TIPS#

Treasury Inflation Protected Securities (TIPS)

Treasury notes and bonds (no bills)

Semiannual coupon

Issued since 1997

Inflation protection#

TIPS provide a hedge against inflation.

Face value is scaled by CPI

Coupon rate is fixed

Fixed coupon rate multiplies the (CPI-adjusted) face-value, which leads to an inflation-adjusted coupon

import pandas as pd

import matplotlib.pyplot as plt

%matplotlib inline

plt.rcParams['figure.figsize'] = (10,6)

plt.rcParams['font.size'] = 15

plt.rcParams['legend.fontsize'] = 13

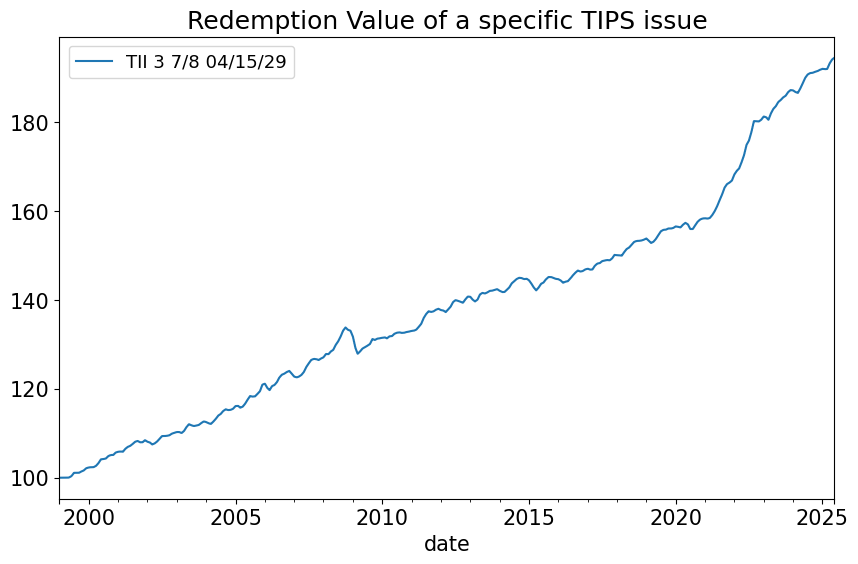

info_tips = pd.read_excel('../data/tips_data_bb.xlsx',sheet_name='info tips').set_index('security_name')

ts_tips = pd.read_excel('../data/tips_data_bb.xlsx',sheet_name='timeseries tips').set_index('date')

styler = (

info_tips.T.style

.format('{:%Y-%m-%d}', subset=pd.IndexSlice['issue_dt', :])

.format('{:%Y-%m-%d}', subset=pd.IndexSlice['maturity', :])

.format('{:.3f}', subset=pd.IndexSlice['issue_px', :])

.format('{:.3f}', subset=pd.IndexSlice['cpn', :])

.format('{:.3f}', subset=pd.IndexSlice['base_cpi', :])

.format('{:.1e}', subset=pd.IndexSlice['amt_issued',:])

)

styler

| security_name | TII 3 7/8 04/15/29 |

|---|---|

| BB ID | 912810FH@BGN Govt |

| issue_dt | 1999-04-15 |

| maturity | 2029-04-15 |

| cpn | 3.875 |

| amt_issued | 2.0e+10 |

| issue_px | 103.628 |

| base_cpi | 164.393 |

(ts_tips*100).plot(title='Redemption Value of a specific TIPS issue');

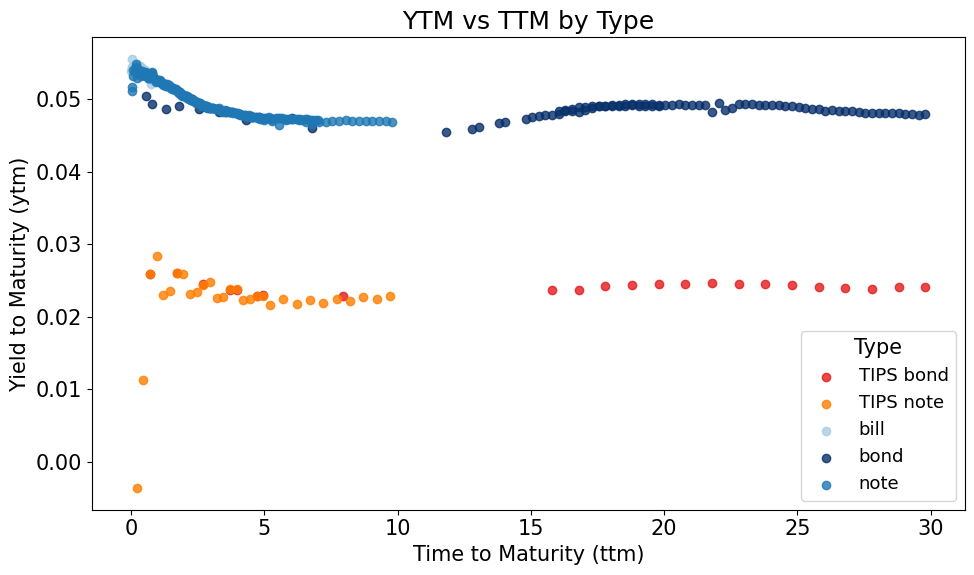

QUOTE_DATE = '2024-04-30'

filepath_rawdata = f'../data/treasury_quotes_{QUOTE_DATE}.xlsx'

data = pd.read_excel(filepath_rawdata,sheet_name='quotes').set_index('KYTREASNO')

from cmds.bond_calcs import crsp_data_calculate_ytm

ytm_calcs = crsp_data_calculate_ytm(data)

data['ytm'] = ytm_calcs['ytm']

from cmds.plot_utils import scatter_by_type

from cmds.config import COLOR_MAP

ax = scatter_by_type(

data,

x='ttm',

y='ytm',

color_map=COLOR_MAP,

xlabel='Time to Maturity (ttm)',

ylabel='Yield to Maturity (ytm)',

title='YTM vs TTM by Type',

alpha=0.8,

)

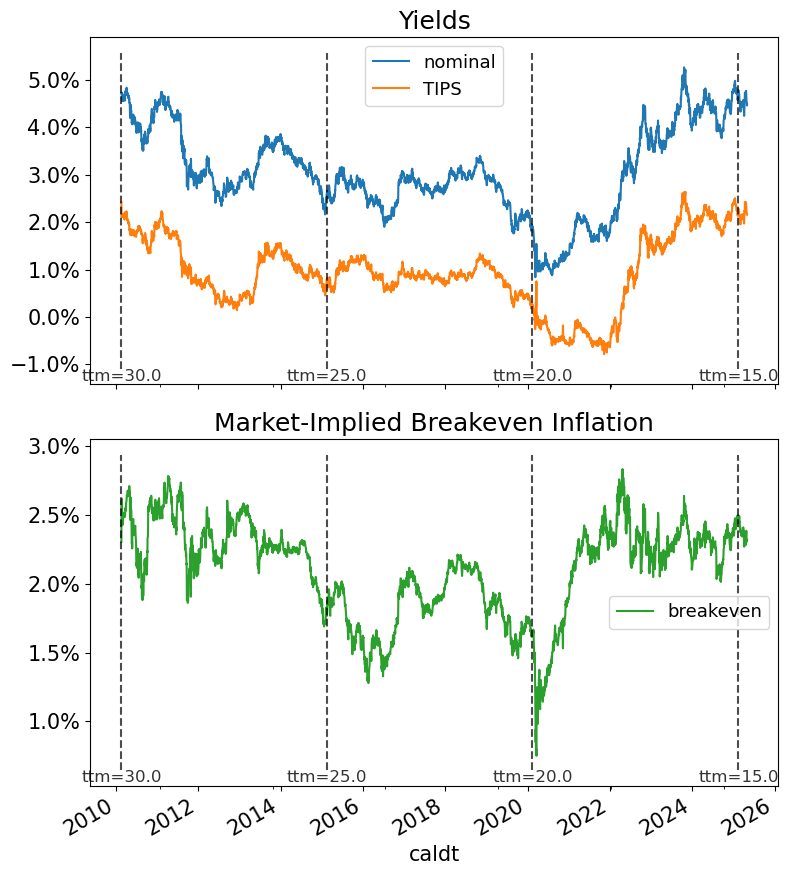

DATE = '2025-04-30'

FILEIN_TS = f'../data/treasury_ts_crsp_{DATE}.xlsx'

df_ytm = pd.read_excel(FILEIN_TS,sheet_name='ytm').set_index('caldt')

df_ttm = pd.read_excel(FILEIN_TS,sheet_name='ttm').set_index('caldt')

df_info = pd.read_excel(FILEIN_TS,sheet_name='info').set_index('Unnamed: 0').T

ttm = df_ttm.iloc[:, 0]

df_plot = df_ytm.copy()

# grab the first index value (or, if you actually want a column, use info['itype'].iloc[0])

first = df_info['itype'][0]

# decide the new column order in one line

new_cols = (['nominal','TIPS'] if first in (1, 2)

else ['TIPS','nominal'] if first in (11, 12)

else None)

if new_cols is None:

raise ValueError(f"Unexpected info index: {first!r}")

# apply the renaming

df_plot.columns = new_cols

/var/folders/zx/3v_qt0957xzg3nqtnkv007d00000gn/T/ipykernel_27098/2880877461.py:5: FutureWarning: Series.__getitem__ treating keys as positions is deprecated. In a future version, integer keys will always be treated as labels (consistent with DataFrame behavior). To access a value by position, use `ser.iloc[pos]`

first = df_info['itype'][0]

from matplotlib.ticker import PercentFormatter

import numpy as np

import matplotlib.pyplot as plt

tol = 0.01

max_val = ttm.max()

multiples = np.arange(5, max_val + 5, 5)

fig, (ax1, ax2) = plt.subplots(2, 1, sharex=True, figsize=(8, 9))

# ─── Top panel: your two curves ───

df_plot.plot(ax=ax1)

ymin1, ymax1 = ax1.get_ylim()

for m in multiples:

mask = np.isclose(ttm.values, m, atol=tol)

if not mask.any():

continue

loc = ttm.index[mask][0]

ax1.vlines(loc, ymin1, ymax1, colors='black', linestyles='--', alpha=0.7)

ax1.text(loc, ymin1, f"ttm={m}", rotation=0,

va='top', ha='center', fontsize=12, alpha=0.8)

ax1.legend()

ax1.set_title("Yields")

ax1.yaxis.set_major_formatter(PercentFormatter(xmax=1, decimals=1))

# ─── Bottom panel: the breakeven ───

breakeven = df_plot.iloc[:, 0] - df_plot.iloc[:, 1]

breakeven.plot(ax=ax2, label='breakeven', color='tab:green') # new color here

ymin2, ymax2 = ax2.get_ylim()

for m in multiples:

mask = np.isclose(ttm.values, m, atol=tol)

if not mask.any():

continue

loc = ttm.index[mask][0]

ax2.vlines(loc, ymin2, ymax2, colors='black', linestyles='--', alpha=0.7)

ax2.text(loc, ymin2, f"ttm={m}", rotation=0,

va='top', ha='center', fontsize=12, alpha=0.8)

ax2.legend()

ax2.set_title("Market-Implied Breakeven Inflation")

ax2.yaxis.set_major_formatter(PercentFormatter(xmax=1, decimals=1))

plt.tight_layout()

plt.show()

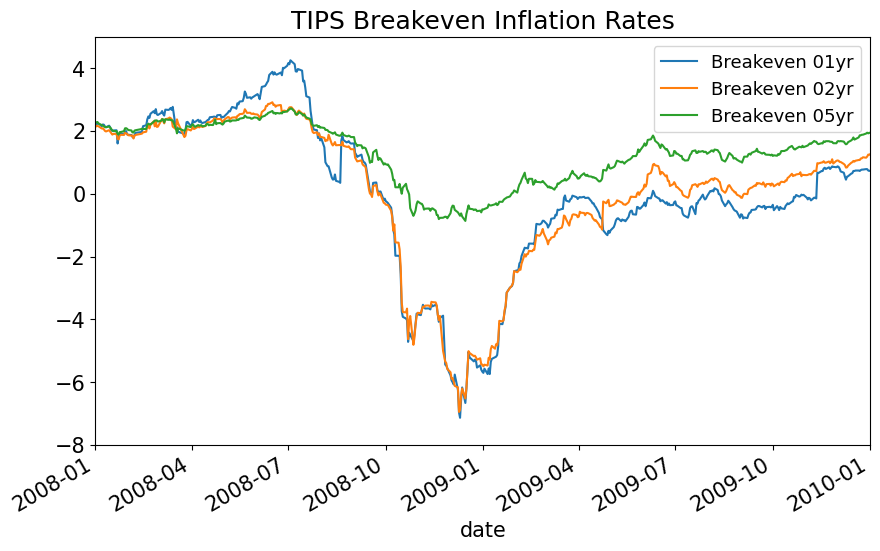

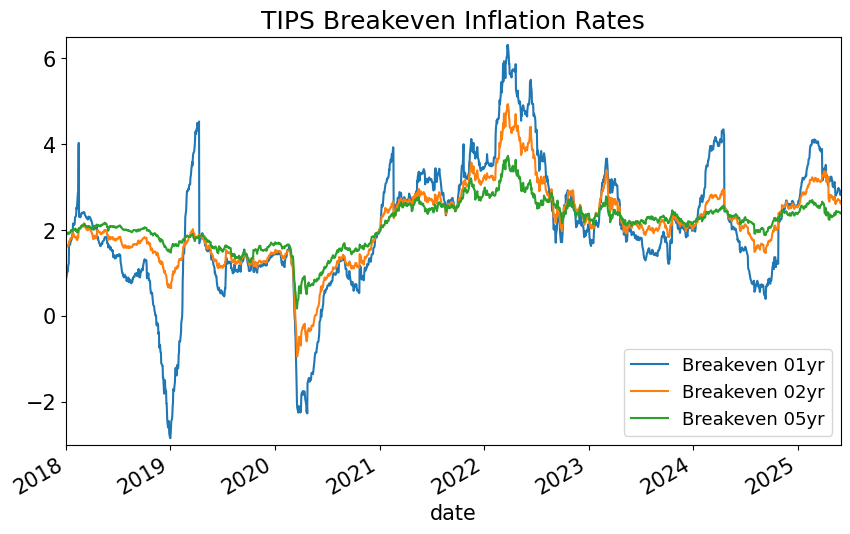

Market Expectations#

SELECT = 3

ts = pd.read_excel('../data/tips_data_bb.xlsx',sheet_name='timeseries breakeven').set_index('date')

ticks = ts.columns.str.split().str[0]

labels_ticks = [f'{tick[-3:-1]}yr' for tick in ticks]

labels_ticks = ['Breakeven ' + tick for tick in labels_ticks]

ts.columns = labels_ticks

ts.iloc[:,0:SELECT].plot(xlim=('2008','2010'),ylim=(-8,5),title='TIPS Breakeven Inflation Rates')

plt.show()

ts.iloc[:,0:SELECT].plot(xlim=('2018-01-01', '2025-05-31'),ylim=(-3,6.5),title='TIPS Breakeven Inflation Rates')

plt.show()

Expectations and Outcomes#

rawdata = pd.read_excel('../data/economic_data.xlsx',sheet_name='data').set_index('date')

FREQ = 4

if FREQ == 4:

FREQcode = 'QE'

elif FREQ == 1:

FREQcode = 'Y'

elif FREQ==12:

FREQcode = 'M'

data = rawdata.resample(FREQcode).agg('last')

data.index = data.index - pd.tseries.offsets.BDay(1)

data_econ = data

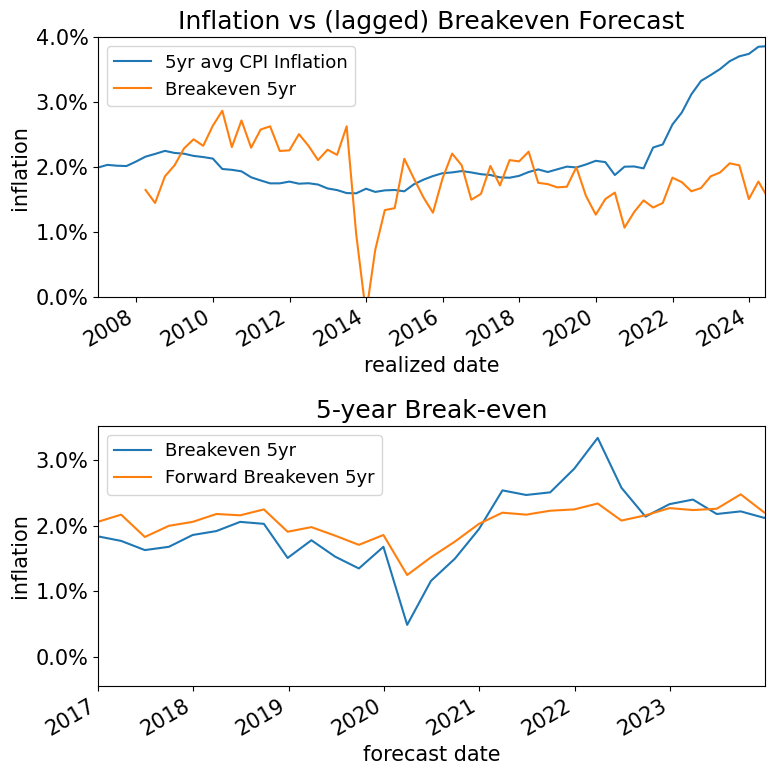

inflation = (data['CPI-Core']/data['CPI-Core'].shift(1) -1 ) * FREQ

import pandas as pd

import matplotlib.pyplot as plt

from matplotlib.ticker import StrMethodFormatter

# --- prepare your data (as you already have) ---

inflation_expectations = pd.concat([

inflation.rolling(FREQ*5).mean(),

(data_econ['Breakeven 5yr']/100).shift(5*FREQ)

], axis=1)

inflation_expectations.rename(

columns={'CPI-Core':'5yr avg CPI Inflation'},

inplace=True

)

# --- make the wide, 2×1 figure ---

fig, (ax1, ax2) = plt.subplots(

2, 1,

figsize=(8, 8), # wider than default

sharex=False, # each panel has its own x‐range

gridspec_kw={'height_ratios': [1,1]}

)

# Top panel: realized vs lagged breakeven

inflation_expectations.plot(

ax=ax1,

xlim=('2007-01-01','2024-05-31'),

ylim=(0, .04),

xlabel='realized date',

ylabel='inflation',

title='Inflation vs (lagged) Breakeven Forecast'

)

ax1.yaxis.set_major_formatter(StrMethodFormatter('{x:.1%}'))

# Bottom panel: breakeven series

(data_econ[['Breakeven 5yr','Forward Breakeven 5yr']] / 100).plot(

ax=ax2,

xlim=('2017-01-01','2023-12-31'),

xlabel='forecast date',

ylabel='inflation',

title='5-year Break-even'

)

ax2.yaxis.set_major_formatter(StrMethodFormatter('{x:.1%}'))

# tighten and show

plt.tight_layout()

plt.show()