The Fed#

import pandas as pd

import numpy as np

import datetime

import warnings

from sklearn.linear_model import LinearRegression

from scipy.optimize import fsolve

import matplotlib.pyplot as plt

%matplotlib inline

plt.rcParams['figure.figsize'] = (12,6)

plt.rcParams['font.size'] = 15

plt.rcParams['legend.fontsize'] = 13

data = pd.read_excel('../data/fed_data.xlsx',sheet_name='data').set_index('date')

FREQ = 52

if FREQ == 4:

FREQcode = 'Q'

elif FREQ == 1:

FREQcode = 'Y'

elif FREQ==12:

FREQcode = 'M'

elif FREQ==52:

FREQcode = 'W-FRI'

data = data.resample(FREQcode).agg('last')

info = pd.read_excel('../data/fed_data.xlsx',sheet_name='info').set_index('ticker (FRED)')

Monetary policy in the media#

In the media, monetary policy is typically reported with statements such as Powell lowered interest rates half a percentage point today.

What does this mean?

Of course, Powell did not change “interest rates.” Almost all interest rates are determined in the market. Powell manipulated a specific rate, the Fed Funds rate.

As noted above, the Fed Funds rate is a market rate, so the Fed “sets” it via open market operations discussed below.

Source

Bloomberg FED

Open Market Operations#

An expansionary open market operation, the Fed prints money and uses it to buy Treasury bonds.

This puts more money into the economy and raises the money supply.

In effect, it is as if the Fed is printing money and dropping it into the economy.

This causes downward pressure on short-term rates.

A contractionary open market operation is the reverse:

Sell some of the accumulated bonds in order to pull money back out of the market.

This causes upward pressure on short-term rates.

The Fed does not target the actual money supply, but rather a particular short-term interest rate: the Fed Funds rate.

These are two sides of the same coin.

The short-term Fed Funds rate moves negatively with the money supply.

At times, central banks target the actual money supply but it is harder to measure in real time.

Monetary Policy#

so as to promote effectively the goals of maximum employment, stable prices, and moderate long-term interest rates.

Referred to as the dual mandate#

Keep inflation low and stable

Keep economy at full employment

Third goal listed above regarding interest rates is seen as a consequence of the two above.

See the Inflation note for more on this topic.

Reference#

Temporary OMO#

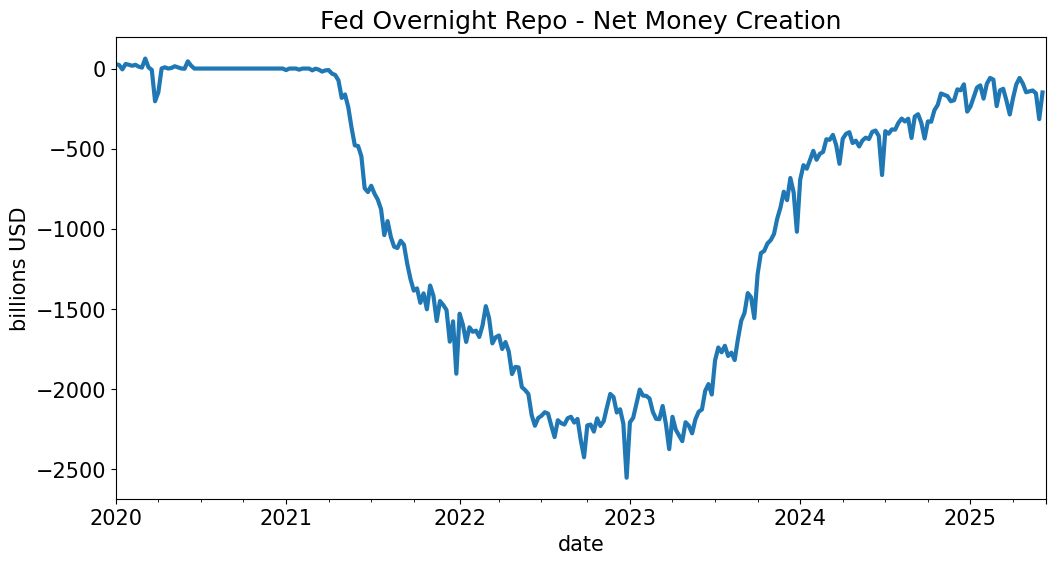

Importance of overnight repo.

Statement from the Fed…#

Temporary open market operations involve short-term repurchase and reverse repurchase agreements that are designed to temporarily add or drain reserves available to the banking system and influence day-to-day trading in the federal funds market.

Reverse Repo as described by the Fed#

A reverse repurchase agreement (known as reverse repo or RRP) is a transaction in which the New York Fed under the authorization and direction of the Federal Open Market Committee sells a security to an eligible counterparty with an agreement to repurchase that same security at a specified price at a specific time in the future. For these transactions, eligible securities are U.S. Treasury instruments, federal agency debt and the mortgage-backed securities issued or fully guaranteed by federal agencies.

For more information, see https://www.newyorkfed.org/markets/rrp_faq.html

Reference:#

https://fred.stlouisfed.org/series/RRPONTSYD

repo = data['RPONTSYD'] - data['RRPONTSYD']

repo.plot(xlim=('2020',None),linewidth=3,title='Fed Overnight Repo - Net Money Creation',ylabel='billions USD')

plt.show()

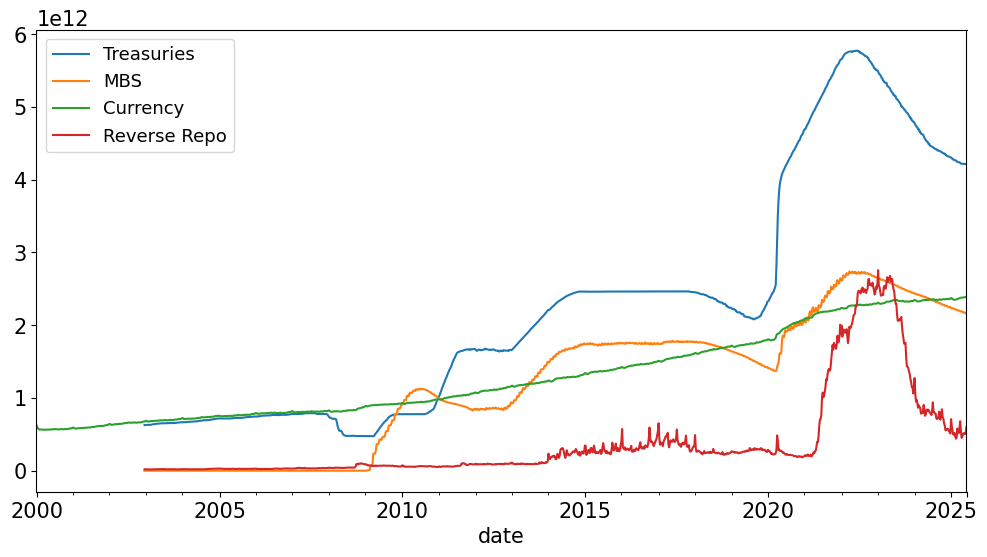

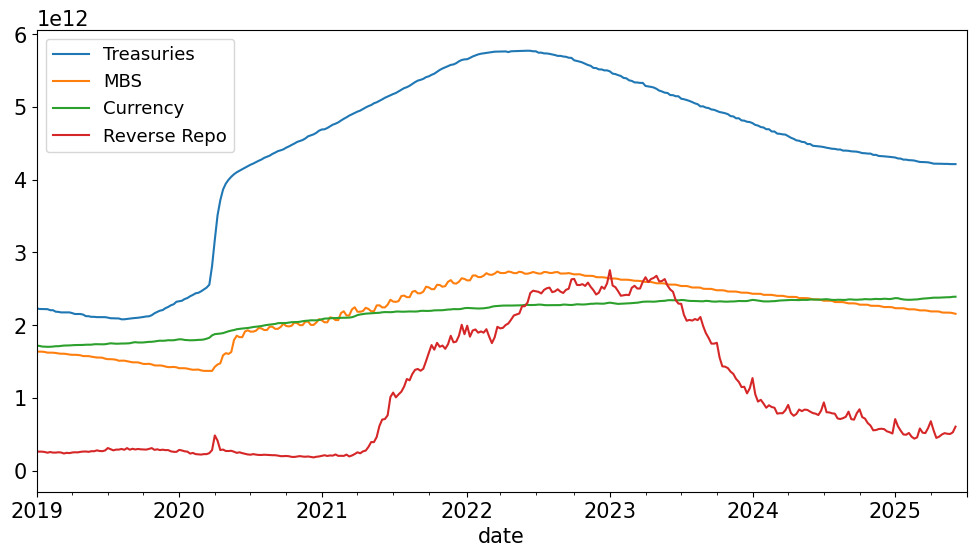

Beyond Treasuries#

It is not critical that Treasury bonds be used when the Fed exchanges new money for securities.

They could buy many things, but Treasury bonds are safe, liquid, and convenient.

During the Financial crisis, the Fed got very creative in what they bought.

To inject more money, the Fed bought asset-backed-securities including some potentially distressed mortgage-backed securities.

The following figure shows how the Fed has increased its assets and broadened what it is buying.

FOMC#

The Federal Open Market Committee determines when open market operations are used.

All 7 governors are voting members on this committee.

The NY Fed president is also a voting member.

Of the other 11 Fed presidents, 4 of them are voting members on a rotating basis.

FOMC Announcements#

Source#

Bloomberg FED->Calendar.

https://www.federalreserve.gov/monetarypolicy/fomccalendars.htm

Market Expectations#

Using STIR futures, infer the expected path of Fed Funds rates…

Using STIR options, compute probabilities of various rate hikes. CME FedWatch Tool

Balance Sheet#

data = pd.read_excel('../data/fed_bs.xlsx',sheet_name='data').set_index('date')

FREQ = 52

if FREQ == 4:

FREQcode = 'Q'

elif FREQ == 1:

FREQcode = 'Y'

elif FREQ==12:

FREQcode = 'M'

elif FREQ==52:

FREQcode = 'W-FRI'

data = data.resample(FREQcode).agg('last')

info = pd.read_excel('../data/fed_bs.xlsx',sheet_name='info').set_index('ticker (FRED)')

data.plot();

data.plot(xlim=('2019-01-01','2025-06-30'));

Source#

https://fred.stlouisfed.org/release/tables?rid=20&eid=840849#snid=840941

For another look at the balance sheet, try the Cleveland Fed’s tool.

https://www.clevelandfed.org/our-research/indicators-and-data/credit-easing.aspx

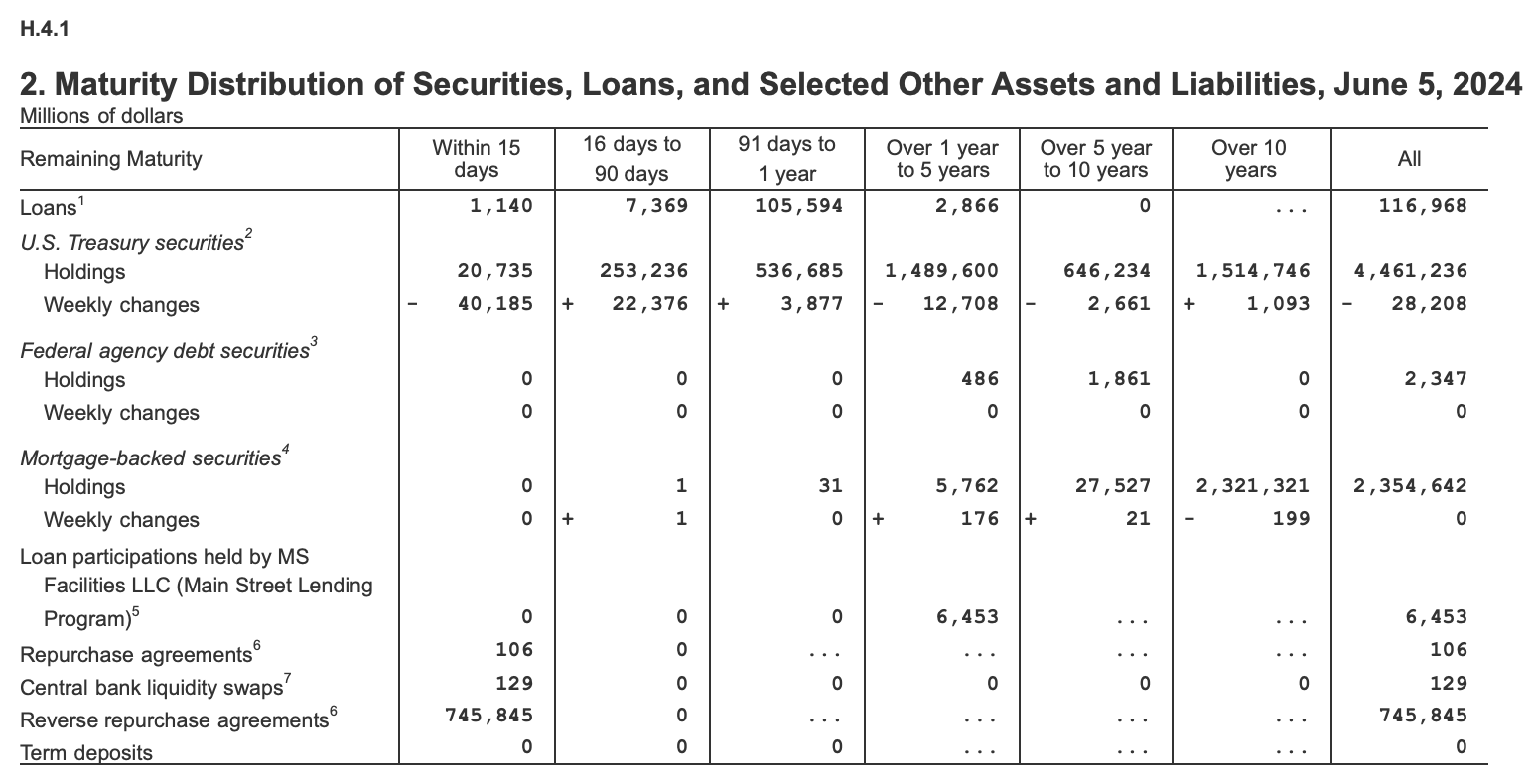

By Maturity#

Source:#

Table 2, current release. https://www.federalreserve.gov/monetarypolicy/bst_fedsbalancesheet.htm

Fed Structure#

The Federal Reserve is a system.

12 regional banks

along with a board of 7 governors.

Regional banks

president appointed by the regional bank’s board.

Board of Governors

14-year term, and is appointed by the President of the U.S. and confirmed by the Senate.

The long terms are meant to give them a degree of independence from political considerations.

The Chair of the Board of Governors is appointed by the President for a 4-year term.

Source:#

https://www.federalreserve.gov/monetarypolicy/files/BeigeBook_20220601.pdf

The Fed does more than monetary policy.

Lends to banks when they are having liquidity troubles.

This role was an important motivation in creating the Fed in 1914, as there were many bank failures leading up to that point.

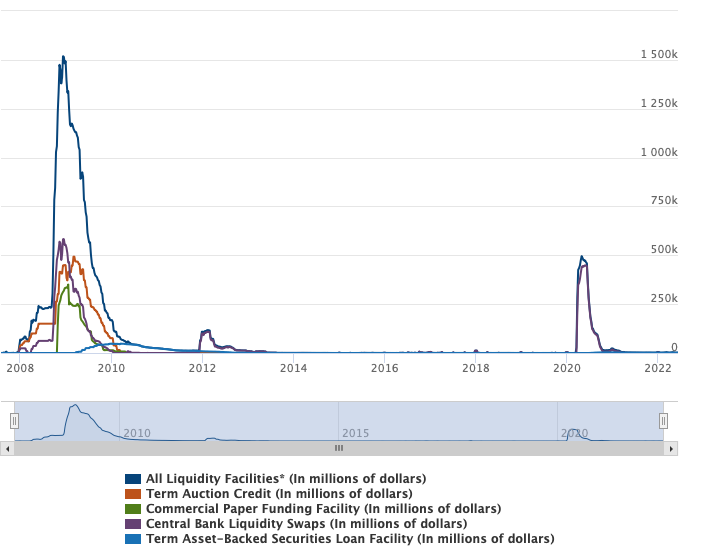

Liquidity Facilities#

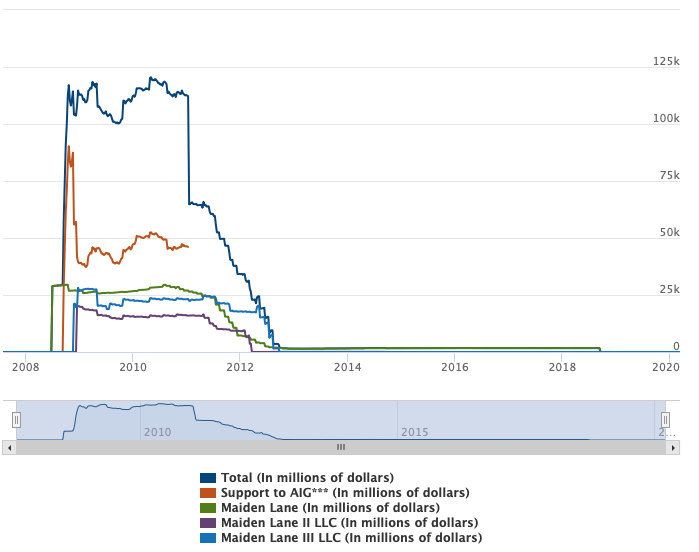

Support for Specific Institutions#

Source for charts#

https://www.federalreserve.gov/monetarypolicy/bst_recenttrends.htm

Appendix: Statistical Releases#

Daily H.15 Release#

Selected interest rates https://www.federalreserve.gov/releases/h15/

H.4.1 Release#

Federal Reserve’s Balance Sheet https://www.federalreserve.gov/releases/h41/

Beige Book#

https://www.federalreserve.gov/monetarypolicy/beige-book-default.htm

Appendix: Fed’s Impact on Shape of the Rate Curve#

When the Fed manipulates the short-term Fed Funds rate, how does the rest of the term structure respond?

While much research is still devoted to this question, empirical work indicates that the long term rates move in the same direction.

Namely, the Fed pumps money through buying bonds, which lowers the Fed Funds rate. On average, the long-term rates will also go down.

A conundrum?#

The fact that the long-rates move with the Fed Funds rate is somewhat surprising.

In the long-run, inflation is almost proportional to money growth.

Thus, if the Fed is pumping in money, one might think expected inflation would go up. - If investors expect more inflation, then the long-term rates would have to increase to compensate.

A resolution?#

Perhaps investors see the Fed pumping money in and infer that the Fed must be trying to fight off some deflation they see coming.

Then investors would not take the money injection as a sign of future inflation but rather a sign that the Fed now sees deflation as a threat.

Greenspan’s Conundrum#

In 2005, the usual empirical relation did not hold.

The Fed was raising the Fed Funds rate, but long-term rates were instead falling.

Greenspan remarked that this was a conundrum, as it did not obey the usual empirical relationship.

Of course, this is not that puzzling considering the alternate reasoning above.

The short rate was rising while the long rate fell until the yield curve inverted.

Repo at the Fed#

https://www.newyorkfed.org/markets/desk-operations/repo