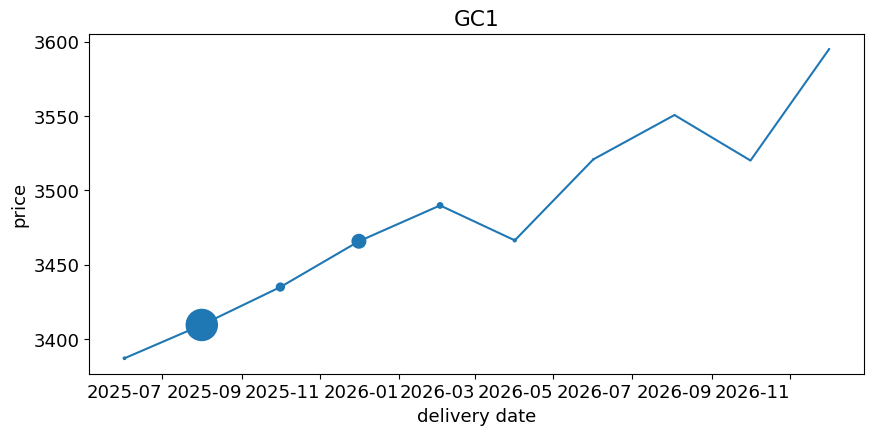

The Futures Curve#

Defining the Curve#

At a given date, consider the full chain of some futures contract:

list_curves = ['CL1','GC1']

curves = dict()

for comdty in list_curves:

curves[comdty]= pd.read_excel(LOADFILE,sheet_name=f'curve {comdty}')

curves[comdty].style.format({'price':'${:,.2f}', 'open interest':'{:,.0f}','deliver date':'{:%Y-%m-%d}'})

| ticker | delivery date | price | open interest | |

|---|---|---|---|---|

| 0 | GCM5 Comdty | 2025-06-02 00:00:00 | $3,387.10 | 1,828 |

| 1 | GCQ5 Comdty | 2025-08-01 00:00:00 | $3,409.50 | 319,598 |

| 2 | GCV5 Comdty | 2025-10-01 00:00:00 | $3,435.00 | 20,568 |

| 3 | GCZ5 Comdty | 2025-12-01 00:00:00 | $3,465.80 | 61,091 |

| 4 | GCG6 Comdty | 2026-02-02 00:00:00 | $3,489.90 | 9,796 |

| 5 | GCJ6 Comdty | 2026-04-01 00:00:00 | $3,466.40 | 2,560 |

| 6 | GCM6 Comdty | 2026-06-01 00:00:00 | $3,520.90 | 529 |

| 7 | GCQ6 Comdty | 2026-08-03 00:00:00 | $3,550.70 | 85 |

| 8 | GCV6 Comdty | 2026-10-01 00:00:00 | $3,520.10 | 13 |

| 9 | GCZ6 Comdty | 2026-12-01 00:00:00 | $3,595.00 | 78 |

If we plot this chain against the delivery dates, we get the futures curve.

The curves below show the marker sizes in proportion to the open interest of each contract.

for comdty in list_curves:

temp = curves[comdty].set_index('delivery date').sort_index()

msize = (temp['open interest']/temp['open interest'].max()) * 500

fig, ax=plt.subplots()

temp['price'].plot(ax=ax,marker=None,title=comdty)

temp.reset_index().plot.scatter('delivery date','price',s=msize,ax=ax,title=comdty)

plt.show()

Backwardation and Contango#

Relative to expectations#

“Normal” Backwardation

the futures price is below the expected future spot

Contango

the futures price is above the expected future spot

Economics#

Normal?#

“Normal” backwardation refers to economists (Keynes) thinking it should be the “normal” situation to have the futures price below the expected future spot.

The argument depends on the assumption that hedgers (suppliers) would tend to be short the futures contract while market-makers and speculators would be long. The risk aversion of the former group being higher than the latter group might lead to the futures price being pressured below the market forecast

Relation to pricing equations above#

The simple pricing above implies…

Contango = high carry costs relative to convenience yield

Backwardation = low carry costs relative to convenience yield

Descriptions of the futures curve#

Note that

there is not an objective “expected future spot”.

thus, whether in backwardation or contango would depend on one’s model of the forecasted spot price.

In practice, these terms are often used with the assumption that today’s spot is the best prediction of the future spot:

\(\begin{align} P_t = \boldsymbol{E}_t\left[P_T\right] \end{align}\)

Common usage#

This leads to the common usage.

Backwardation

the futures curve is downward sloping

Contango

the futures curve is upward sloping

This definition is simpler and can be directly measured.

In the examples above#

Oil is in backwardation

Gold is in contango

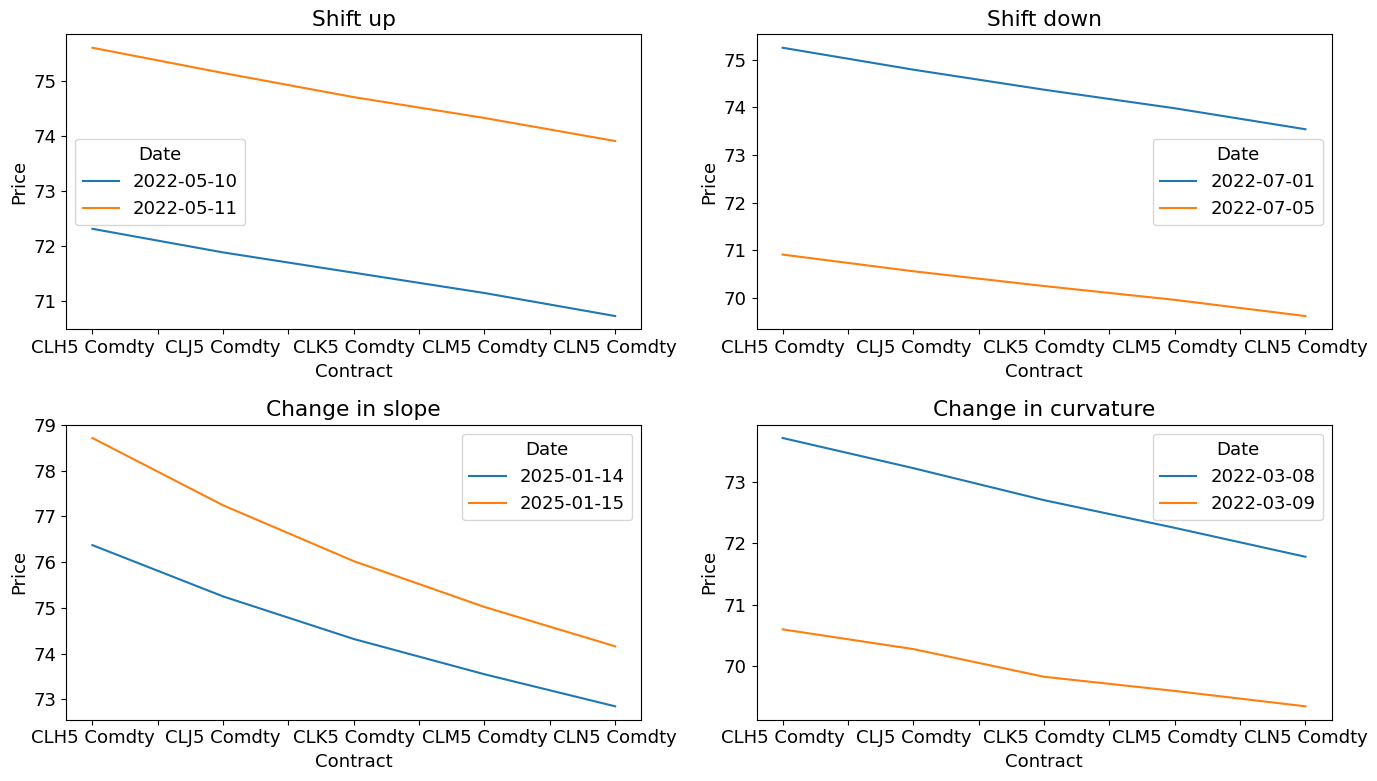

Does Backwardation Guarantee a Profit?#

df = pd.read_excel(

LOADFILE,

sheet_name="futures timeseries",

header=[0, 1],

index_col=0, # first column → index

parse_dates=[0], # parse that same column as dates

)

df_px_last = df.xs("LAST_PRICE", axis=1, level=1)

px_curves = df_px_last.loc[:, df_px_last.columns.str.startswith("CL")].dropna()

slopes = px_curves.diff(axis=1)

slope_range = slopes.max(axis=1) - slopes.min(axis=1)

curvature = slopes.diff(axis=1)

curv_range = curvature.max(axis=1) - curvature.min(axis=1)

idx_list = []

idx_list.append(px_curves.diff().mean(axis=1).idxmax())

idx_list.append(px_curves.diff().mean(axis=1).idxmin())

idx_list.append(slope_range.abs().idxmax())

idx_list.append(curv_range.abs().idxmax())

import matplotlib.pyplot as plt

import pandas as pd

list_titles = ['Shift up', 'Shift down', 'Change in slope', 'Change in curvature']

fig, axes = plt.subplots(2, 2, figsize=(14, 8))

for ax, idx in zip(axes.flatten(), idx_list):

prev_date = df.index[df.index < idx].max()

# plot (legend will pick up the raw datetime strings)

px_curves.loc[prev_date:idx].T.plot(ax=ax)

# grab the handles & labels, then reformat the labels

handles, labels = ax.get_legend_handles_labels()

new_labels = [pd.to_datetime(lbl).strftime("%Y-%m-%d") for lbl in labels]

ax.legend(handles, new_labels, title="Date")

ax.set_title(list_titles[0])

list_titles.pop(0)

ax.set_xlabel("Contract")

ax.set_ylabel("Price")

plt.tight_layout()

plt.show()

Roll#

Trading futures positions involves rolling the position to new contracts.

If the curve is in contango this rolling will require buying at a higher price

add capital to hold same number of contracts

keep capital flat, but in fewer contracts

If the curve is in backwardation this rolling will mean buying at a lower price

reallocate some capital to hold same number of contracts

keep capital flat, but in more contracts

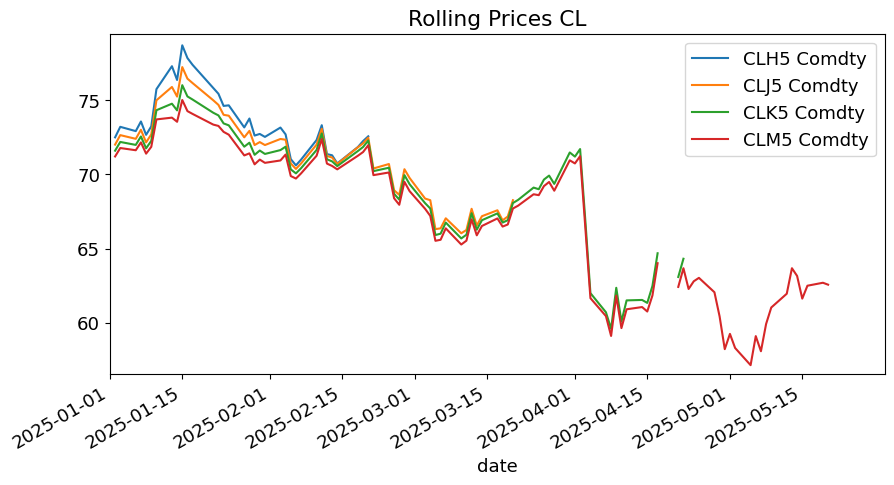

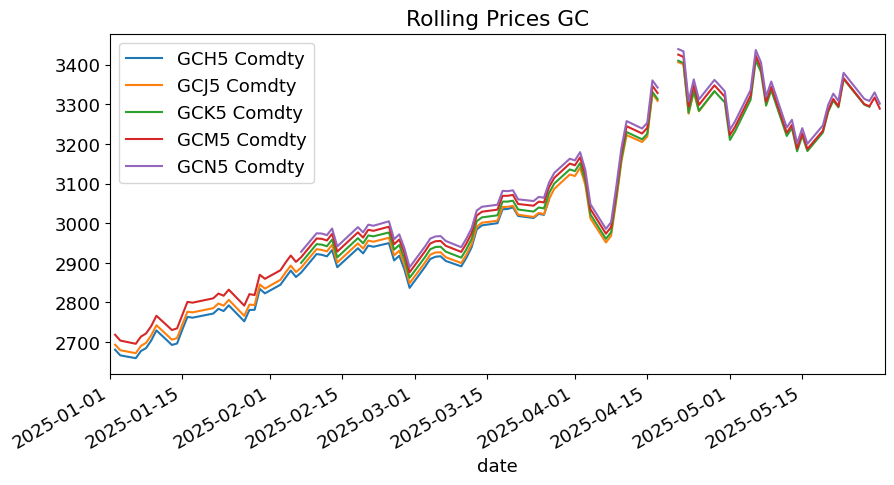

The chart below shows price histories for various contracts on the chain, note that when one settles, a trader would have to roll up/down to another contract.

PLOTDATESTART_2 = '2025-01'

ptitle = futures_ts['LAST_PRICE'].iloc[:,0].name[:2]

temp = futures_ts['LAST_PRICE'].iloc[:,0:4][PLOTDATESTART_2:PLOTDATEEND]

temp.plot(xlim=(PLOTDATESTART_2,PLOTDATEEND),ylim=(.99*temp.min().min(),1.01*temp.max().max()),title=f'Rolling Prices {ptitle}');

ptitle = futures_ts['LAST_PRICE'].iloc[:,-1].name[:2]

temp = futures_ts['LAST_PRICE'].iloc[:,5:][PLOTDATESTART_2:PLOTDATEEND]

temp.plot(xlim=(PLOTDATESTART_2,PLOTDATEEND),title=f'Rolling Prices {ptitle}');

Continuous Contract#

Given that futures contracts mature and roll off, it can be a challenge to obtain a long history of their prices.

This is similar to getting long timeseries of bond prices.

Generic indexes#

Like with bonds, the answer is to construct a generic index which is the compilation of many short-term instruments.

With bonds, this is done by building so-called “constant maturity” series, which at any point in the past point might point to the bonds closest in maturity to the stated index.

For futures, an index can be constructed by simply pointing to the active contract at any point in time.

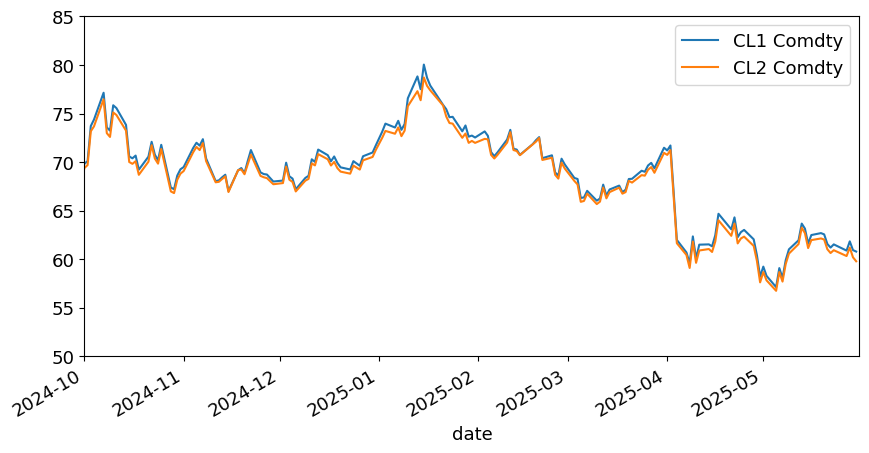

Generic front and back#

The common notation is to denote the generic front contract with a “1” and the generic back contract with a “2”.

For example, for crude oil, (CL), we have

CL1

CL2

The chart below shows these price series.

data_comp[['CL1 Comdty','CL2 Comdty']].plot(xlim=(PLOTDATESTART,PLOTDATEEND),ylim=(50,85));

Rolling the Continuous Series#

The complication with the continuous front and back futures series is that at the time of rolling, the price will jump simply due to the roll.

In analyzing the series, it will seem that these jumps are returns, when they are actually just a rebasing of the contract.

If a series tends to be in contango, this will make the returns seem artificially high.

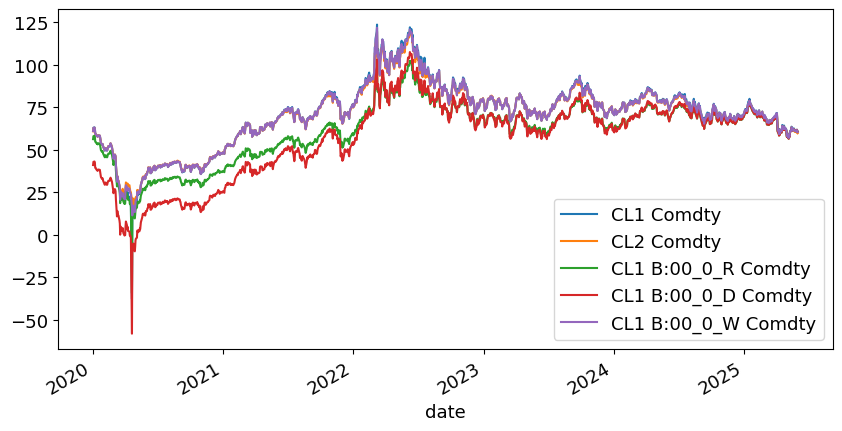

Adjusting the Continuous Series#

To avoid these jumps in the series, it is common to see one of three adjustments made at each roll, going back through time, to keep the breaks continuous.

difference: adjust the level by an addititive factor

ratio: adjust the past series by a multiplicative factor

weighted average: roll between the front and back contracts over a window of \(m\) days, taking a weighted average between the contracts.

The effect of all three adjustments is to

eliminate jumps at roll dates.

report true historic prices for the most recent contract used in the continuous series

report an adjusted price for the earlier contracts used in the continuous series

In these ways, it is similar to the adjustments to equity prices discussed in another note.

So which adjustment to use?#

difference: keeps the profit and loss true, which is useful if simulating a particular number of contracts

ratio: ensures valid return series, which is useful if simulating a particular investment size.

data_comp.plot();

Roll Rule#

There is also a decision to make regarding when to roll the contract in the continuous series. The most popular rules are

fixed date (often first day of the month)

at contract close

when the max open interest shifts

Careful with the roll method#

Using an improper roll method for historic analysis may greatly misrepresent the performance.

Which of these is correct for understanding returns over time?

px = data_comp.copy()

px[px<0] = np.nan

px[px==np.inf] = np.nan

rx_comp = px.pct_change()

metrics_comp = pd.DataFrame(columns=['mean','vol'],index=rx_comp.columns,dtype=float)

metrics_comp['mean'] = rx_comp.mean() * DAYS

metrics_comp['vol'] = rx_comp.std() * np.sqrt(DAYS)

metrics_comp.iloc[:3,:].style.format('{:.1%}')

/var/folders/zx/3v_qt0957xzg3nqtnkv007d00000gn/T/ipykernel_89789/1016369827.py:4: FutureWarning: The default fill_method='pad' in DataFrame.pct_change is deprecated and will be removed in a future version. Either fill in any non-leading NA values prior to calling pct_change or specify 'fill_method=None' to not fill NA values.

rx_comp = px.pct_change()

| mean | vol | |

|---|---|---|

| CL1 Comdty | 16.8% | 57.0% |

| CL2 Comdty | 17.0% | 60.7% |

| CL1 B:00_0_R Comdty | 17.6% | 55.2% |