Meme Stocks#

The Question#

What happens when retail traders discover options on highly shorted stocks?

Stocks analyzed: GameStop (GME), AMC, BlackBerry (BB), Bed Bath & Beyond (BBBY), and others from the 2021 meme stock frenzy.

Key metrics we’re tracking:

Options activity relative to shares outstanding

Volume patterns in calls vs puts

How options trading compares to stock trading

import pandas as pd

import numpy as np

import matplotlib.pyplot as plt

%matplotlib inline

plt.rcParams['figure.figsize'] = (9,5)

plt.rcParams['font.size'] = 11

plt.rcParams['legend.fontsize'] = 11

FILENAME = '../data/meme_stocks.xlsx'

SHEET = 'meme stock data'

ts = pd.read_excel(FILENAME, sheet_name=SHEET, header=[0, 1], index_col=0)

ts.tail().style.format('{:.1f}').format_index('{:%Y-%m-%d}')

| GME US Equity | AMC US Equity | AAPL US Equity | TSLA US Equity | NVDA US Equity | SPY US Equity | |||||||||||||||||||||||||||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| PX_LAST | OPEN_INT_TOTAL_CALL | OPEN_INT_TOTAL_PUT | VOLUME | VOLUME_TOTAL_CALL | VOLUME_TOTAL_PUT | EQY_SH_OUT | PX_LAST | OPEN_INT_TOTAL_CALL | OPEN_INT_TOTAL_PUT | VOLUME | VOLUME_TOTAL_CALL | VOLUME_TOTAL_PUT | EQY_SH_OUT | PX_LAST | OPEN_INT_TOTAL_CALL | OPEN_INT_TOTAL_PUT | VOLUME | VOLUME_TOTAL_CALL | VOLUME_TOTAL_PUT | EQY_SH_OUT | PX_LAST | OPEN_INT_TOTAL_CALL | OPEN_INT_TOTAL_PUT | VOLUME | VOLUME_TOTAL_CALL | VOLUME_TOTAL_PUT | EQY_SH_OUT | PX_LAST | OPEN_INT_TOTAL_CALL | OPEN_INT_TOTAL_PUT | VOLUME | VOLUME_TOTAL_CALL | VOLUME_TOTAL_PUT | EQY_SH_OUT | PX_LAST | OPEN_INT_TOTAL_CALL | OPEN_INT_TOTAL_PUT | VOLUME | VOLUME_TOTAL_CALL | VOLUME_TOTAL_PUT | EQY_SH_OUT | |

| date | ||||||||||||||||||||||||||||||||||||||||||

| 2025-06-24 | 23.3 | 996503.0 | 530788.0 | 11660172.0 | 135776.0 | 28848.0 | 447.3 | 3.0 | 629523.0 | 146802.0 | 4379887.0 | 36549.0 | 4166.0 | 433.1 | 200.3 | 2903818.0 | 2087842.0 | 54064033.0 | 554893.0 | 276554.0 | 14935.8 | 340.5 | 4231080.0 | 4009088.0 | 114736245.0 | 1096515.0 | 825473.0 | 3221.0 | 147.9 | 9641076.0 | 8768880.0 | 187566121.0 | 1573615.0 | 943560.0 | 24400.0 | 606.8 | 5292474.0 | 11305608.0 | 67735293.0 | 4021862.0 | 5257330.0 | 1023.2 |

| 2025-06-25 | 23.6 | 1013588.0 | 535743.0 | 9840749.0 | 98805.0 | 27869.0 | 447.3 | 3.0 | 638125.0 | 147400.0 | 4968114.0 | 26970.0 | 5303.0 | 433.1 | 201.6 | 2970777.0 | 2123396.0 | 39525730.0 | 438941.0 | 215690.0 | 14935.8 | 327.6 | 4395663.0 | 4118931.0 | 119845050.0 | 1703670.0 | 1186768.0 | 3221.0 | 154.3 | 10137395.0 | 9131950.0 | 269146471.0 | 3863998.0 | 1539360.0 | 24400.0 | 607.1 | 5426166.0 | 11495609.0 | 62114767.0 | 3811191.0 | 4158585.0 | 1029.9 |

| 2025-06-26 | 23.9 | 1036220.0 | 538544.0 | 8777965.0 | 130822.0 | 39860.0 | 447.3 | 3.0 | 649393.0 | 148795.0 | 4237091.0 | 38928.0 | 4006.0 | 433.1 | 201.0 | 3065468.0 | 2163559.0 | 50799121.0 | 601823.0 | 392877.0 | 14935.8 | 325.8 | 4466995.0 | 4202770.0 | 80440907.0 | 1158862.0 | 886635.0 | 3221.0 | 155.0 | 10316490.0 | 9414999.0 | 198145746.0 | 2074735.0 | 1351663.0 | 24400.0 | 611.9 | 5528473.0 | 12030509.0 | 78548361.0 | 3609760.0 | 4683545.0 | 1028.5 |

| 2025-06-27 | 23.6 | 1088638.0 | 551234.0 | 11638237.0 | 192027.0 | 46109.0 | 447.3 | 3.1 | 674242.0 | 153354.0 | 9739939.0 | 53032.0 | 8412.0 | 433.1 | 201.1 | 3162125.0 | 2190106.0 | 73188571.0 | 697983.0 | 322696.0 | 14935.8 | 323.6 | 4576464.0 | 4481144.0 | 89067049.0 | 1668487.0 | 1625142.0 | 3221.0 | 157.8 | 10509692.0 | 9756422.0 | 263234539.0 | 2628172.0 | 1618135.0 | 24400.0 | 614.9 | 5603665.0 | 12312087.0 | 86258398.0 | 4693802.0 | 5119717.0 | 1030.1 |

| 2025-06-30 | 24.4 | 988156.0 | 526013.0 | 10439313.0 | 170159.0 | 29771.0 | 447.3 | 3.1 | 645698.0 | 150747.0 | 6322139.0 | 59150.0 | 13676.0 | 433.1 | 205.2 | 3072744.0 | 2171894.0 | 91912816.0 | 1272592.0 | 365953.0 | 14935.8 | 317.7 | 4130528.0 | 3916484.0 | 76695081.0 | 681068.0 | 611189.0 | 3221.0 | 158.0 | 9984979.0 | 9123520.0 | 194580316.0 | 1292108.0 | 724481.0 | 24400.0 | 617.9 | 5524009.0 | 12421425.0 | 92502541.0 | 3853371.0 | 4346607.0 | 1024.9 |

Options Activity: The Scale of the Phenomenon#

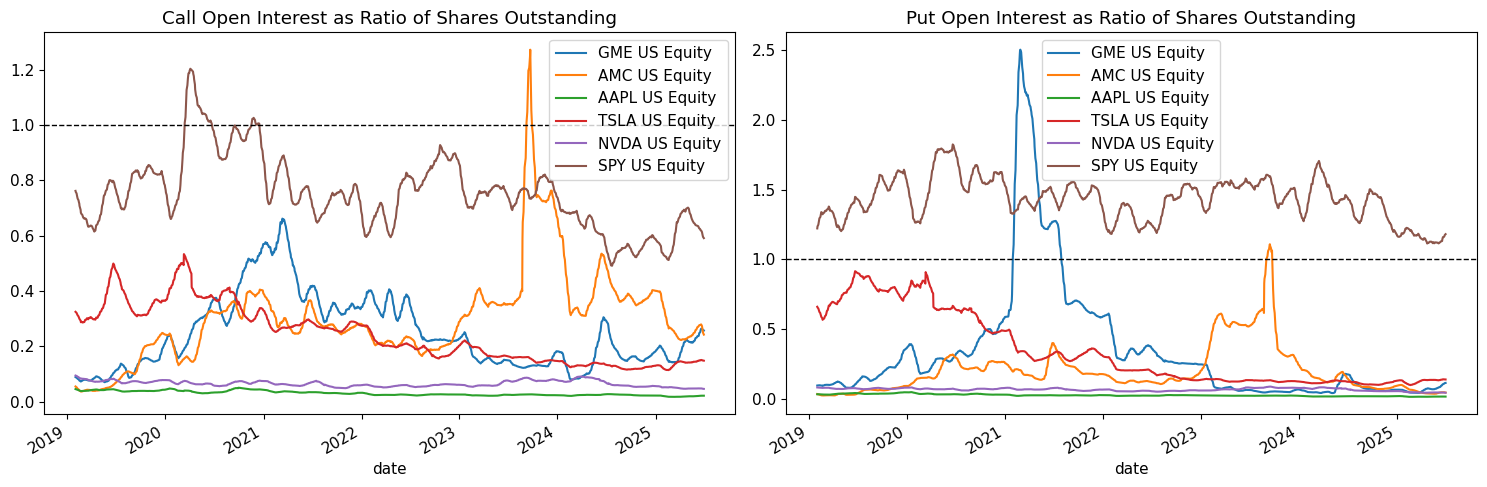

How Big Is the Options Market?#

We’re measuring open interest (total outstanding option contracts) as a percentage of shares outstanding.

SHARES_PER_CONTRACT = 100

SCALE_BB_SHARES_OUT = 1e6

open_call = ts.xs('OPEN_INT_TOTAL_CALL', axis=1, level=1)

open_put = ts.xs('OPEN_INT_TOTAL_PUT', axis=1, level=1)

sh_out = ts.xs('EQY_SH_OUT', axis=1, level=1)

open_call_pct = open_call.mul(SHARES_PER_CONTRACT).div(sh_out.mul(SCALE_BB_SHARES_OUT))

open_put_pct = open_put.mul(SHARES_PER_CONTRACT).div(sh_out.mul(SCALE_BB_SHARES_OUT))

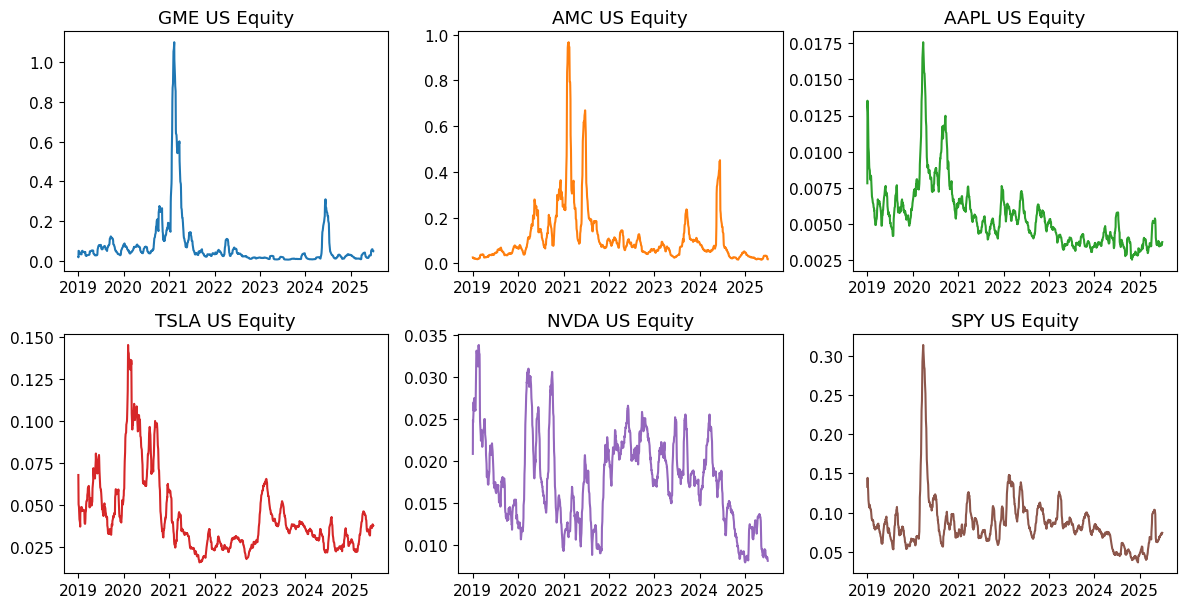

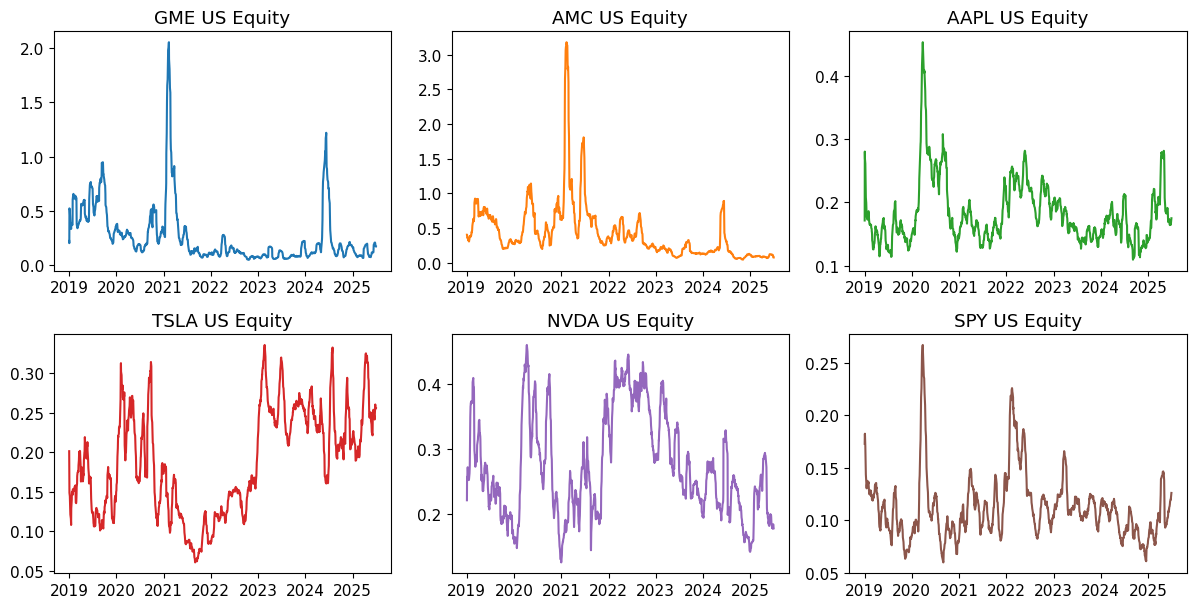

Call option open interest as ratio of shares outstanding.#

Do any of these stocks have more call option open interest than shares outstanding?

WINDOW = 21

fig, axes = plt.subplots(1, 2, figsize=(15, 5))

# Call options plot

open_call_pct.dropna().rolling(WINDOW).mean().plot(ax=axes[0], title='Call Open Interest as Ratio of Shares Outstanding')

axes[0].axhline(y=1, color='black', linestyle='--', linewidth=1)

# Put options plot

open_put_pct.dropna().rolling(WINDOW).mean().plot(ax=axes[1], title='Put Open Interest as Ratio of Shares Outstanding')

axes[1].axhline(y=1, color='black', linestyle='--', linewidth=1)

plt.tight_layout()

plt.show()

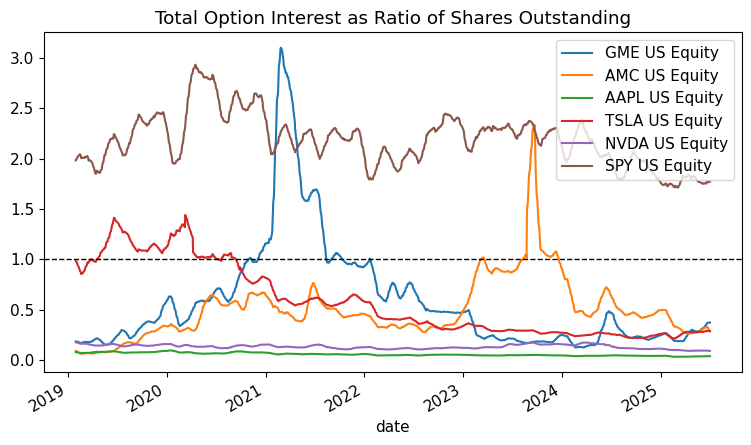

Total Options Activity#

Combined calls + puts: Shows the full scale of options open interest relative to the shares outstanding.

open_opt_pct = open_call_pct + open_put_pct

ax = open_opt_pct.dropna().rolling(WINDOW).mean().plot(title='Total Option Interest as Ratio of Shares Outstanding')

ax.axhline(y=1, color='black', linestyle='--', linewidth=1)

plt.show()

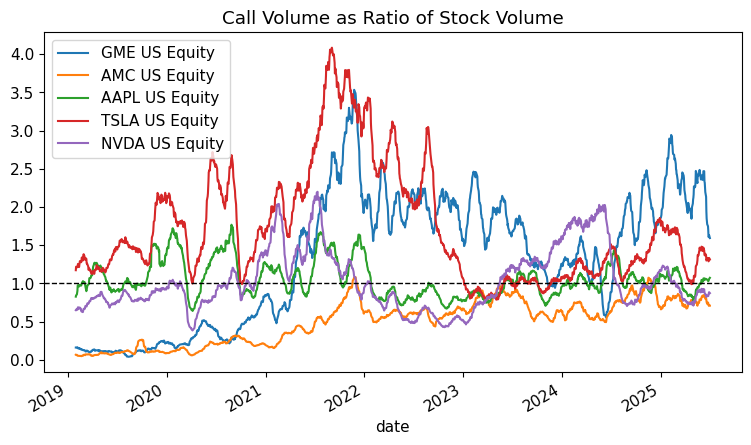

Volumes#

Call Volume Ratio: Call option volume as % of stock volume.

When this exceeds the 1% line, it means call option trading is unusually heavy relative to stock trading.

WINDOW = 21

FLDS = [

'VOLUME',

'VOLUME_TOTAL_CALL',

'VOLUME_TOTAL_PUT'

]

volumes = ts.xs(FLDS[0], axis=1, level=1)

volumes_call = ts.xs(FLDS[1], axis=1, level=1)

volumes_put = ts.xs(FLDS[2], axis=1, level=1)

volume_c_pct = (volumes_call * SHARES_PER_CONTRACT / volumes).rolling(WINDOW).mean()

volume_p_pct = volumes_put * SHARES_PER_CONTRACT / volumes

ax = volume_c_pct.drop(columns=['SPY US Equity']).plot(title='Call Volume as Ratio of Stock Volume')

ax.axhline(y=1, color='black', linestyle='--', linewidth=1)

plt.show()

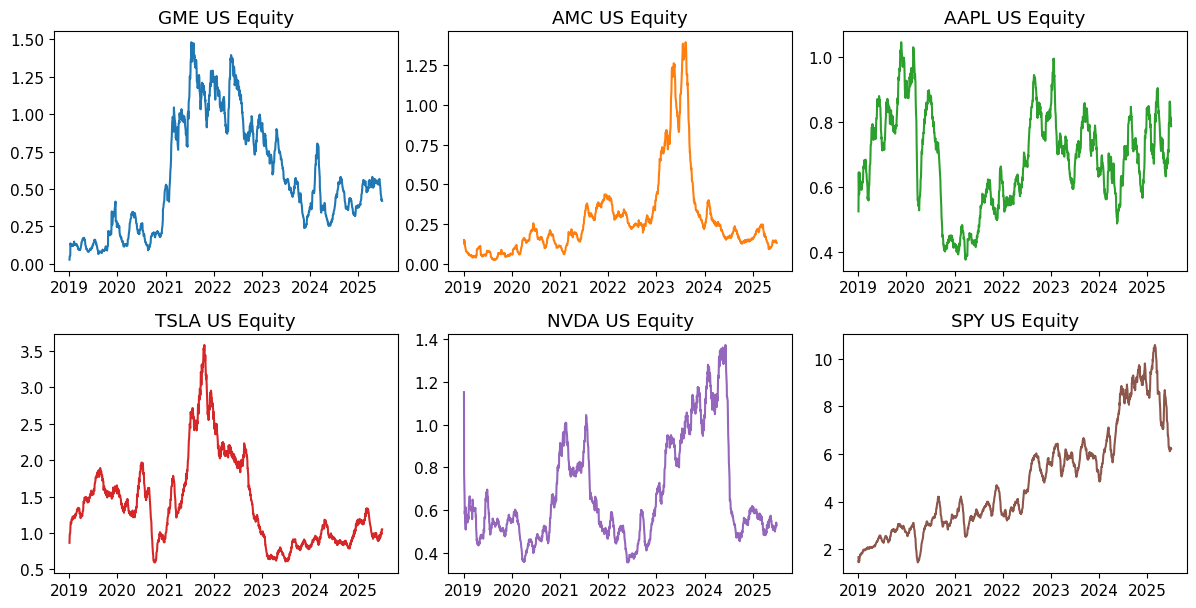

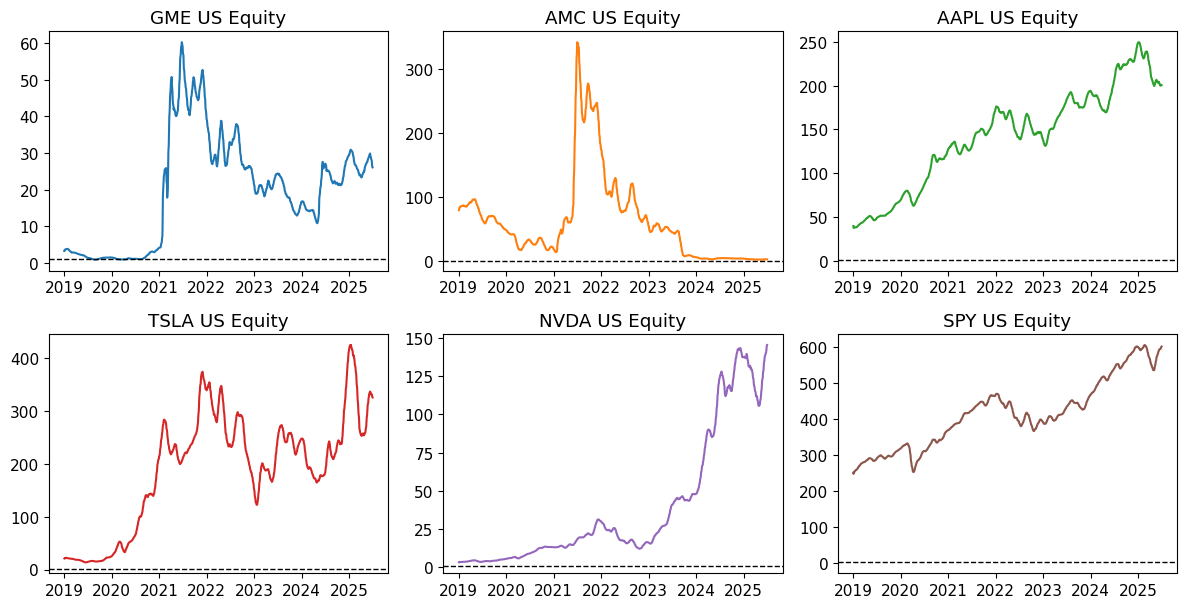

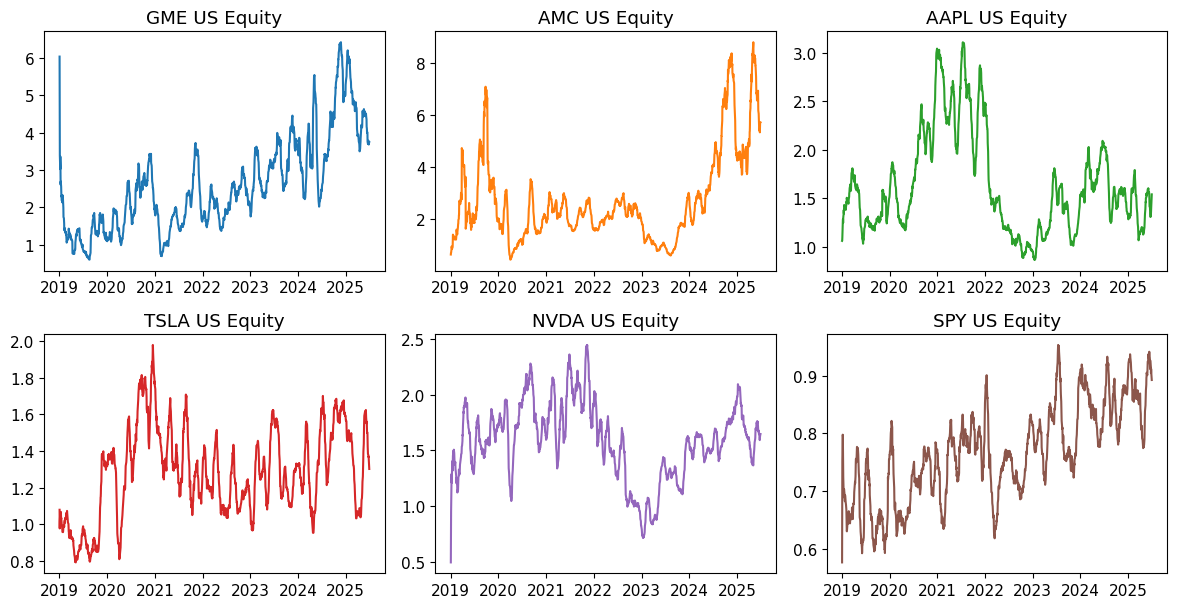

Stock Prices#

import math

import matplotlib.pyplot as plt

def plot_field(ts, field, window=10,

figsize=None, sharex=False, sharey=False):

"""

Extract one field from a MultiIndex-ts DataFrame and plot each stock.

Parameters

----------

ts : pd.DataFrame

Time-indexed DataFrame whose columns are a MultiIndex

(level0=stock tickers, level1=fields).

field : str

The second-level field name to extract (e.g. 'volume', 'price', etc.).

window : int, default=10

Rolling window size for smoothing.

figsize : tuple, optional

Figure size; if None it defaults to (4*n, 3*n).

sharex, sharey : bool, default=False

Whether subplots share x-/y-axes.

Returns

-------

fig, axes : matplotlib Figure and flattened Axes array

"""

# 1) extract the field across all tickers

try:

df = ts.xs(field, axis=1, level=1)

except KeyError:

raise KeyError(f"Field {field!r} not found in ts.columns")

# 2) set up grid

tickers = df.columns.tolist()

m = len(tickers)

n = math.ceil(math.sqrt(m))

fig, axes = plt.subplots(n, n,

figsize=figsize or (4*n, 3*n),

sharex=sharex,

sharey=sharey)

axes = axes.flatten()

# 3) pull the default color cycle

colors = plt.rcParams['axes.prop_cycle'].by_key()['color']

# 4) loop & plot

for i, (ax, ticker) in enumerate(zip(axes, tickers)):

sm = df[ticker].rolling(window=window, min_periods=1).mean()

ax.plot(sm.index, sm.values,

color=colors[i % len(colors)])

ax.axhline(1, linestyle='--', linewidth=1, color='black')

ax.set_title(ticker)

# 5) hide any unused axes

for ax in axes[m:]:

ax.set_visible(False)

plt.tight_layout()

return fig, axes

FLD = 'PX_LAST'

fig, axes = plot_field(ts, FLD, window=WINDOW)

plt.show()

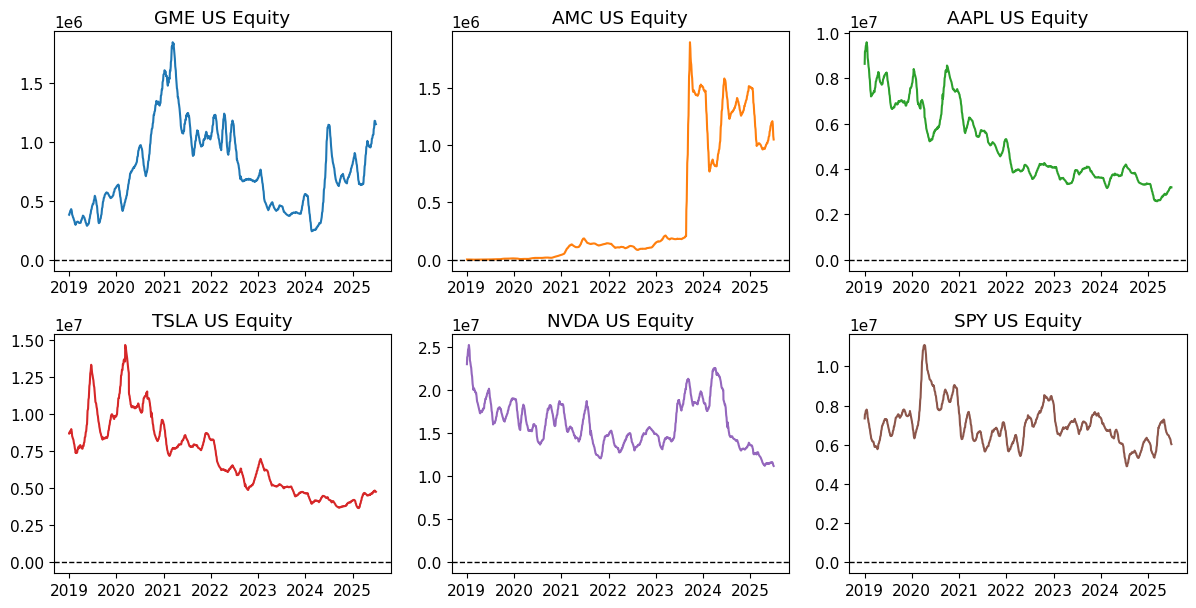

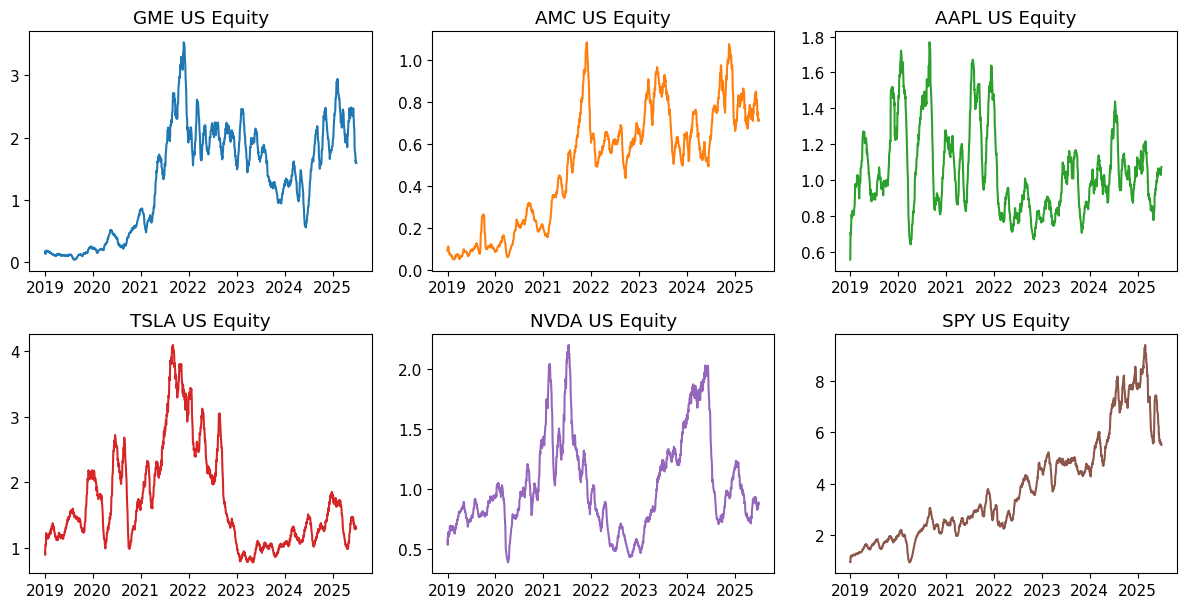

FLD = 'OPEN_INT_TOTAL_CALL'

fig, axes = plot_field(ts, FLD, window=WINDOW)

#plt.show()

Stock Volume vs. Call Open Interest#

What this shows: How many shares trade relative to call option positions.

Lower ratios suggest options activity is very large compared to stock trading.

fig, axes = plot_field_ratio(ts, 'VOLUME', 'EQY_SH_OUT', window=WINDOW,scale=1/1e6)

plt.show()

Call vs. Put Volume Ratio#

Sentiment indicator: Values above 1.0 show more call than put volume (bullish bias).

Meme stocks typically show very high call/put ratios during rallies.

fig, axes = plot_field_ratio(ts, 'VOLUME', 'OPEN_INT_TOTAL_CALL', window=WINDOW,scale=1/100)

Call Volume as % of Stock Volume#

Scale of speculation: When call volume exceeds 10-20% of stock volume, it indicates massive options speculation.

fig, axes = plot_field_ratio(ts, 'VOLUME_TOTAL_CALL', 'VOLUME_TOTAL_PUT', window=WINDOW)

Put Volume as % of Stock Volume#

Bearish activity: Generally much lower than call volume for meme stocks - retail traders were primarily betting on upward moves.

Extra Analysis#

Peak Options Activity Summary#

# Summary of peak options activity for each stock

summary_stats = pd.DataFrame()

# Peak call open interest as % of shares outstanding

summary_stats['Peak Call OI %'] = open_call_pct.max()

# Peak put open interest as % of shares outstanding

summary_stats['Peak Put OI %'] = open_put_pct.max()

# Peak total options activity

summary_stats['Peak Total OI %'] = open_opt_pct.max()

# Peak call volume as % of stock volume

peak_call_vol = (volumes_call * 100 / volumes).max()

summary_stats['Peak Call Vol %'] = peak_call_vol

# Clean up and sort

summary_stats = summary_stats.round(2)

summary_stats = summary_stats.sort_values('Peak Total OI %', ascending=False)

print("Peak Options Activity by Stock:")

print("=" * 40)

summary_stats

Peak Options Activity by Stock:

========================================

| Peak Call OI % | Peak Put OI % | Peak Total OI % | Peak Call Vol % | |

|---|---|---|---|---|

| AMC US Equity | 4.36 | 5.11 | 9.48 | 1.74 |

| TSLA US Equity | 1.40 | 2.68 | 4.08 | 6.15 |

| GME US Equity | 0.77 | 3.02 | 3.73 | 5.16 |

| SPY US Equity | 1.37 | 1.97 | 3.11 | 13.07 |

| NVDA US Equity | 0.11 | 0.09 | 0.20 | 3.85 |

| AAPL US Equity | 0.07 | 0.07 | 0.14 | 5.79 |

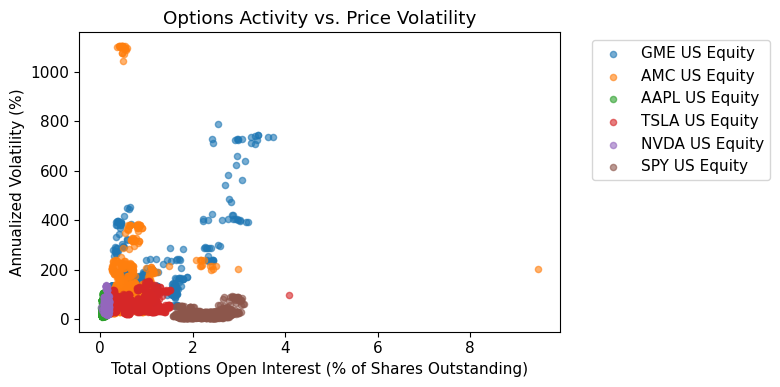

Options Activity vs. Price Volatility#

# Calculate price volatility and compare with options activity

prices = ts.xs('PX_LAST', axis=1, level=1)

returns = prices.pct_change()

volatility = returns.rolling(WINDOW).std() * np.sqrt(252) * 100 # Annualized vol

# Create scatter plot of options activity vs volatility

fig, ax = plt.subplots(1, 1, figsize=(8, 4))

for stock in open_opt_pct.columns:

if stock in volatility.columns:

# Get data where both exist

opt_data = open_opt_pct[stock].dropna()

vol_data = volatility[stock].dropna()

# Align the data

common_dates = opt_data.index.intersection(vol_data.index)

if len(common_dates) > 10: # Only plot if we have enough data

ax.scatter(opt_data[common_dates], vol_data[common_dates],

alpha=0.6, label=stock, s=20)

ax.set_xlabel('Total Options Open Interest (% of Shares Outstanding)')

ax.set_ylabel('Annualized Volatility (%)')

ax.set_title('Options Activity vs. Price Volatility')

ax.legend(bbox_to_anchor=(1.05, 1), loc='upper left')

plt.tight_layout()

plt.show()

Key Takeaways#

- Massive options activity: Open interest often exceeds 5-10% of shares outstanding

- Bullish bias: Call volume dominates put volume by huge margins

- Retail-driven: Options volume can exceed 20%+ of stock volume during peaks

- High volatility: Options activity correlates with extreme price swings

The 2021 meme stock phenomenon showed how options markets can amplify retail sentiment and create feedback loops between options activity and stock prices.

fig, axes = plot_field_ratio(ts, 'VOLUME_TOTAL_CALL', 'VOLUME', window=WINDOW,scale=100)

plt.show()

fig, axes = plot_field_ratio(ts, 'VOLUME_TOTAL_PUT', 'VOLUME', window=WINDOW,scale=100)

plt.show()